Podcast: Play in new window

- The Haven Status Of U.S. Treasuries Is Eroding

- Olympic Medal Gold & Gold Investment Similarities to 1980

- Blue Owl (Canary) Suspends Payments Indefinitely

John Exter’s Inverted Liquid Pyramid

“It’s telling us a lot in recent years, the price of gold. Geopolitics is in the frame, and with a disruption in relationships—not just trade relationships—there’s a signal there in the gold market. But over-indebtedness is also in the frame, and over-indebtedness is a key factor driving the durability of this gold cycle. I think that’s one of the most critical takeaways. If you’re looking back at where prices were, 1980 gold hit a peak. Are we at a peak in gold today? I would say again, over-indebtedness is a key factor driving the durability of this gold cycle.” —David McAlvany

* * *

Kevin: Welcome to the McAlvany Weekly Commentary. I’m Kevin Orrick, along with David McAlvany.

Well, David, I certainly wish we would fight most of our wars on the ice rather than with weaponry. Now, I’m thinking back to 1980. But even now, I mean, look at what happened on Sunday and Saturday with the women’s and the men’s team.

David: Amazing. The women did great overtime and a victory over the Canadians. Again, the men’s hockey team, US beating Canadians. Probably the most meaningful Olympic gold handed out this year, meaningful to me, was the US men’s hockey win against the Canadians.

Kevin: You remember the 1980 game, how critical that was. Well, the sequence of events that had occurred in that time frame with Russia and with America, and the wars that were going on in Afghanistan, that hockey game was an amazing relief. And you were alive at the time.

David: Yeah, I think the win this week was purely sentimental for me, a walk down memory lane. Obviously, 1980 was a long time ago, and I watched that victory 46 years ago, which was not only a massive upset against the Soviet team— They had won in ’56 and ’64 and ’68 and ’72 and ’76. I mean, they were just unstoppable.

Kevin: Unbeatable, yeah.

David: Until 1980. And then of course they picked it back up again in ’84 and ’88 and ’92 and 2018. The Russian team has always been phenomenal. At that time, it was a shot in the arm for American patriotism and national pride, at a time when the Soviets, as you mentioned, were invading Afghanistan, stoking revolutions in Central America and the Caribbean Basin, and setting the world on edge as they sought global dominance. It was also a shot across the bow, don’t count out the USA.

Kevin: Yeah, and for people who were not alive at that time, it’s hard to really help them get their head around what that felt like. We had the Iranian hostage crisis going on, we had Russia going into Afghanistan. Khrushchev had said, about 15 years before, that he was going to try to dominate, or Russia would dominate, all the mineral resources and the petroleum resources in the world. And it looked like that was happening.

David: And yet under the surface there was something quite different. The last half of Sun Tzu’s dictum was, I think, being applied by the Russians, appear weak when you are strong and strong when you are weak. And the hockey team was strong, but the empire was in fact in collapse, and all the Russians had was a show of strength, but in 1980 even that fell apart.

So less than a decade later, the Soviet empire was in shambles. Gorbachev launched his Perestroika and Glasnost shortly after coming to power in 1985. Chernobyl opened why the idea that Soviet engineering was not indomitable. And by 1988, the Baltics were pushing for sovereignty. Estonia was the first to declare it. The Berlin Wall fell in 1989, effectively signaling the beginning of the end for everything behind the Iron Curtain. And by March of 1990, 10 years later—after the hockey game of course— We anchor all of history according to hockey. But you had the Communist Party’s monopoly on Eastern European power—it was over. 1991, December of that year, the Soviet Union was dissolved.

Kevin: Yeah, and you were raised in a household, Dave, probably unlike most. Even though we were aware of the Cold War, your father was probably one of the most staunch anti-communist writers and commentators at the time. So I mean, how did that affect you when you saw the Soviet Union actually dissolving, even though they were trying to put up the appearance of strength?

David: Yeah, you’re right. Child of the Cold War, born to parents with an interest in current events, dialed into the US-Soviet military competition of the ’70s and ’80s. And when the Russian hockey team played in Lake Placid, lost to Team USA, it was more than a sporting event, more than an upset on the ice. It’s been 46 years since our team won the gold medal on the ice, so it was particularly stirring for me.

Kevin: The kid who shot the final goal on Sunday morning, that game started at six o’clock Mountain Time, and when he shot that final goal, and then they interviewed him right afterwards, it gave me the memory of the national pride we had back in 1980. He was not ashamed to be an American.

David: Now, and in many circles in the US today, national pride has been replaced with self-loathing. And I’d suggest that sporting events have always been more than sporting events. In the Cortina games this year, I mean, we had 64 golds won by US athletes, a phenomenal showing. And I appreciate it. No apologies.

Kevin: I was in high school in 1980, and I do remember I had the choice of going skiing or staying home and watching the game. So I did, I went skiing. But the game was everywhere, the radios were on. And I remember when the US won that game, just the shouts while everybody was in a lift line, I think I was at Vail, if I remember right. But where were you? I mean, you were just a kid.

David: I got a text from our first hire the other day, right after the games finished.

Kevin: Steve?

David: Steve Van Erden. Nearly 50 years ago, as we transitioned from a business run single-handedly by my mother towards the metals brokerage we are today, doing more business in a month than we used to do in a decade, he lived with our family. He was like an older brother, he was like an uncle, and—

Kevin: And he was the first person this company ever hired.

David: Yeah. And in that text exchange, he was recalling the game we watched together. It was amazing then, and it was fun to recall it.

When I recall the strained years of the oil embargoes that just preceded, the stress on the dollar market, the uncertainty tied to global military competition, and the rivalry on display, you could see it in every May Day parade. There’s as many differences as similarities between the 1980s and the present.

Kevin: But you have a constant, because think about what was happening to gold at that time, David.

David: Yeah, I mean, so you’ve got global power rivalries, check. We’ve got that, that’s similar. A strain on the dollar, check. That’s like today. More acutely, today you’ve got pressure building in the US bond market. And you’re right, then and now gold was a barometer for uncertainty, and it told of the shifts that were occurring on the world stage.

So geopolitics featured prominently then and now, the US dollar had, throughout the 1970s, come under intense pressure, as budgetary strains mounted as inflation took hold. And so we lived through the potential demise of dollar dominance then, largely bailed out by the petrodollar system, which forced an increase in US dollar holdings throughout the global financial system.

Kevin: Everybody had to have dollars to buy oil.

David: For trade settlement, primarily for oil. So then followed the upswing in dollar strength from ’80 to ’85, roughly 50% from 1980 to 1985.

Kevin: Almost too much, right? I mean, the administration didn’t want to see that strong of a dollar.

David: Right. So it required a coordinated effort, 1985, to devalue the dollar. And that was implemented following what is called the Plaza Accord. They met at the Plaza Hotel right on the edge of South Central Park in New York City. And against the yen had triggered a 50% decline, against the West German mark, a 45 to 50% decline. This is over a two-year period.

Kevin: And that was a policy shift, right, to have a weaker dollar?

David: Oh, yeah. And against a trade-weighted basket of currencies it was a 30 to 40% decline over the following two years. So it was the group of five, US, Japan, West Germany, France, the United Kingdom. And there is talk today of the US dollar being overvalued.

Kevin: Okay. So we’ve talked about this before. We’ve talked about Scott Bessent, and some of the vocabulary of a weaker dollar being needed, maybe less of a reserve currency status, but back in 1980, Dave, we had taken from George Washington all the way to Jimmy Carter to get to a trillion. 1 trillion in debt. Can we do anything like what Volcker did with, what, almost 40 trillion in debt?

David: Yeah. I think the biggest difference I see today from that time frame is in our debt markets. To address inflation, Volcker was willing and the markets were able to absorb a spike in interest rates that took fed funds briefly over 20%.

Kevin: That was amazing. CDs were paying 20%.

David: Yeah. So the quantity of debt we have today takes a policy shift of that magnitude off the table, and it’s not warranted anyways. We’re well below the CPI levels, consumer price index levels, of 13%, 14% we had then. More to the point, we can’t raise rates significantly. And if the market forces up rates at the long end of the curve, even small shifts in interest rates are highly consequential today. Debt service costs already exceed 20% of tax revenue, so we can’t take much more.

Kevin: And gold is becoming the unnamed international currency again. That’s what seems to be happening.

David: Right. It’s telling us a lot in recent years, the price of gold. Geopolitics is in the frame, and with a disruption in relationships, not just trade relationships, there’s a signal there in the gold market. But over-indebtedness is also in the frame, and over-indebtedness is a key factor driving the durability of this gold cycle. I think that’s one of the most critical takeaways.

If you’re looking back at where prices were—1980, gold hit a peak. Are we at a peak in gold today? I would say, again, over-indebtedness is a key factor driving the durability of this gold cycle. So we have almost a necessity to devalue the currency, to alleviate the strain of our over-indebtedness. And we have an administration who, from a policy perspective, are intent on rebuilding our industrial base.

So whether it’s on-shoring, reshoring, friend-shoring, however you want to view it, the increase in exports, there’s an implicit call for a lower value in our currency. It’s the only way we can go toe-to-toe. In our meeting earlier today, we were talking about the IMF comments that production costs and distribution of products globally dominated by the Chinese. The only way to compete with the Chinese is by devaluing your currency on a relative basis. So the most likely policy course remains a gradual erosion of our debt burden via inflation, real dollar weakening, and financial repression, which we’ve talked about previously.

Kevin: So back in 1980, and actually all the way up till just recently, the US Treasury, going and buying Treasuries would be like buying gold. That’s what people thought. Granted, we had inflation. But it is the stable trade. What you’re saying right now, especially with what the IMF is saying, is that maybe the US Treasury is not going to be the stable trade going forward.

David: Yeah. Whether it was viewed as the anti-fragile asset or a risk-free asset, the benchmark for risk-free returns— I read a Financial Times article, this is actually from the 23rd of February, titled, “The Haven Status of US Treasuries is Eroding.” And I think it tells the story well. It notes that Trump-induced geopolitical fragmentation, erratic policy shocks—including a tariff policy designed to hurt America’s friends more than its foes, a sustained assault on Federal Reserve independence, and neo-imperial threats to annex Greenland are but a few of the worries impacting the perception of the US Treasury market as a safe haven.

Kevin: Let me ask you, though, because you’re quoting the Financial Times, do you sense a bias in that article? They’re using imperialism, they’re using those types of terms. They’re not wrong in the degradation of the Treasury, but is it all Trump’s fault, or was this coming anyway?

David: Yeah, I think that there’s certainly a view from the Financial Times. We all have biases, and from their perspective there’s a number of things that they find distasteful, whether it’s the style of delivery, to use the word erratic. Well, that’s actually pretty accurate. I mean, from one day to the next—

Kevin: Last couple of months have been.

David: And if you look at March, April of last year, is it going to be a 50% tariff, 150% tariff, a 10% tariff? And now we’ve got tariffs off the table because of the Supreme Court ruling last week.

Kevin: And then the addition of the 10%.

David: At 10, but it’s going to be 15 if we get that approved.

Kevin: There you go. Yeah.

David: So there’s a dimension of, we just don’t know what’s next. And I think that the clear message is, whereas you in past times could look at the Treasury market as a safe haven, that is beginning to shift.

Kevin: Okay. And want to specify, too, we’re talking about longer term Treasuries, right? Short-term Treasuries are still probably one of the safest plays that you’re going to catch.

David: They’re almost a completely different asset class. The way they behave, the things that influence them, and how people even allocate them into a portfolio as a cash alternative or long bonds as a fixed income trade, very different in terms of the role that they play in a portfolio. So the article went on to say, “Donald Trump has come close to exploding one of the great myths of the investment world, namely that sovereign bonds are safe—risk-free assets.”

Kevin: And this is quoting the IMF.

David: No, from the Financial Times.

Kevin: From the Financial Times. Okay.

David: “And his second coming has contributed significantly towards undermining the role of US Treasuries as the world’s ultimate capital market hedge. Longstanding doubts about the continuing preeminence of the dollar as a reserve currency have intensified. Investors…” And I love this quote, “Investors have reshuffled the hierarchy of haven assets with the Swiss franc, Singaporean dollar, gold, and German bunds taking the lead in haven rankings.” The conclusion is that capital flows, although there is still money coming into the US, capital flows are seeking US exceptionalism within the equity markets.

Kevin: They like stocks, they just don’t like the bonds.

David: But more exposure, if you’re talking about the debt markets within Europe, where basically the judgment is, look, they’ve already dealt with Brexit. They’ve already done well working through the Greek debt crisis. So investors globally like the US income statement—this is the way it was described in the article—but not our balance sheet; but not our balance sheet.

So debt is suspect while US equities remain of interest. For how long, we can’t be sure because clearly the interest in the idea of exceptionalism, particularly within tech, you’re talking about the AI and tech narrative. And that’s drawn many a moth to the bright light of structural change, this revolution in AI. But maybe it’s moths to flame as a more accurate description. So the final note in that article is that “long bonds are at times more volatile than stocks”—to your point, the difference between short-term T-bills and long bonds. They say “de-dollarization will be a very protracted business. The lesson is simply that in capital markets, the concept of safety is strictly relative.”

Kevin: Well, and let me ask, when you’re running the race of who’s going to borrow from whom, it used to be the government’s really dominated that. But right now we’ve sort of got this shadow banking going on. You’ve got private debt markets that you really don’t know where the danger lies.

David: If you see credit expansion in recent years, and certainly in the last six to 12 months, in a huge way it’s been in the private markets. If you look at the loans extended, the growth in bank lending, as an example, very small relative to what’s happened in the private markets, private credit markets.

So within the credit market Olympics, if you will, private credit has pulled ahead. They’ve reigned as the unassailable, capturing greater and greater capital flows. And of course, that’s been at the expense of commercial banks and their loan books. Private credit has infused capital into tech and AI. And they’ve done it in a way that’s unbound by things that typically go with a loan arrangement—recurring cash flows, predictability of repayment—the normal baselines for bank lending. Private credit has to some degree been a derivation of an equity play on US tech exceptionalism.

Kevin: Okay. But there’s an assumption of liquidity there, and the ability to actually get to money. And this thing with Blue Owl just recently shows that maybe this narrative is fading and the liquidity is fading with it.

David: I went to a Jim Grant Conference in New York back in—

Kevin: October, I think.

David: Well, this was 2022.

Kevin: Oh, okay.

David: And there was a gentleman speaking, I don’t even remember who it was. But he basically said the best days of private credit are already behind us.

Kevin: Wow. And that was four years ago.

David: So, early in his call, but it does take time for credit market dynamics to shift. And at that point there was still momentum in play. But I took a copy of that article, with permission from Grant, and passed it on to the investment advisory board of the local college where I’m one of the members, and just said, “Folks, this is an interesting insight. You’re wanting to build out more and more, chasing Yale, chasing some of the larger university pensions and endowment funds. You want a larger allocation to alternatives, specifically allocations to private equity and private credit. Just for your consideration, if he’s right and the best days are behind us, you’re making a judgment on future vintages on the performance of past vintages. And perhaps that’s not the way that we should be looking at this asset class.”

Now in recent weeks, you’ve got the AI narrative shifting, and with it the value of the trades all around it. Blue Owl captures the headlines last week. They suspended payments to investors indefinitely.

Kevin: Yeah.

David: Indefinitely.

Kevin: You can’t have your money. We don’t have it.

David: And that’s in response to redemption requests going through the roof. And what it reveals is a liquidity mismatch. The underlying assets, the loans, are not really liquid, and the cash they have on hand is not sufficient to meet the wave of redemption requests.

Kevin: I love how you said it’s a liquidity mismatch. That’s an interesting way of saying, “You cannot get your money back out.” That’s what you’re saying.

David: Yeah. Well, and it also speaks to the frailty of the structure. You can’t have certain products within an ETF because of the implied liquidity of the structure. You go to sell, and click the mouse, and it’s gone, except that the underlying assets might not have a two-way market.

And so the liquidity mismatch is the implied liquidity, what you assume is liquid, when actually it’s really not. And the whole notion of private credit is that you’ve bought yourself extra time, and you’re getting paid what’s called an illiquidity premium. You should be making more money on it because your money’s going to be tied up for three, four, or five years, and you can only have part of your money back on a quarterly basis requested in advance.

Kevin: But now it’s indefinite.

David: Yes.

Kevin: Now it’s indefinite.

David: So Blue Owl is—and again, this ties into AI in many ways. Blue Owl is in the process of walking away from a CoreWeave data center loan. CoreWeave builds all of their compute capacity with debt. And this is a problem. If Blue Owl is not going to provide the credit, they can’t build the data center. So CoreWeave’s under pressure as well. Other private equity companies are rushing to their client inboxes, sending messages of, “Don’t worry, we’re okay.”

Kevin: Doesn’t this sound like 19— Oh, no, no, let’s go back.

David: 2008?

Kevin: 2007.

David: 2007?

Kevin: Yeah, yeah.

David: Yeah.

Kevin: Where it’s like, “Don’t worry, everything’s going to be fine,” but it’s not.

David: Right. Well, the popular products of the time, 2008, 2009, and of course packaged in 2004, ’05, ’06, and ’07 were mortgage-backed securities and repackaged loans, collateralized loan obligations—CLOs, CDOs—

Kevin: And they were paying above market at the time.

David: Well, of course.

Kevin: Of course.

David: There was an illiquidity premium. You got to choose the kind of risk that you wanted, and there was an implied liquidity in the product, which ended up not being the case when you got to 2008—late 2008.

Kevin: But what you’re saying is there’s a connection to the AI narrative and this debt unraveling.

David: Within private credit, yeah. So if you have memories of the mortgage-backed securities crisis that triggered the global financial crisis—that’s 18 years ago now—the C-suite fire-stomping, it can actually be more of a cause for concern than calm. So the private equity guy is getting out and saying, “Hey, we’re okay. Don’t worry. We’re okay.”

That actually may have an unintended effect, like, “Wait a minute, we weren’t worried. But if you’re worried enough to send me an email saying, I shouldn’t be worried, maybe I should be worried, and I now am.”

Kevin: “Why don’t you just give me a little of my money now?”

David: Right. “I’ll just take a small amount.”

Kevin: Yeah.

David: Yeah. The interconnectedness of private equity, private credit, tech into AI is enough of a daisy chain to matter. And while most buyout firms have limited exposure to real estate, there is this added layer of exposure within the credit markets that has negatively impacted commercial real estate.

And so the same private equity groups that have—private credit, I should say—significant loans into tech and AI also have some exposures in commercial real estate. Not all of them. On average, probably 5% exposure to commercial real estate. But then when you go to a Blackstone, a Brookfield, a KKR, an Apollo, they’ve got real estate assets in the range of 20 to 40% of firm-wide assets under management.

So, commercial real estate, is it the canary in the coal mine? You’ve got a listing of Chicago offices that changed hands in the last quarter, selling well under previous purchase prices. I’m looking at the list now. 74% lower than the previous purchase price, 87% lower, 82.5% lower, 85% lower, 68% lower, 94% lower.

Kevin: So it’s either a bargain or it’s a free-fall.

David: Yeah. I mean, we’re talking about real money here, from 165 million at last purchase to the hammer price at 22. 51 million to four.

Kevin: Wow.

David: 377 to 85, 302 million to 45.

I mean, they’re great deals unless vacancy rates go even lower, which again ties back into AI.

Kevin: Yeah. See, that’s thing you’ve called it a daisy chain. Who would’ve thought that AI might be connected to commercial real estate collapse?

David: Notably, Anthropic CEO Dario Amodei predicts 50% of entry-level white-collar jobs will be impacted within the next five years.

Kevin: So possibly replaced.

David: Well “Impacted” is one way of saying it. Probably a 14 to 30% disruption or complete displacement in total. Talk about deflationary.

Kevin: Wow.

David: So particularly for commercial real estate, maybe these are sensational prices at rock bottom levels, and maybe the revolutionary nature of AI is jobs-negative at a scale we care not to imagine, right?

So leaving some commercial real estate, I mean, can you imagine having commercial real estate with a negative value when you factor in the taxes and insurance that you have to pay? Go to a place like New York City. Oh, you think real estate taxes are going down? Not anytime soon.

So your cost to carry, it doesn’t matter what you paid. The question is how much do you have to continue to pay in hopes that you can actually improve your vacancy rate, or your occupancy rates?

Kevin: It’s like during the Great Depression, a person could own their land but not be able to pay their taxes on the land. Just the cost of owning it costs a lot of people a lot of money.

But we’ve talked before, 2007. 2007, Bear Stearns came out and tried to sell bad debt. It was not that big a deal. It was 400 million, but that was the canary in the coal mine. So my question is, is this the canary in the coal mine? I mean, Mohamed El-Erian?

David: Mohamed El-Erian ran PIMCO following Bill Gross’s tenure there, and with reference to Blue Owl, he posted on X, “Is this a canary in the coal mine moment?”

Kevin: Yeah. I wonder.

David: Speculating, “does this further erode investor confidence in credit vehicles, judging by the share performance of the large private equity firms?” So we go back to the Ares, the KKR, the Blue Owls, they’re down 16 to 20% year to date.

Kevin: Somebody knows something.

David: And they’re off 40 to 50% from peak levels last year. So you have to wonder, alongside El-Erian, Blue Owl is now down 60% from its peak, and it’s still sports a price earnings ratio of 101. Texas Pacific Group, TPG, they’re off 40%—the equity is—to trade at a price earnings multiple of 94. Right? So the share price is down 40 to 60% for these firms, and yet they’re still priced like—

Kevin: I’m thinking maybe these aren’t canaries, these are ostriches in the coal mine.

David: Ponder that. Major price corrections, and they’re still asking investors to pay upfront for nearly a century of yet earned income. That’s a little rich.

Kevin: Yeah.

David: And they were even richer. So again, KKR, Ares, Blackstone, Apollo, judging by their share prices, you could say the golden age of private equity is indeed over. And to get to a more modest P/E, earnings need to quadruple—

Kevin: Wow.

David: —or share prices fall by an additional 50 to 70%.

Kevin: Wow.

David: Also worth noting that the folks who’ve populated this space for a long time, again, in the world of institutional money management or pensions, endowments, these are the alts, the alternative investments. So you’ve got your traditionals, which are, again, publicly traded stocks, bonds, then your alternatives give you a range of things. Very rarely does gold hit that list of alternatives.

Kevin: Right.

David: But Princeton and Harvard are both significantly shrinking their exposure to private equity and private credit. This is an allocation shift that hasn’t occurred at this scale in decades.

Kevin: Well, and again, going back to 2007, 2008, there were some who were too big to fail and were bailed out. There were some who were not. But private credit and private equity is not something that’s probably going to be bailed out by the public—I don’t think, do you? I mean, could you see a Blue owl or a KKR being bailed out by you and me, the taxpayer?

David: Anything’s possible. Friends are friends. It’s not what you know, it’s who you know.

Kevin: Yeah. Trillions are trillions.

David: If you went to the right school, maybe you’ve got the right Rolodex. I don’t know. When you review Doug Noland’s periphery to core framework, you’ve got issues that emerge in the credit markets in higher risk areas, kind of at the periphery of the markets, and then move towards the lower risk center as risk intensifies, as liquidity dynamics shift.

Kevin: As it moves toward the core.

David: Yeah. And those liquidity dynamics, they flag emergent issues. Price volatility, discounting of assets, that is a flag of emergent issues. Gating, like the Blue Owl fund, flags an emergent issue. Again, at the periphery, how much does it move to the core? Private credit is really just non-publicly traded junk debt. That really is at the periphery of the credit markets. It’s only accessible if you wear the right kind of bow tie or you wear bespoke shoes and a nice tailored suit. I mean, it’s not accessible to everywhere. It’s institutional access, primarily.

Kevin: Right.

David: And they’ve only just recently opened up a few funds that an individual investor can buy in the form of an ETF. Or maybe you want exposure to all of those assets in a direct investment in Blackstone’s publicly traded stock. Wouldn’t have treated you well over the last six months, but nevertheless—

Kevin: Right.

David: —that’s removed to some degree. Private credit is just non-publicly traded junk debt. So, no surprise that companies that have borrowed at rates north of 10%—I mean, we’re talking 10, 12, 14, 16, 18%—

Kevin: Isn’t there always a reason, when somebody says, “Oh, I’m getting double the interest that I could in your bank account or—”

David: Yeah, it’s an indication of risk.

Kevin: Always. You never get away with it, long.

David: As the creditor, you look and you say, and I see this with many novice investors, they’re like, look, I can get 12% over here. Yeah, you could also find 14 and 16% paper, do you understand the risks that you’re taking?

Kevin: Right.

David: Because you are, in essence, being compensated for a higher likelihood of default, and you have to factor that in. It’s not a free lunch.

Kevin: Right.

David: This isn’t that extra free money—

Kevin: And that’s the—

David: —above the risk-free rate.

Kevin: That’s the market. The market rate, if you’re getting double, you’re taking double the risk at least, yeah.

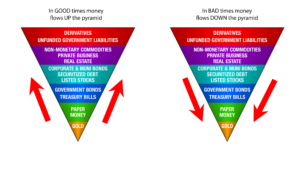

David: But those companies that are borrowing at 10, 12, 14%, they’re the first to be impacted by any slowing in sales or revenue. So again, that periphery to core framework, if you’re at the edge, you’re paying those high rates, you are the first to be impacted by anything that changes within the economy. How far it moves to the core remains to be seen, but I think that whenever you’re considering the periphery to core risk migration, it’s also worth keeping in mind John Exter’s inverted liquidity pyramid. He was at the Federal Reserve Bank of New York for a number of years. My dad knew him. And what he depicts in this inverted pyramid is basically that in good times money flows up the pyramid. And again, the base is at the top going down to-

Kevin: It’s inverted, yeah.

David: It’s inverted .

Kevin: Yeah.

David: Derivatives, unfunded government liabilities. Move down a notch: non-monetary commodities, private businesses, real estate. Then you move to corporate and municipal bonds, securities, listed stocks. Then you move to government bonds and Treasury bills. Then you move to paper money, and then at the very—

Kevin: And then you move to gold.

David: Then you move to gold. So in good times, money flows up the pyramid towards high-risk assets, in bad times, money flows down the pyramid towards assets that don’t have liabilities attached to them. They’re not encumbered. I think these two things marry very well, the periphery to core migration and the inverted liquidity pyramid. Markets under pressure do precisely what the Financial Times article I previously mentioned, described. Investors are reshuffling the hierarchy of haven assets, and they’re going for the gold. Sorry, the Olympics are back and—

Kevin: I was going to say, just like the Women’s Canadian team.

David: No, they went for the silver.

Kevin: Yeah, yeah. But just like the women’s US team went for the gold—

David: Yeah.

Kevin: And the men’s team went for the gold, I guess the message, like you said, is go for the gold.

David: Reshuffling the hierarchy of haven assets and going for gold.

* * *

You’ve been listening to the McAlvany Weekly Commentary. I’m Kevin Orrick, along with David McAlvany. You can find us at mcalvany.com and of course you can call us, at (800) 525-9556.

This has been the McAlvany Weekly Commentary. The views expressed should not be considered to be a solicitation or a recommendation for your investment portfolio. You should consult a professional financial advisor to assess your suitability for risk and investment. Join us again next week for a new edition of the McAlvany Weekly Commentary.