More

Presented by Doug Noland since 2012

* * *

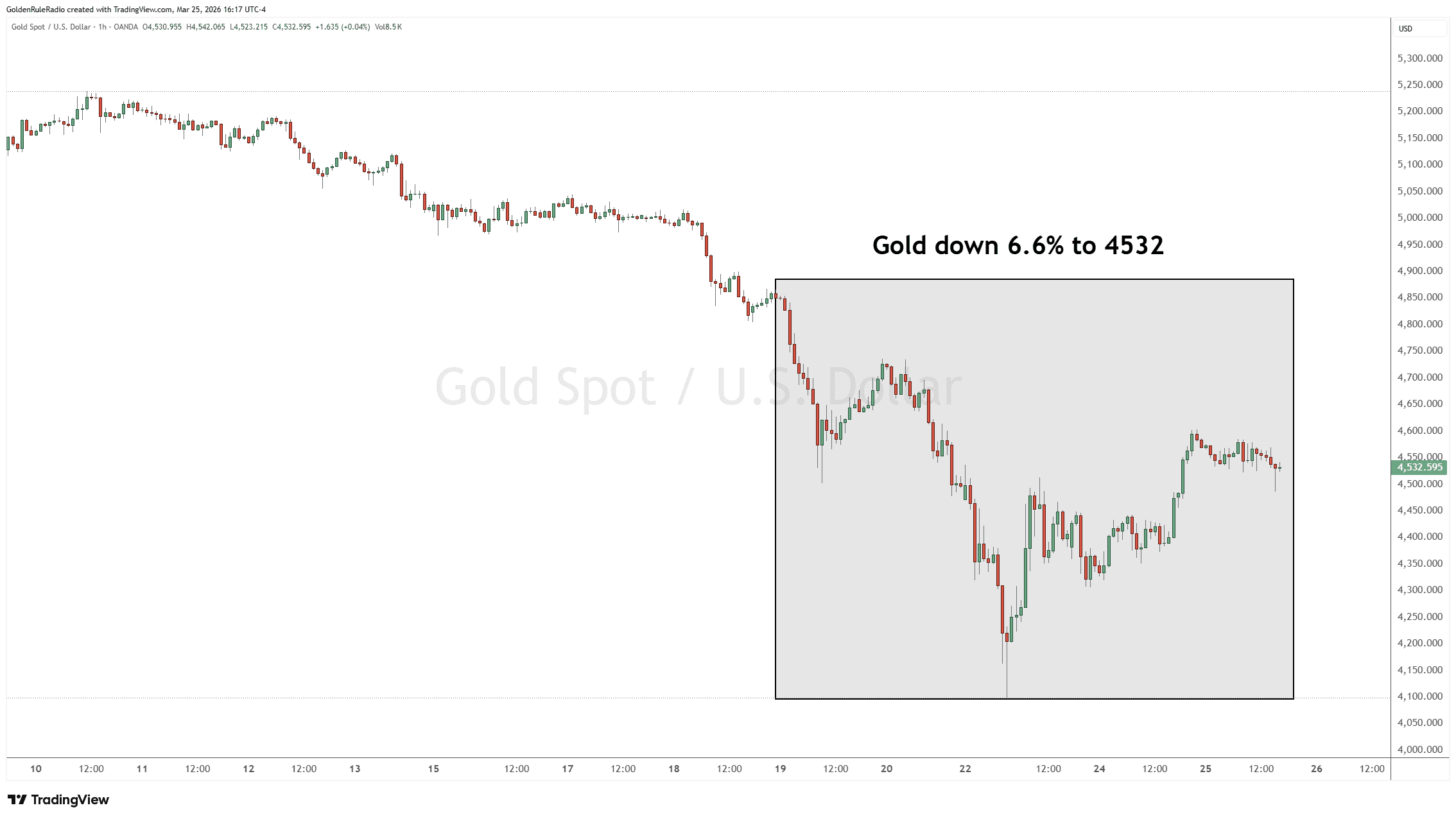

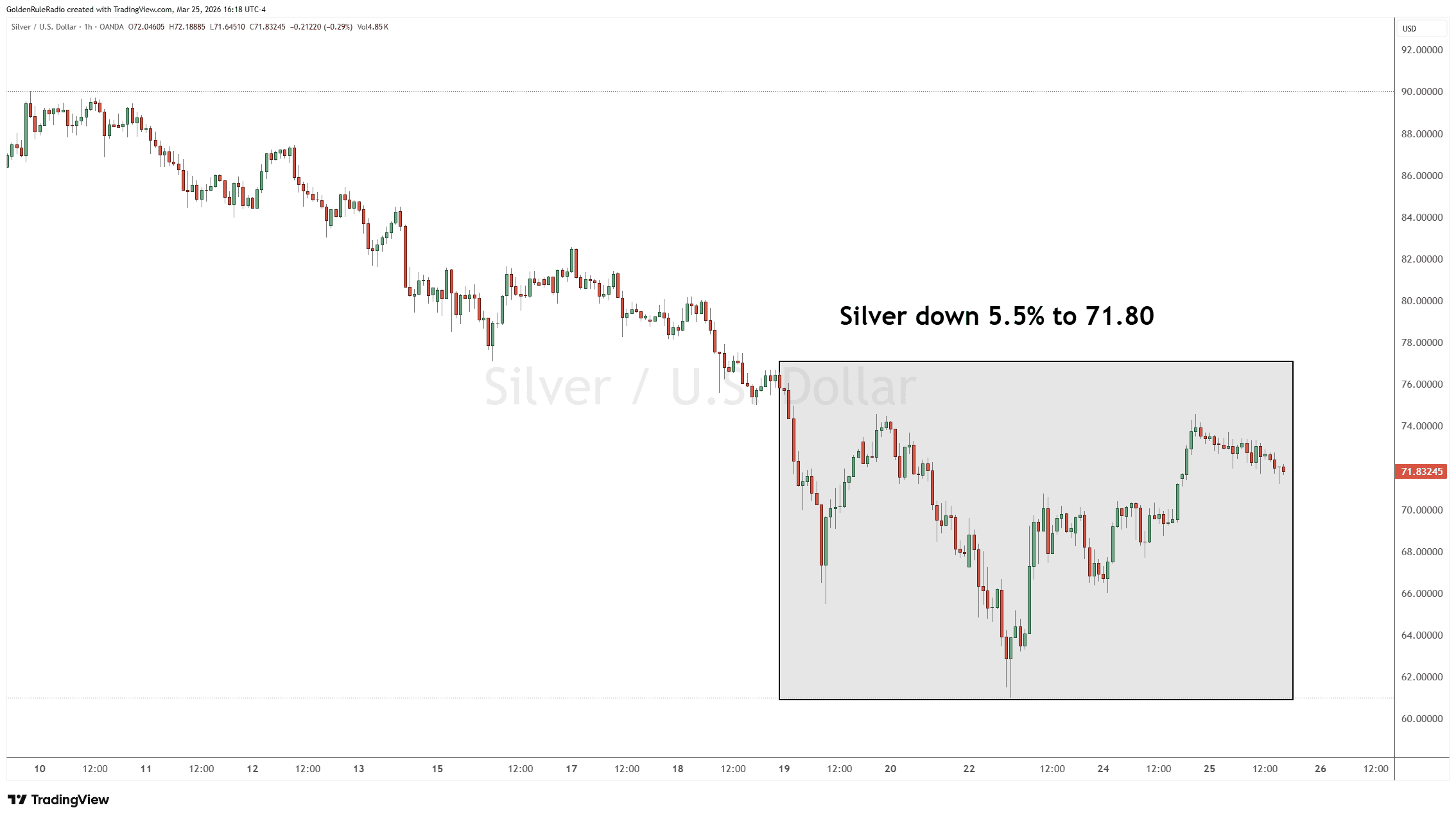

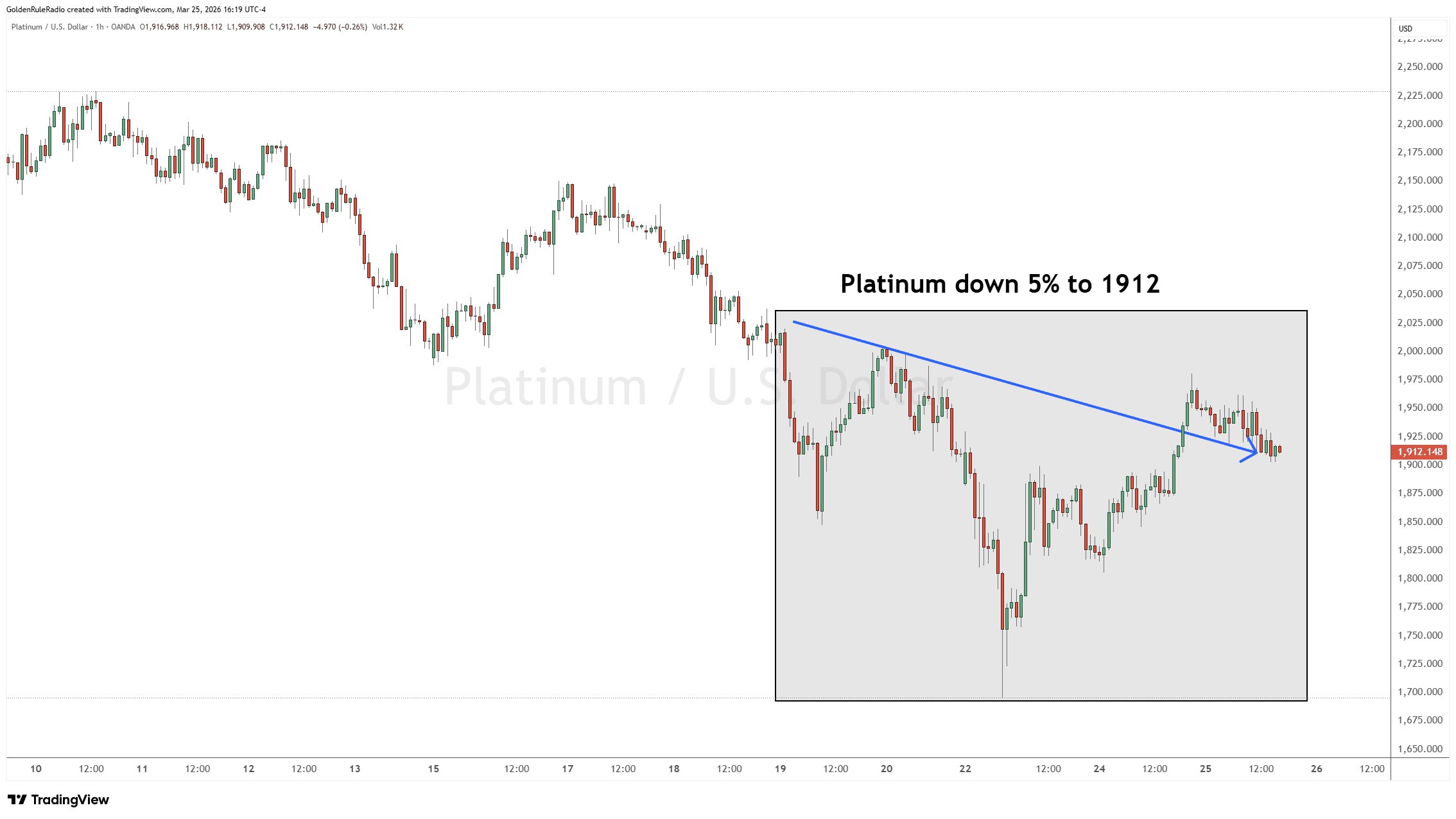

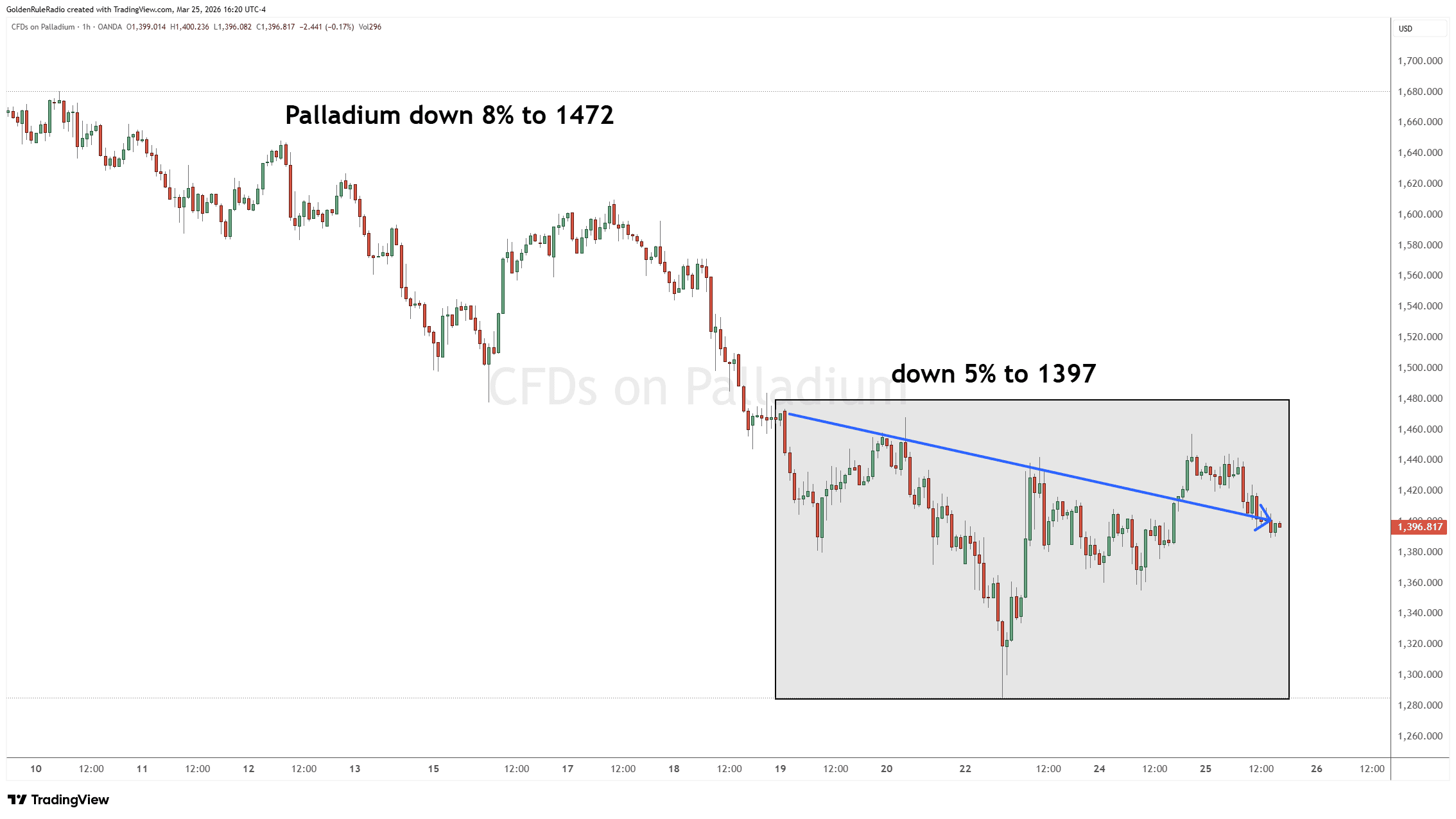

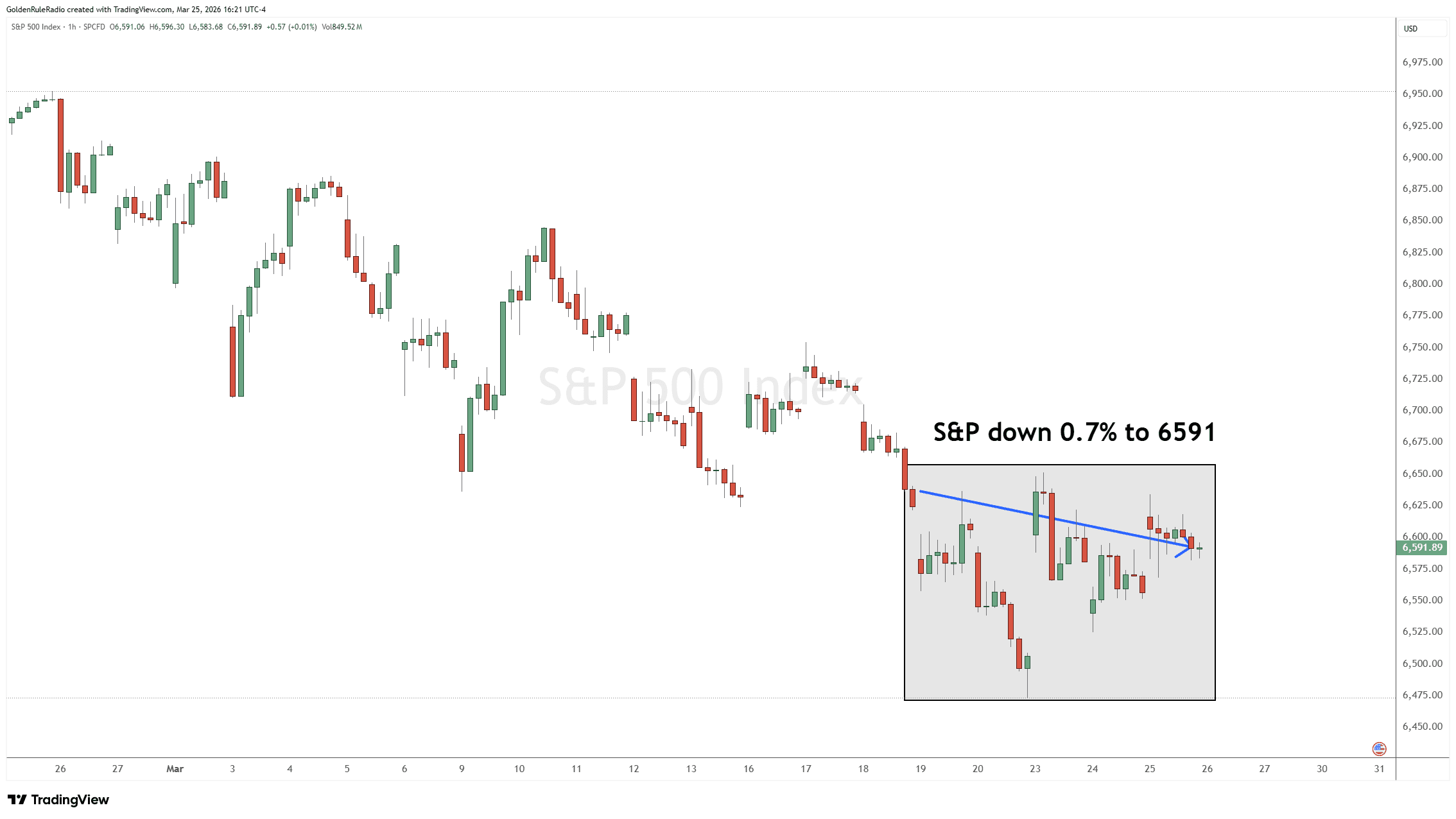

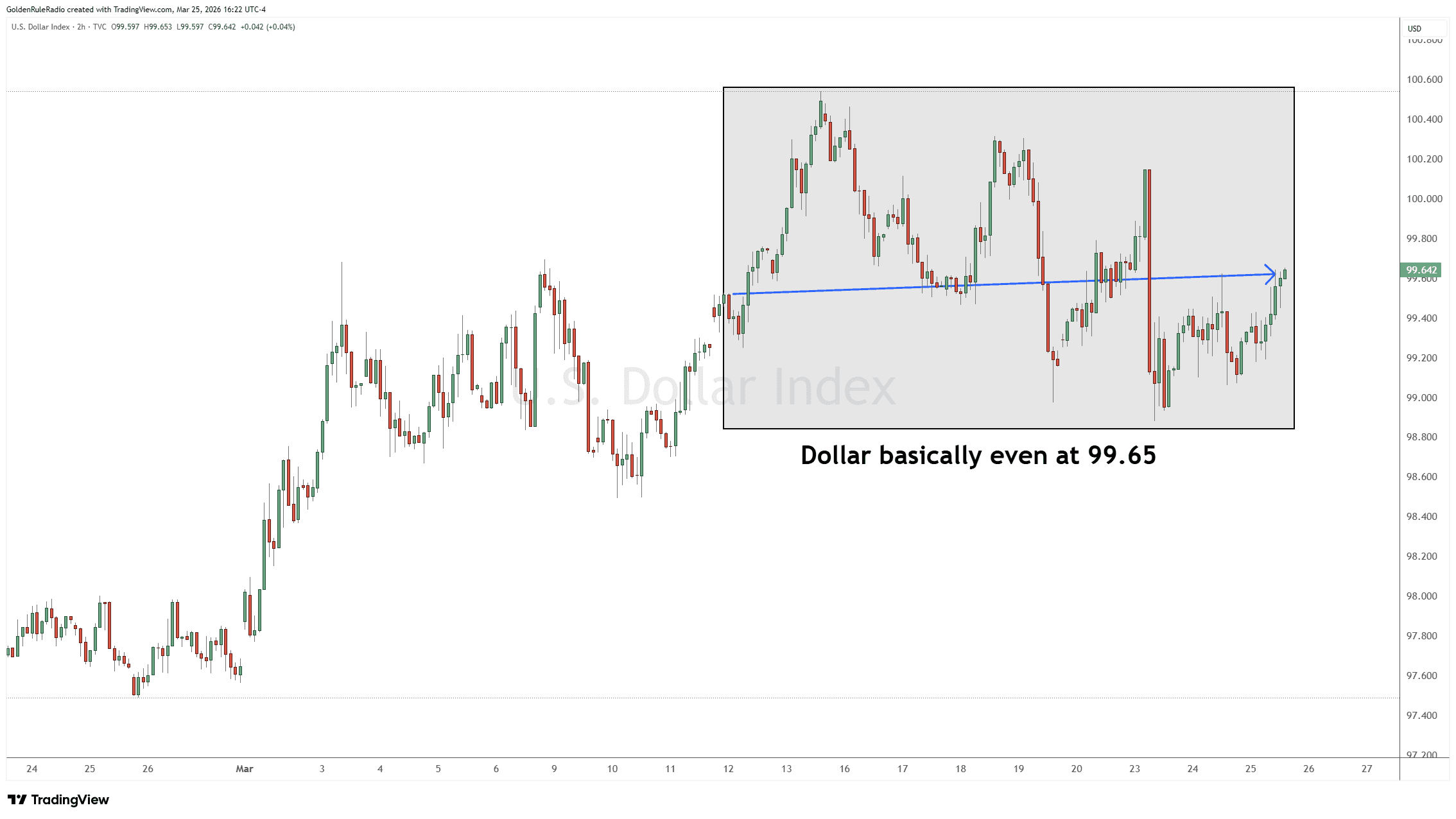

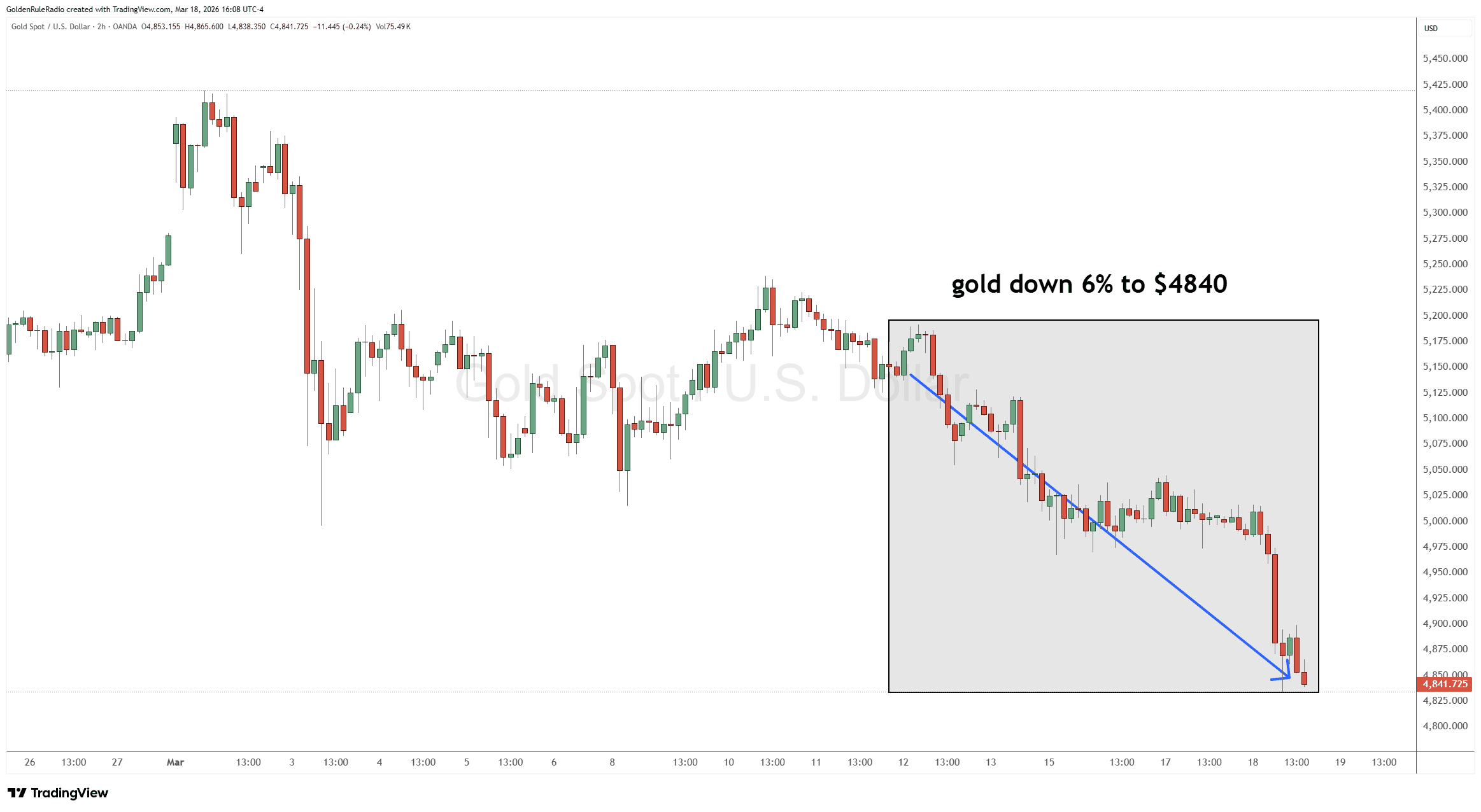

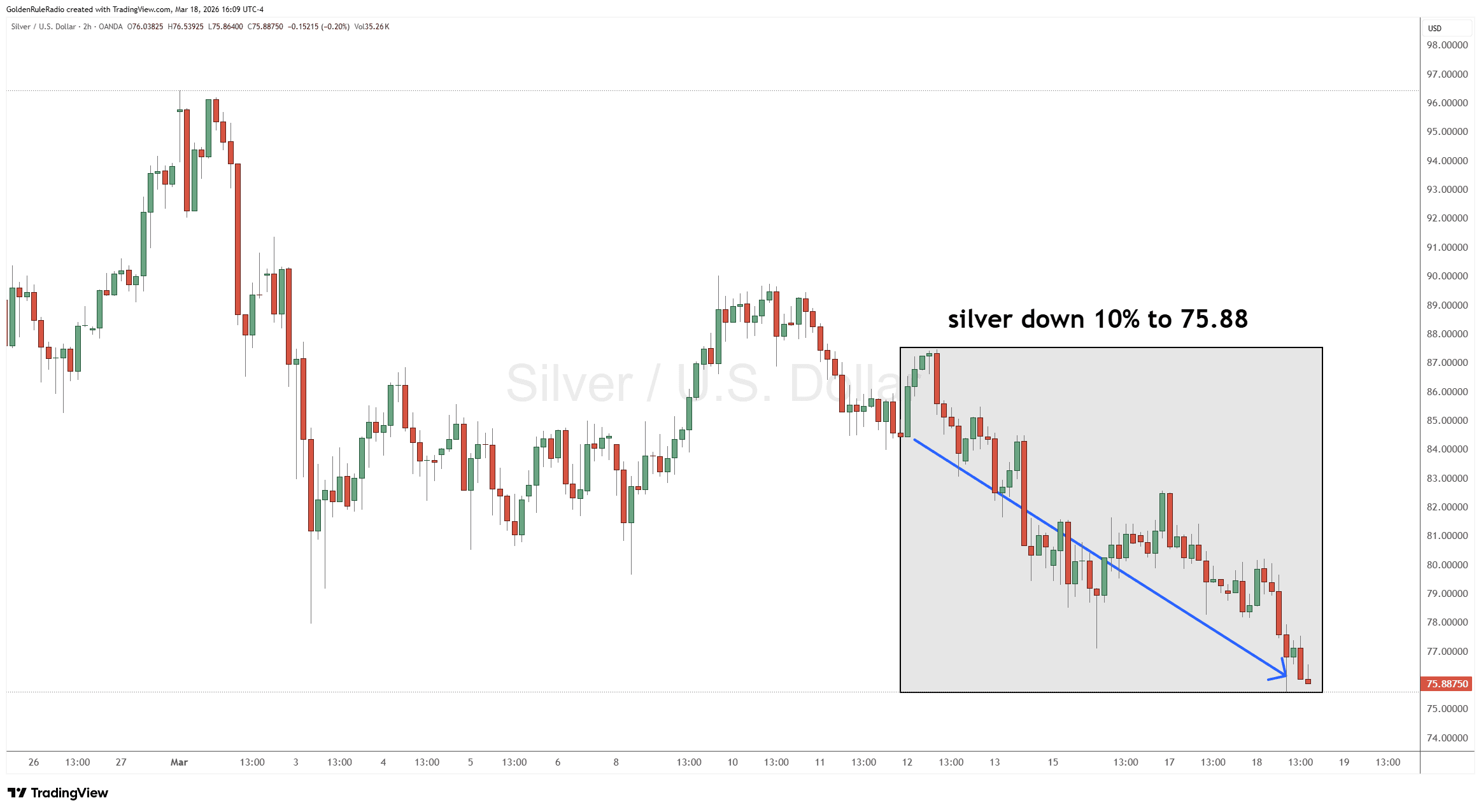

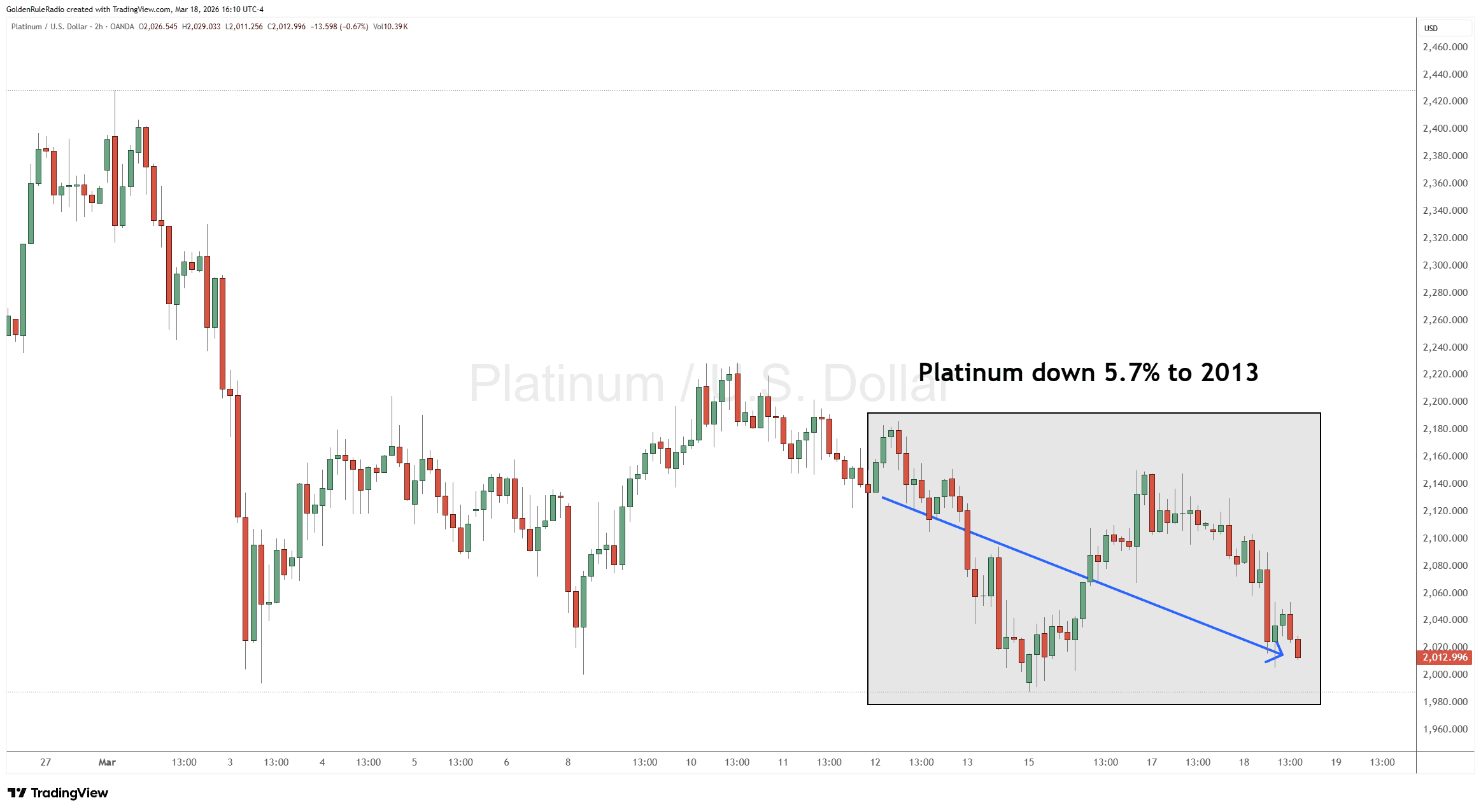

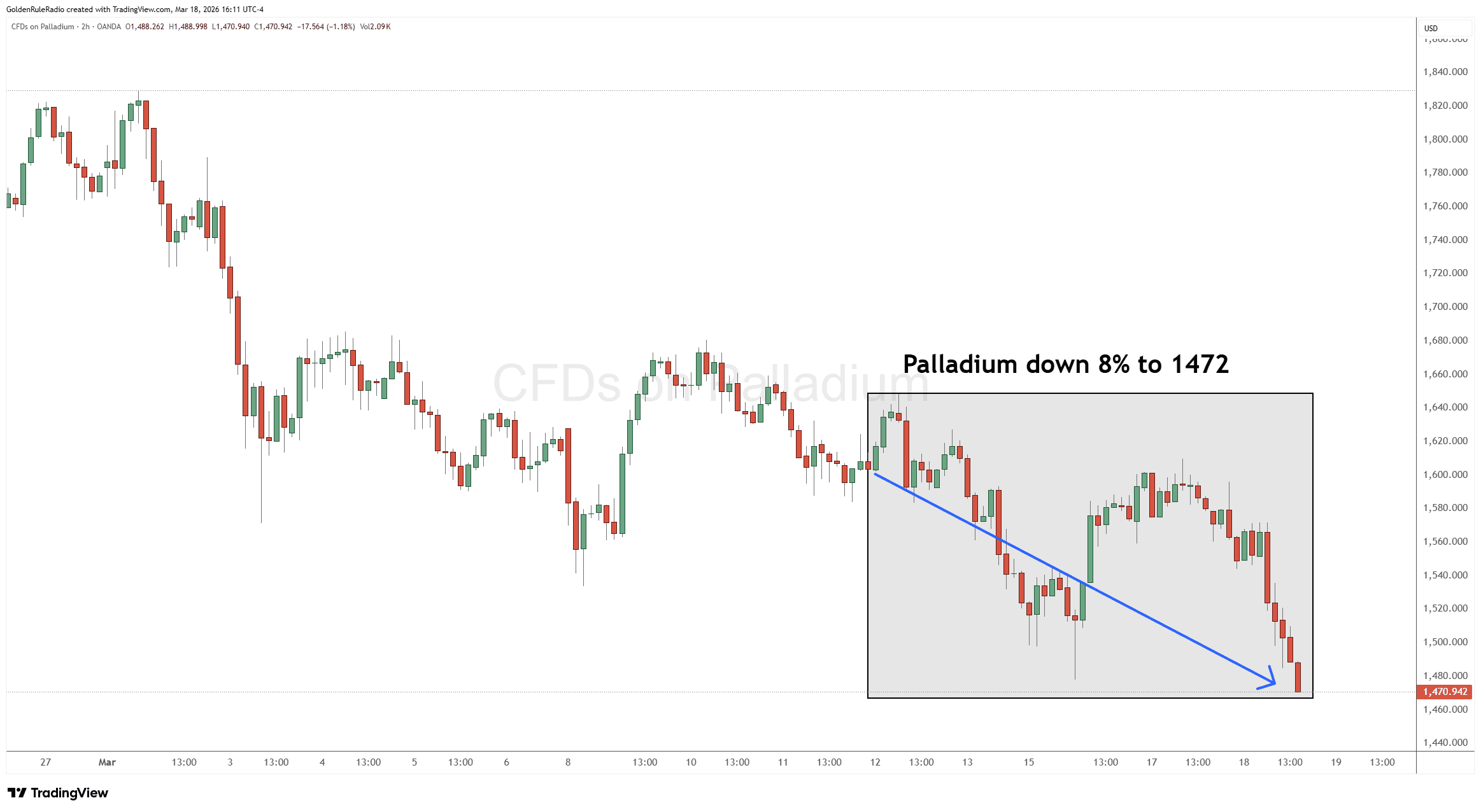

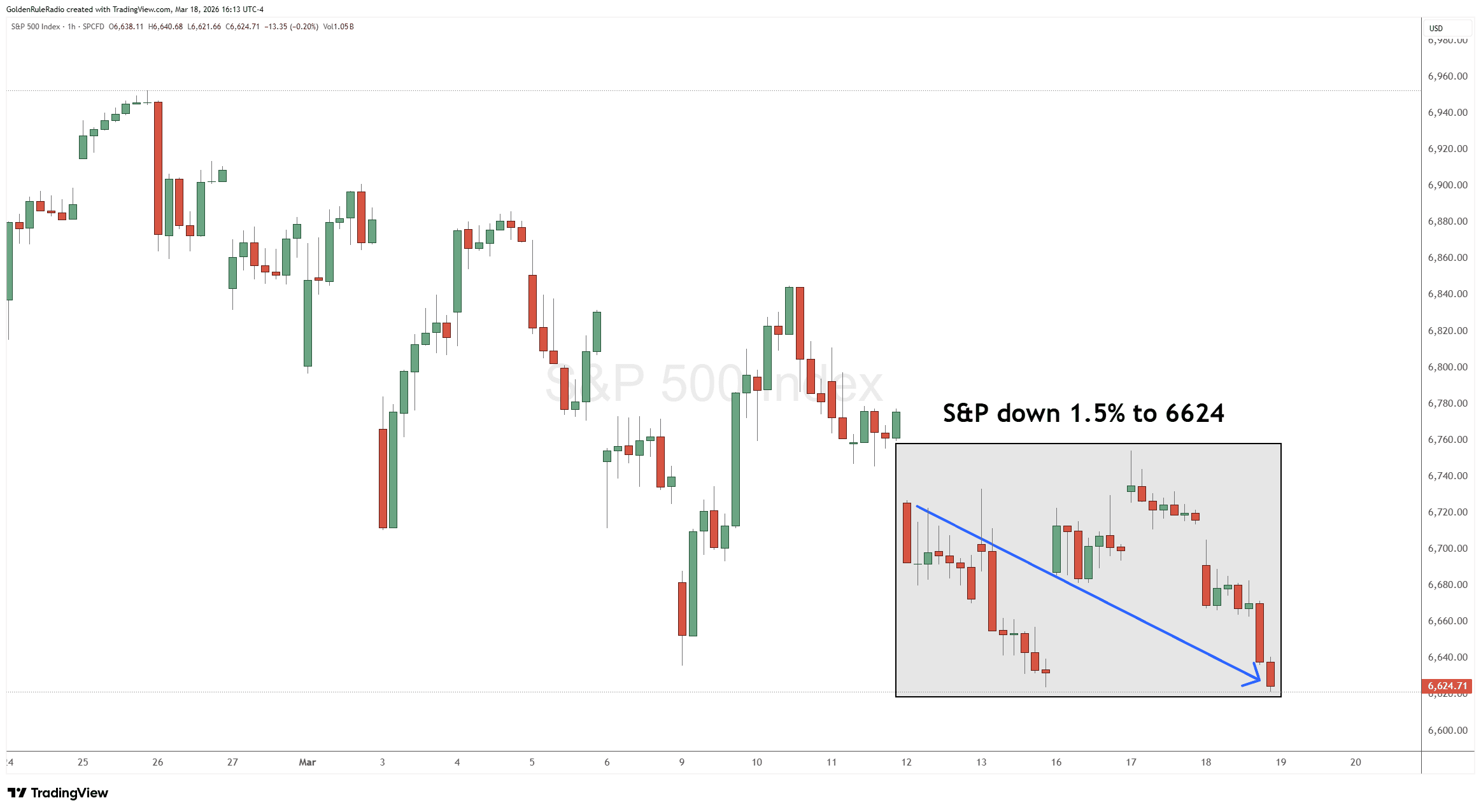

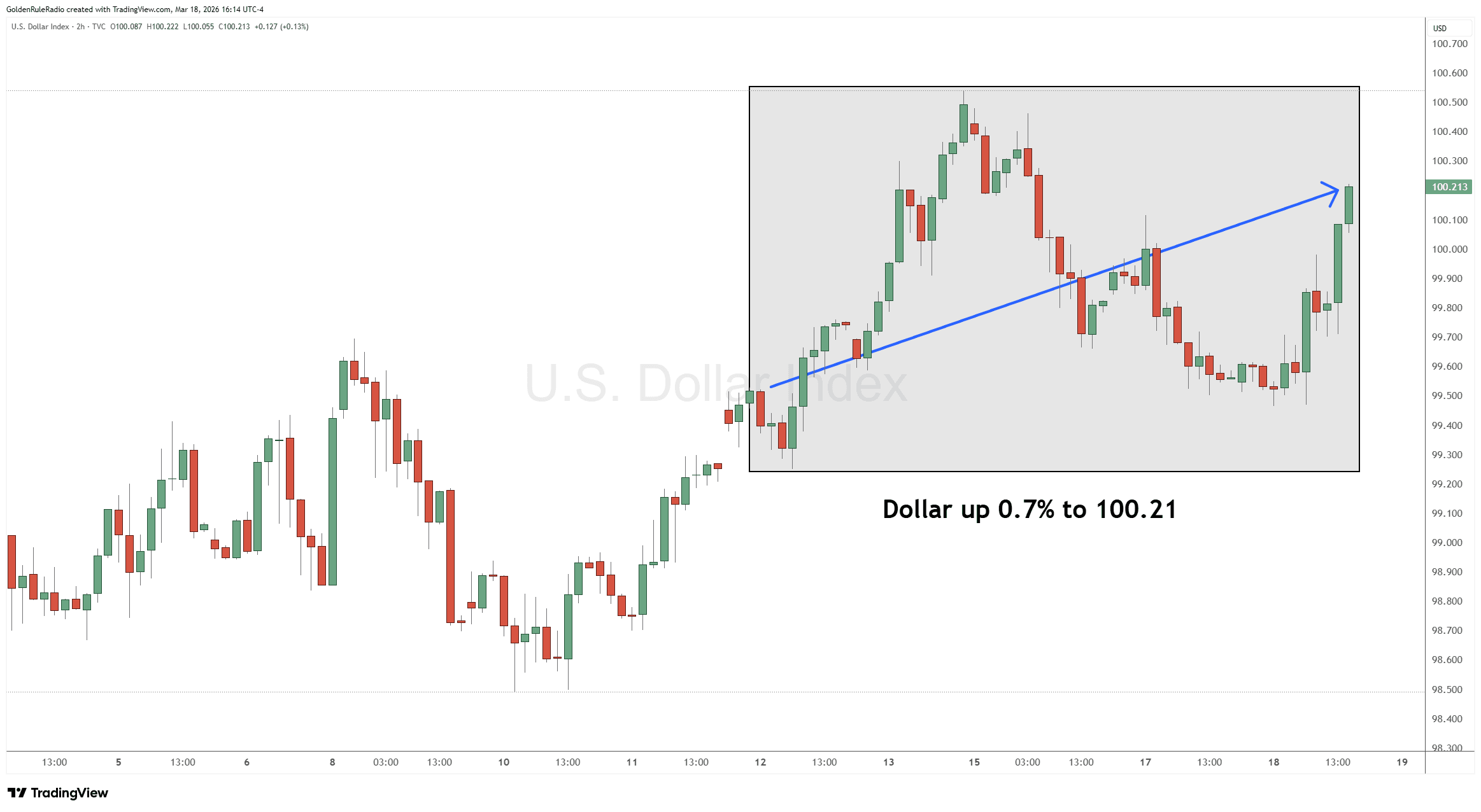

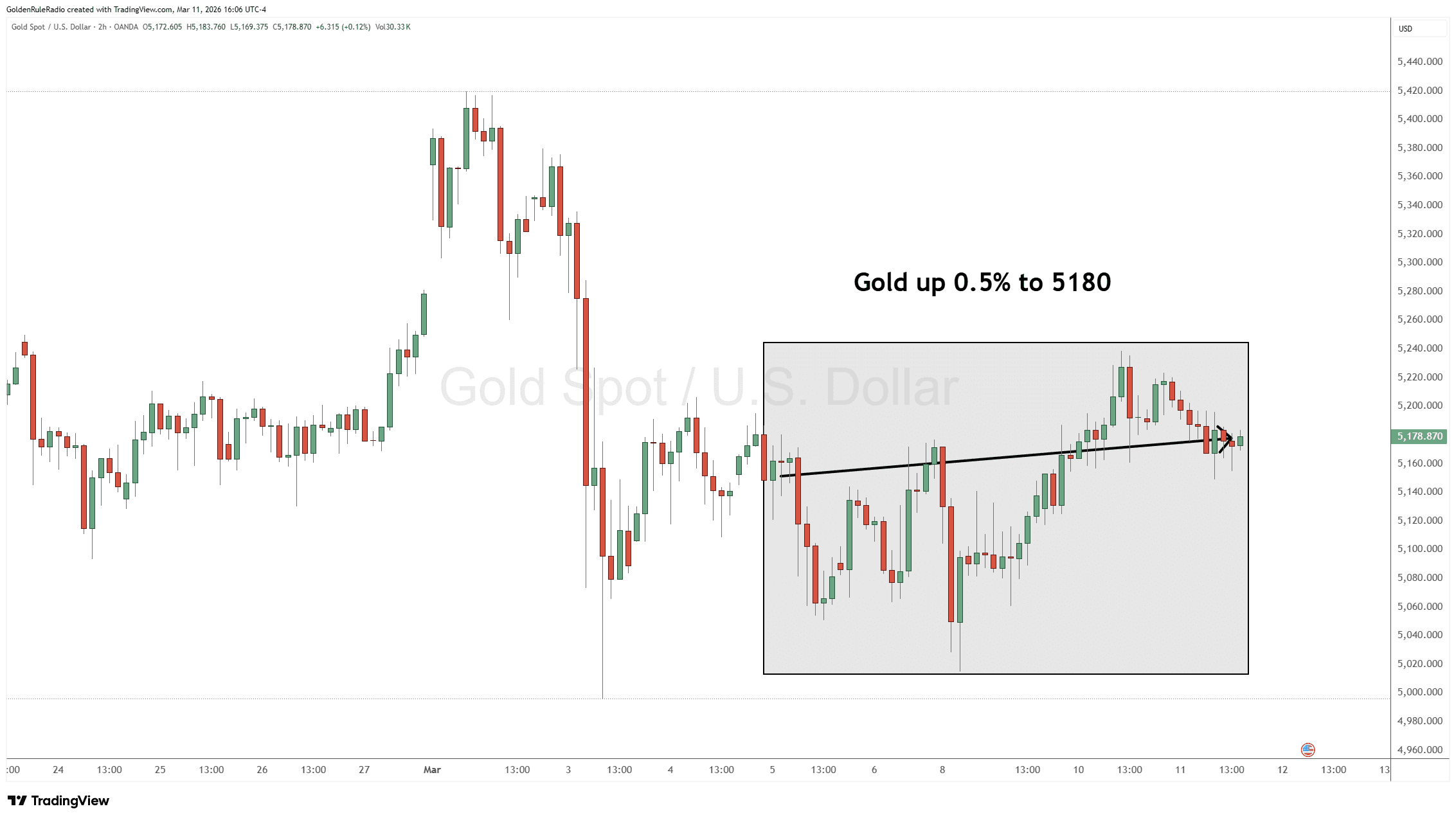

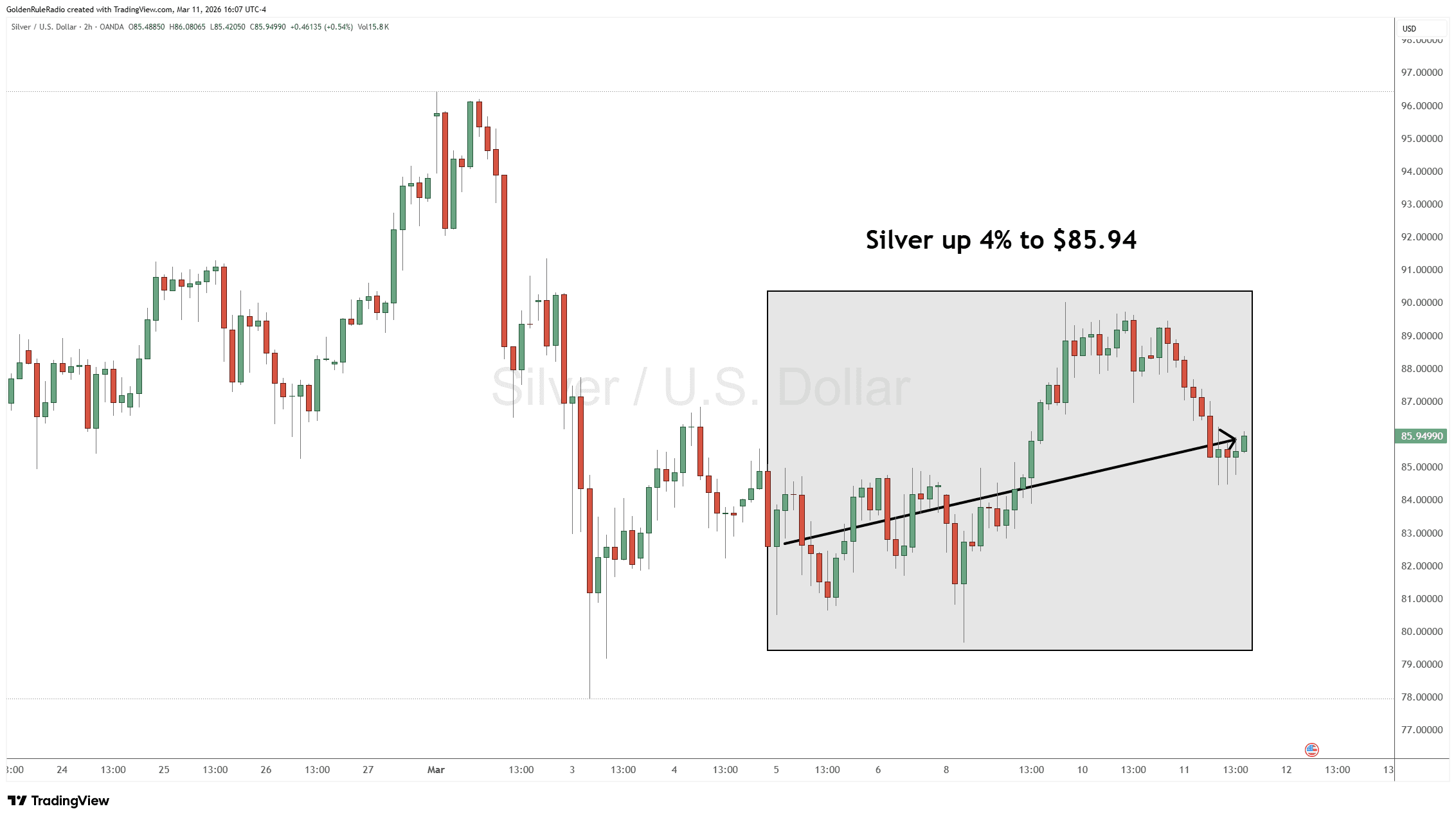

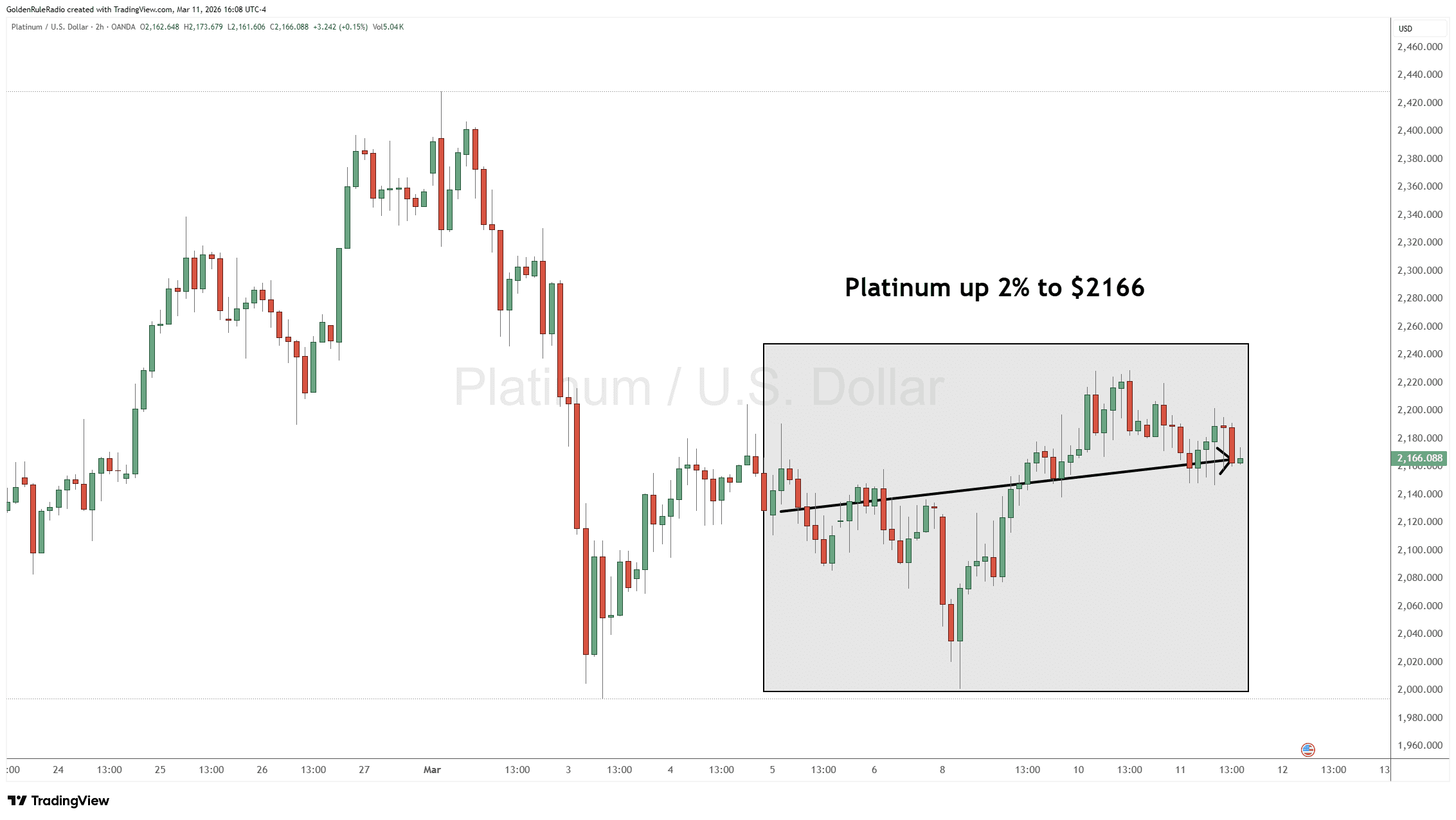

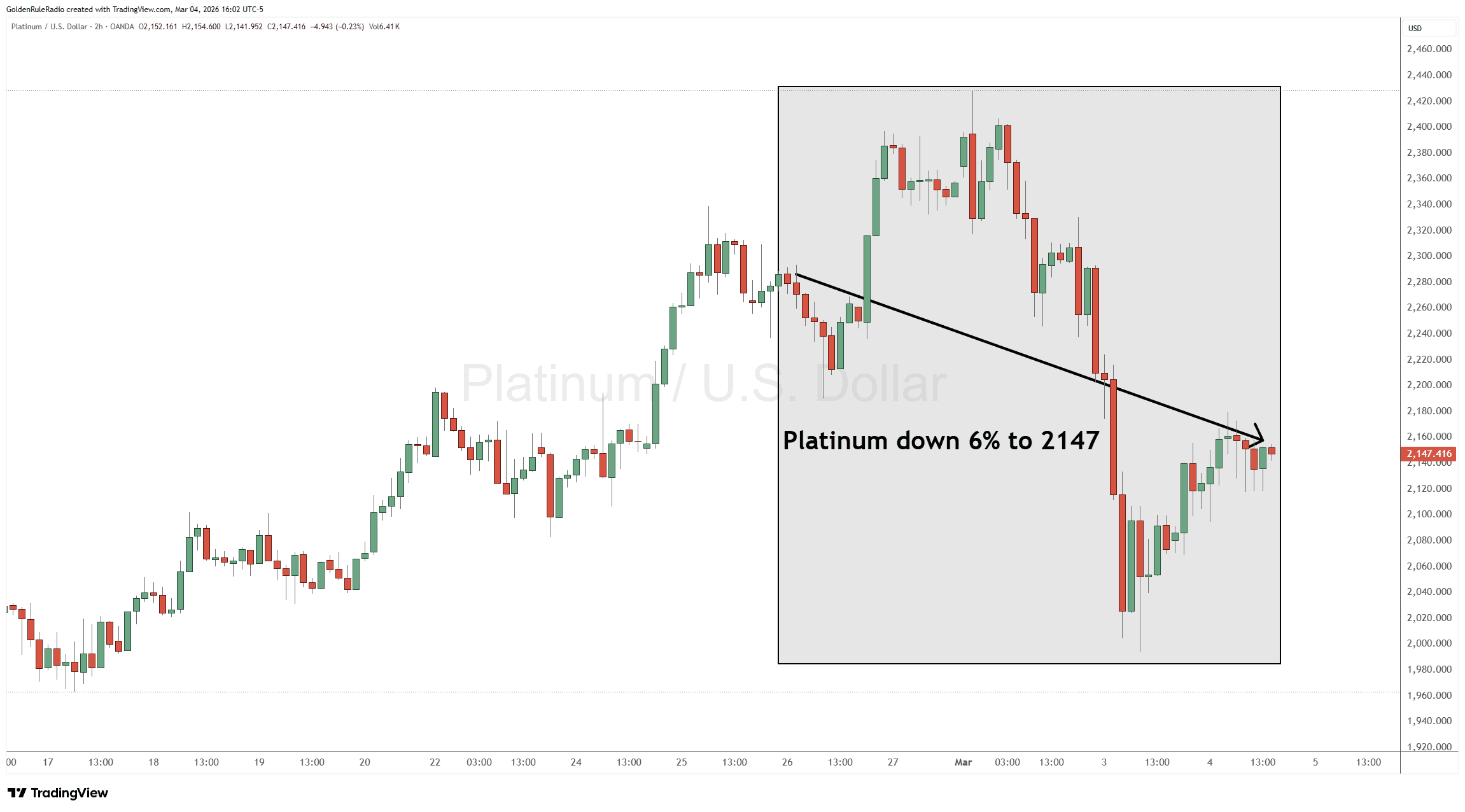

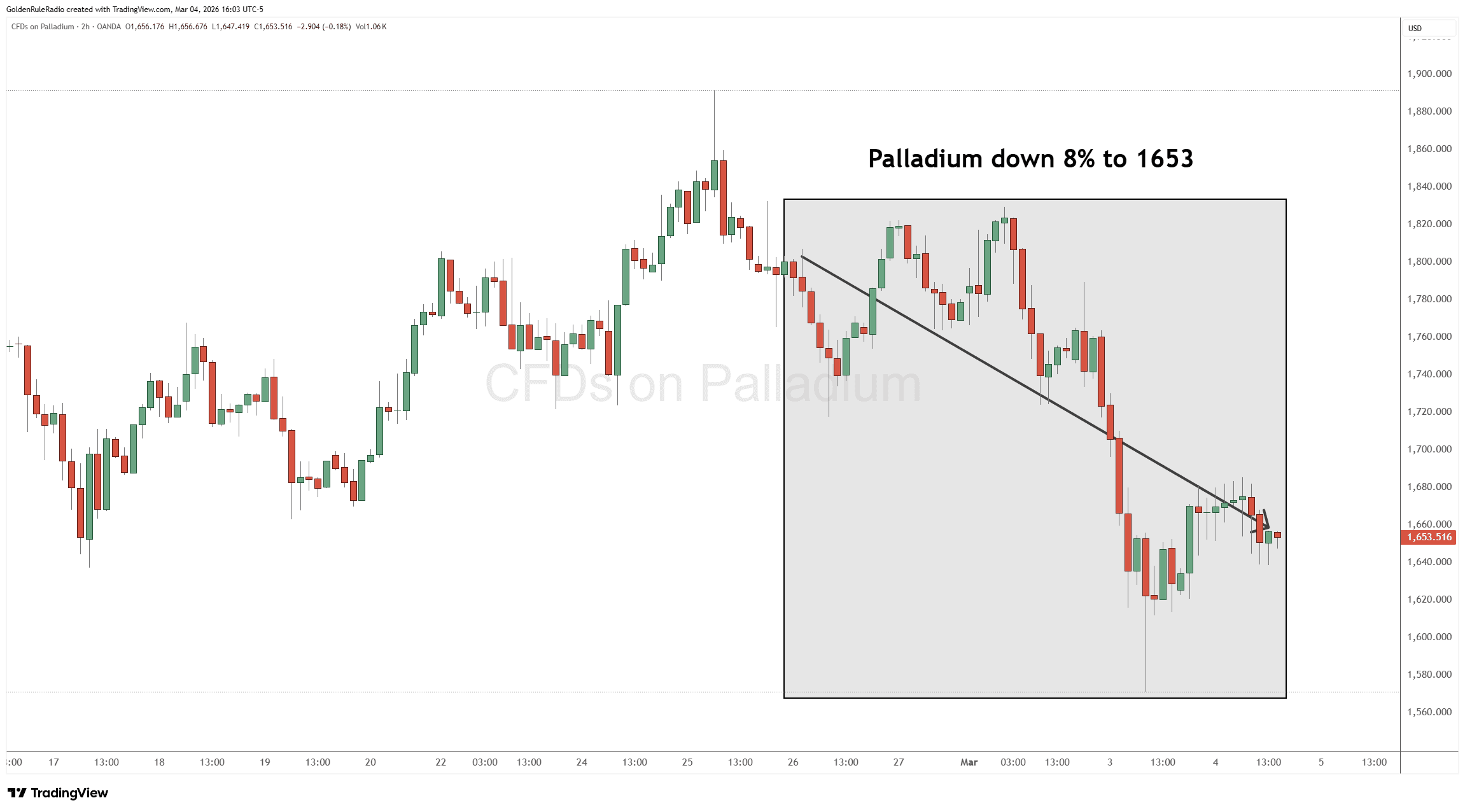

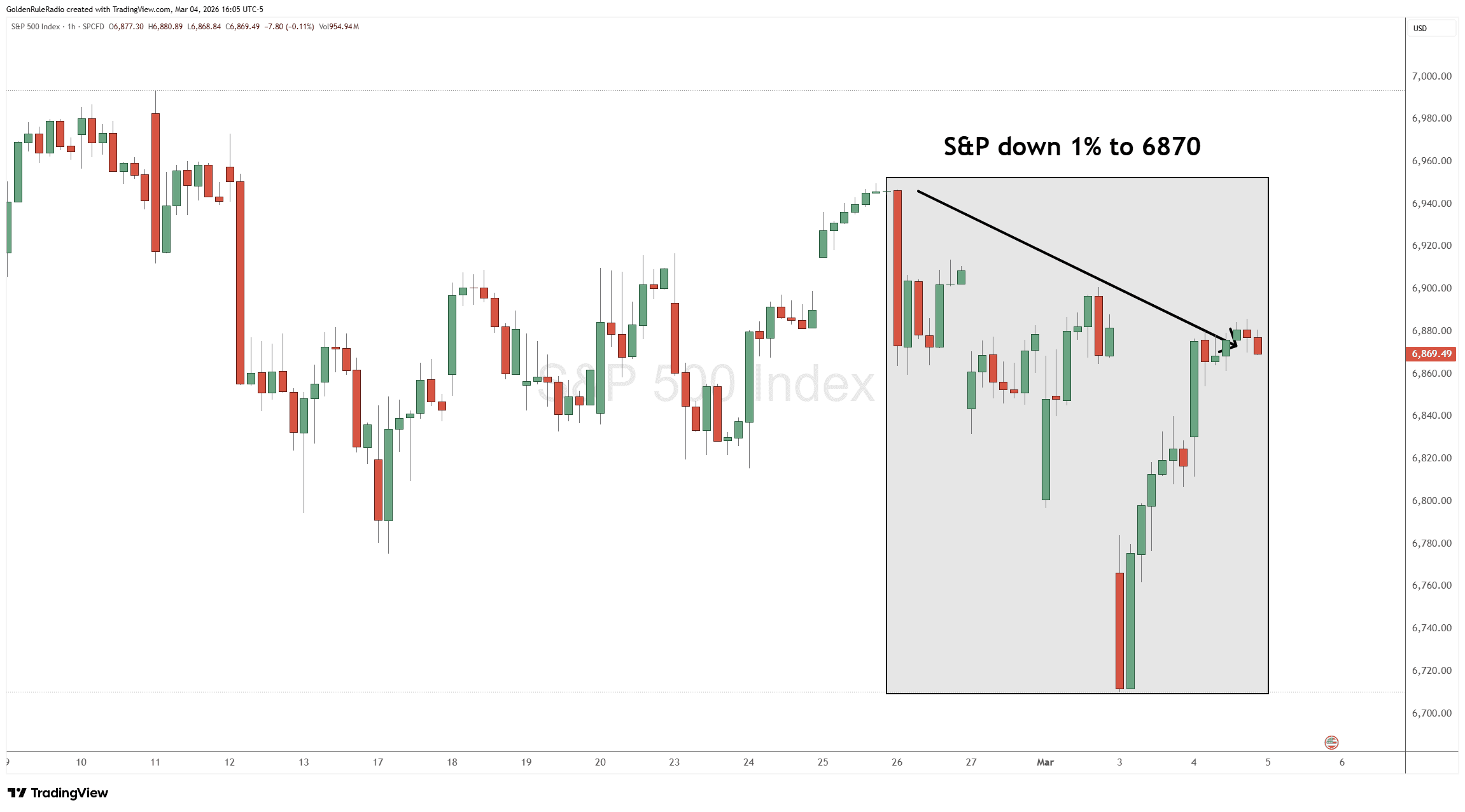

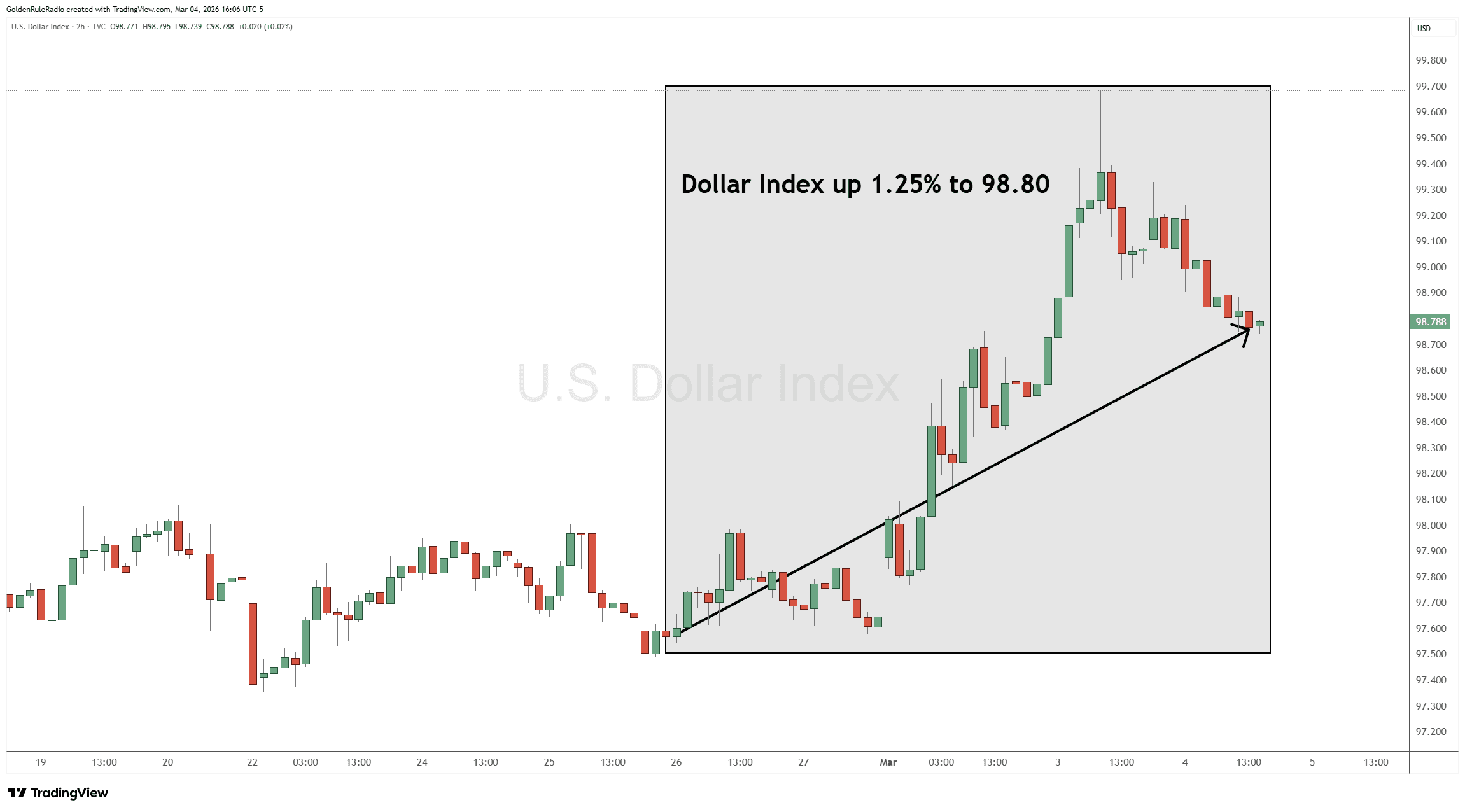

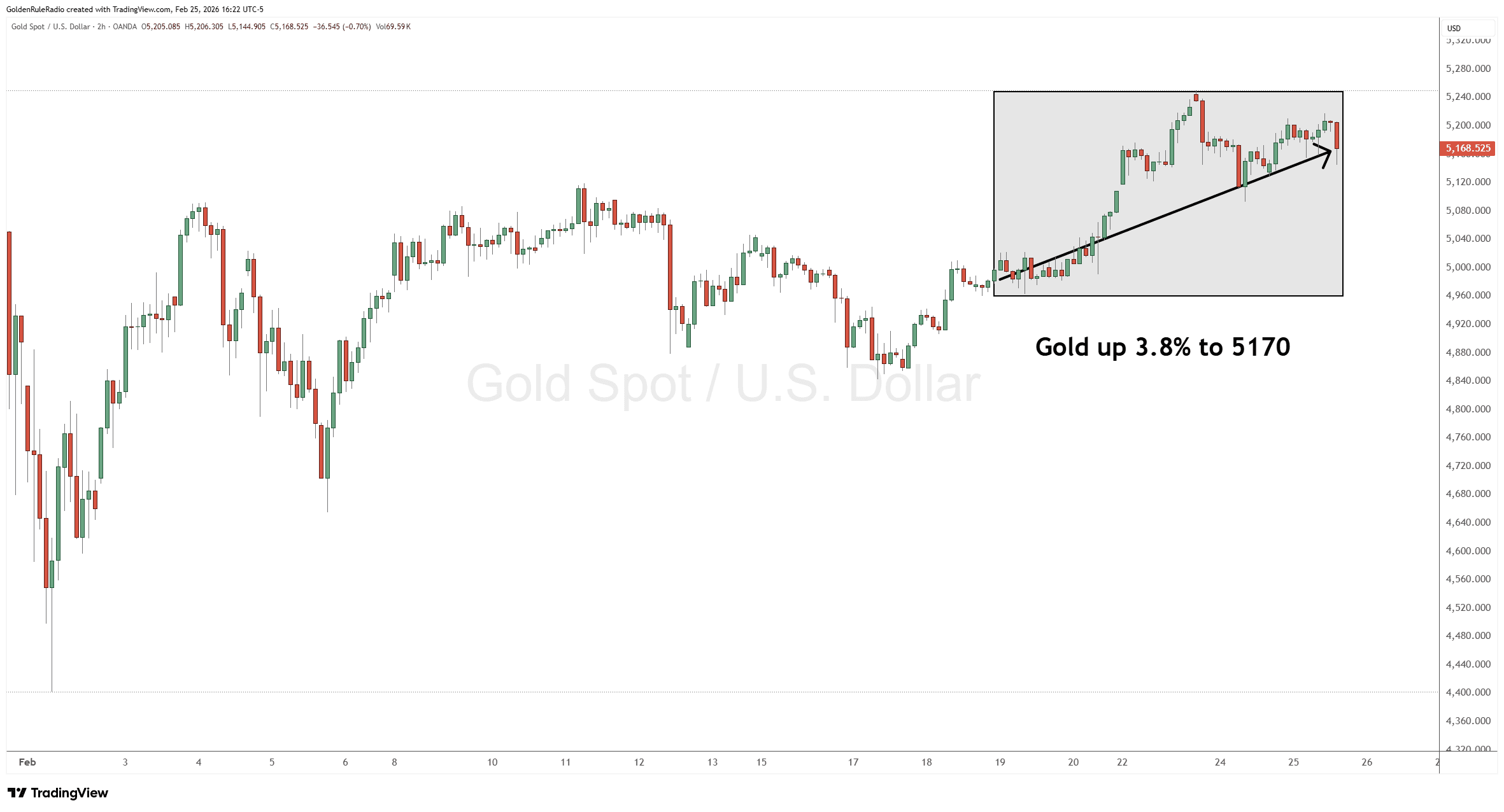

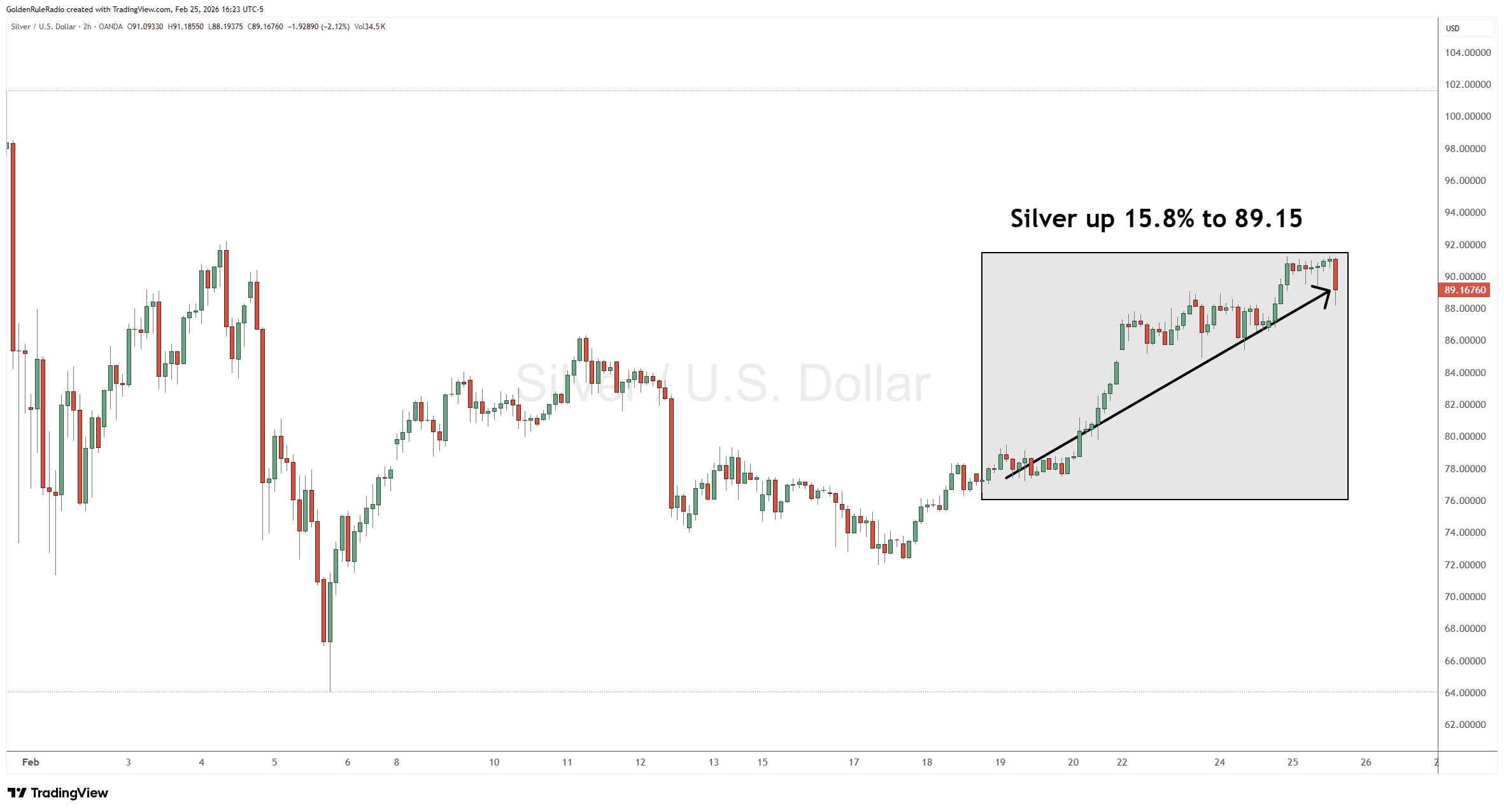

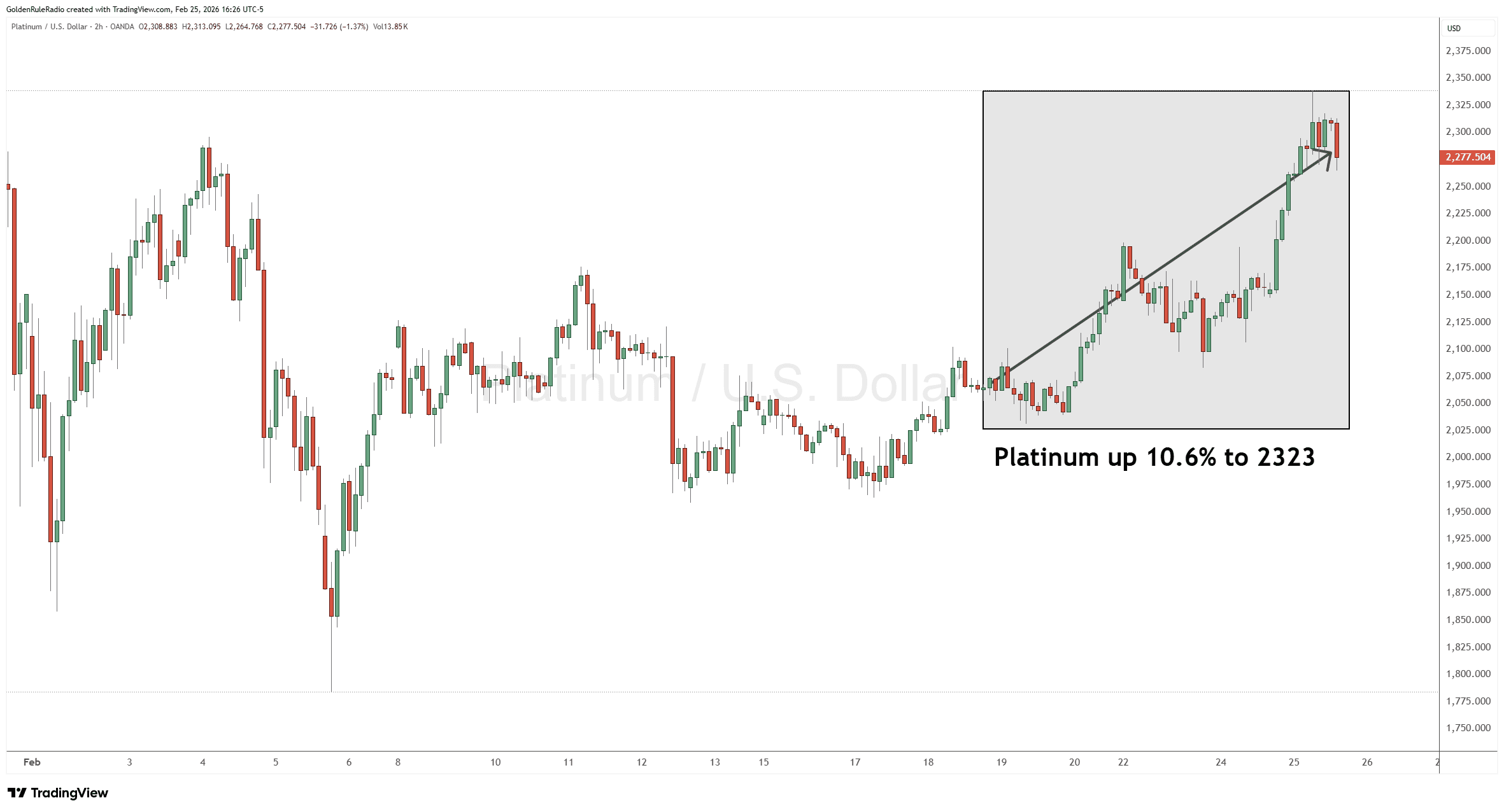

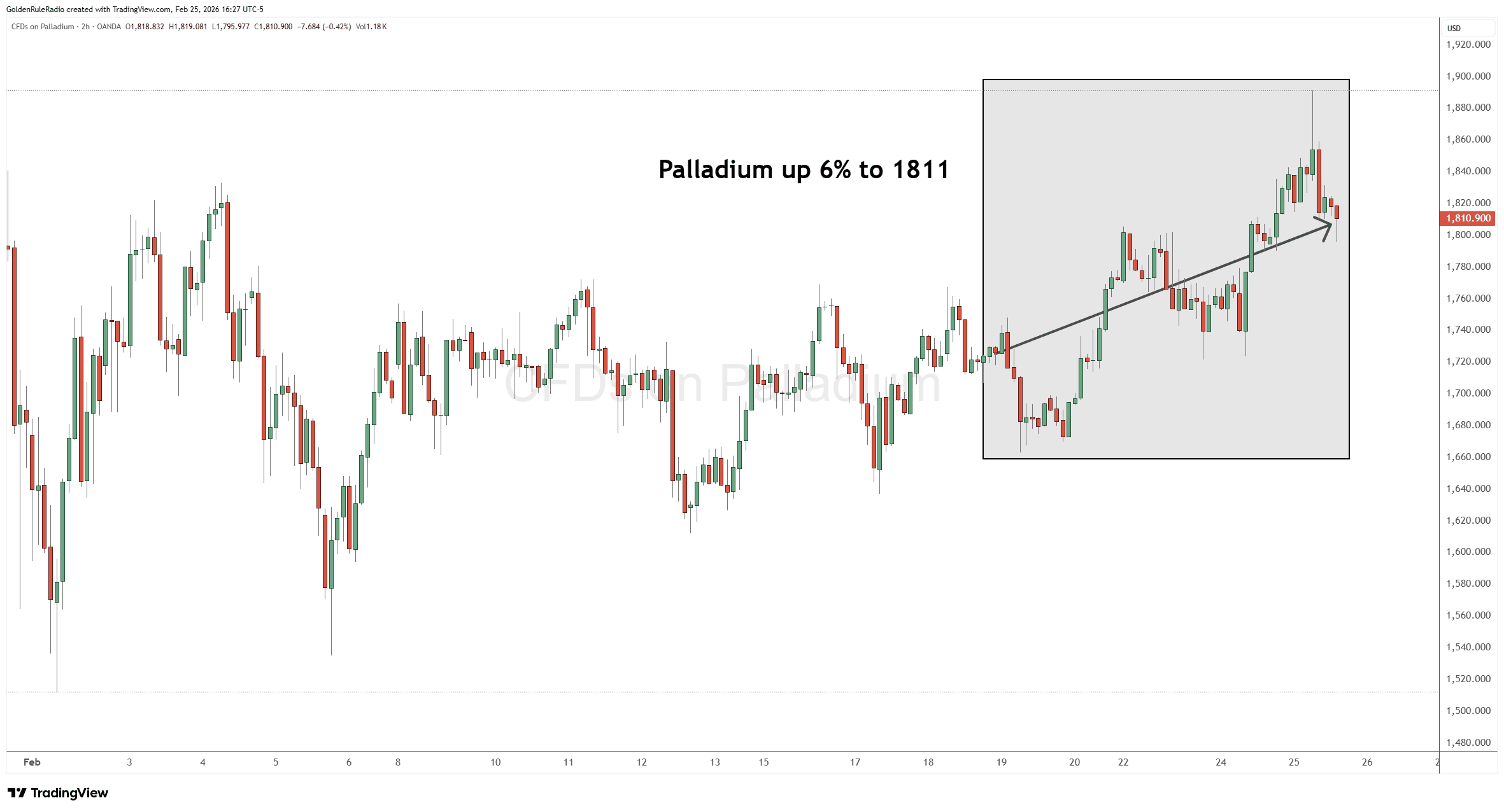

Kevin: Welcome to the McAlvany Weekly Commentary. I'm Kevin Orrick, along with David McAlvany. David, one of my favorite poets is Samuel Taylor Coleridge, I think he's the one who came up with the phrase, "Suspend disbelief." Now, last week you were away, and I'm hoping that you were able to suspend some disbelief.David: Well, you have to at Disney World.Kevin: Yeah.David: It is the happiest place on earth. It may be the most bizarre place on earth as well.Kevin: Yeah, yeah. Well, I would think the Middle East is sort of bizarre right now. So, you had an awful lot of chaos going on worldwide at the same time that you were— What's your favorite ride at Disney World?David: Definitely Guardians of the Galaxy, and Trump did not make an appearance. They didn't play his theme songs. In fact, we didn't even get Tears for Fears, not even one time.Kevin: Really?David: No, no. We were gypped.Kevin: Well, while you were gone, gold and silver tumbled. Okay? Interest rates on, well, not so much the sovereign debt, but interest rates on other debt have been rising fairly quickly. And so, yeah, welcome back, David.David: Yeah. Well, I mean, interest rates were on the rise with sovereign debt, and it was notable, but not to a point which is critical. So, US 10-year Treasury yields, 4.37%. This week, UK 10-year gilts, 4.89. And German 10-year, up to 2.99. There has been a directional shift higher, but little in the sovereign debt markets that signals a massive shift in inflation expectations.Sovereign debt is the core of the core of the fixed income markets. There is developing drama there, but far more if you look at the periphery of credit quality. So leveraged loans, private credit, CLOs, they are now a daily feature on Bloomberg. And as I look at the Financial Times, New York Times, Wall Street Journal, you're going to find a different company featured almost daily. Credit sponsors, limiting redemptions, and it looks more and more like contagion in the private markets has set in.Kevin: Well, you had talked about Blue Owl, and that was— You said every once in a while we would have something three or four weeks ago. Now what you're saying is, every day that's showing up. So in a way, it's really hard to find a safe haven, right?David: Yep, Blue Owl was the first, there's now at least 10 funds that have followed suit, limiting or suspending redemptions as requests have exceeded the quarterly caps. And so, that'll make for a very interesting second quarter as people get in line for liquidity. So, safe havens, you're right, they're hard to find at the moment. Sovereign paper is a classic safe haven. It has sold off, and to see interest rates on the rise would suggest that there's more concern about inflation than there is a drive into sovereign paper as a safe haven.Kevin: And that's probably energy related, right?David: Yeah. I think they're reconsidering the impact— Investors are reconsidering the impact of record debt levels and rising rates. Obviously, an energy shock is gradually being priced in as a fledgling inflationary concern.Kevin: Well, correct me if I'm wrong too, we passed 39 trillion this week, didn't we?David: Yeah.Kevin: While you were in Disney World?David: Wednesday. Yeah, it's a small world and a large number. 39 trillion, that threshold. Bessent has his work cut out for him at the Treasury. And of course, precious metals were not so precious last week. Significant technical pressure and a cascade of stop-loss orders, all the way down to the 200-day moving average. At least in the European markets prior to the Monday open, we saw that steep decline. And then a quick rebound of several hundred dollars off the lows.Kevin: It was like a $400 drop overnight and then the bounce, right?David: Correct, and same with silver. $10 higher for silver off the overnight lows. We give the benefit of the doubt to the secular trend in metals, mindful of a necessary, even if seemingly brutal, short term price correction. Lower prices earlier in the year are a great setup for a third, fourth quarter reassertion of the primary trend.Kevin: Well, and I think it's good to remember, we've talked often in the Commentary, Dave, that countertrends, whether you're in a rising long-term market and you see the downturn, or if it's vice versa, the countertrend is usually the violent one. And what I was sharing with you last night when we were together was just, it's encouraging to see the violence of this drop because it just shows how strong the secular bull is in the long run.David: Yeah. I think the countertrend moves, they're always particularly dramatic. In this case, the primary trend is up and the countertrend decline has found support at the major moving averages. And 4,100 is a very relevant number for gold. Retesting that level in the US markets would be healthy. Yes, temporarily uncomfortable. The line of purchasers was getting longer and longer, in the 5,000 to $5,400 range, and now the line is non-existent.Kevin: Well, and the enthusiasm for gold, you watch that, and the enthusiasm for gold when that was happening was 100%. Now it's dropped to what, three?David: Yeah, the bullish percentage, if you're looking at the bullish percentage measured for gold shares in particular, was pegged at 100, where you had wild enthusiasm. And Friday of last week, it hit 3.6%. Only lower, I think you have to go back to December 2015 for a measure which got to zero.Kevin: Wow.David: Got to zero.Kevin: And that would have been a good time to buy. Yeah.David: Well, when you get sentiment that knocked around, it is an indication of putting in lows. And so, it doesn't mean we're at the lows, but it means we're very near them if we're not at the lows already. So I mean, time will tell, but this is typical herding behavior, and I would act in the opposite spirit to the market. You buy lower and when you're at higher levels, you trim back your positions, versus the recent instincts to buy higher and then sell lower.Although in fairness, I think buyers of physical metals tend to love the lower prices, you get to add ounces at a better cost basis. It's really where you see the pressure most is in leveraged ETFs, in the futures market, with options traders. That's where you see more of the liquidation mode.Kevin: Well, and we saw that, Dave. For the person who owned gold in 2008 when we had the stock market crash and the global financial crisis, the people who had gold, they needed liquidity. So, gold is one of the most liquid assets in the world. That's what happens.David: Yeah, and always worth recalling that gold as a safe haven, if you're in the context of deleveraging, it has in the past looked and behaved like a risk asset for a period of time. And the current selloff suggests to me that the pressure in private credit and in a variety of leveraged trades is more intense than the business news media has suggested. So you go back to 2008, that is a good example of gold selling off as the mortgage backed securities and asset backed securities market was coming unglued, only to reassert its primary trend within 30 to 60 days.Kevin: Yeah, it was very quick.David: Yeah, so finished with a positive number for the year in 2008. I think gold was up five or six percent by the year end, even though it had a 30% drawdown in that correction. And then went on, it was followed by more than a doubling in price off of those corrective lows. So, the late 2008 correction was short, it was sharp as a countertrend correction typically is. And when this correction is over, we'll have set the stage for $6,000 gold, $8,000 gold, ultimately over $10,000 gold.Kevin: Well, and you had mentioned the need for liquidity. We're seeing that in the credit markets, but also Morgan this morning brought up the fact that probably Middle Eastern selling with the Straight of Hormuz being bungled up right now, they're needing to raise liquidity as well, and a lot of their liquidity is in gold.David: Yeah, and a part of that is just, how do we pay the bills? You've got Qatar, Kuwait, Iraq, all looking at a decline in GDP of between 11 and 14%, which is on par with what it was at its worst during the pandemic. And so, you get a couple of countries that are going to take a major hit and will have to fund operations, governmental operations, with something. So having gold reserves, it's a classic rainy day fund. And so yes, they are in some essence, in some sense, raiding the piggy bank.Kevin: Well, but here in America, a lot of times there's a preference for dollars and that preference is based on the need for liquidity, like what you're talking about.David: Yeah, and I think that that preference for dollars over gold, it is a liquidity preference as solvency comes into focus as a concern. Counterparty risk will drive safe haven buying back into gold, and it'll behave less like a risk asset and more like a ballast or a reserve asset.Kevin: So you're basically saying stay patient, because this is temporary?David: Yeah, I would be patient. I'd stay the course. The primary trend is very clear. I would add on weakness, this is temporary. It's also worth noting that the Bank of International Settlements, the central bank to the central bankers, had commentary out in the last couple of days on the role of leveraged ETFs in exaggerating the price volatility of the precious metals.Kevin: Right.David: And I think that's fair on both sides. I mean, how do you get a 50% move in the price of silver in less than 30 days, and then a remarkable decline on the other side of it?Kevin: Margin calls.David: Yeah. Forced liquidations or, if it's just looking at losses accumulating at twice the usual pace, you exit those positions and add even further downside pressure.Kevin: And wasn't it leverage that also pushed the price up so quickly? I mean, at that end when you started to see the spike?David: Exactly. I think it's exaggerated on the upside by that same leverage. And now we get to see the dark side of a leveraged move. And it's worth noting where we're at in the precious metal secular cycle. Thus far, we've seen some opportunism in purchases. You see price appreciation, you see outperformance of gold and silver versus the S&P or the NASDAQ, and you want some of that. So you're lining up for gains, and typically a bull market reaches its crescendo when you have fear and panic buying. And this is anything but fear and panic buying. The late 25 and early 26 scenario was fear of missing out. Wait, it's a winning trade and I'd like some of that.Piling on, and piling on with leverage, the fact that there was a lot of activity in the leveraged ETFs, futures market and options markets, again, suggests that it's a different quality of buyer. And the motivation, the reason, is really not macro in nature. I think you certainly have some macro hedge funds that look at gold as a core holding and look at mining shares as an extension of that, a leveraged play on a longer term bet on the metal itself.But your smaller retail speculator is looking and says, "Well, if silver's up 10%, I'd rather be up 20. If silver's up 40, I'd rather be up 80." And so they're playing for gains. It's a different motivation than asset preservation. It's a different motivation than having something that at the end of the day has simply been money for 5,000 years and is a better expression of a currency allocation not managed by the current PhD standard.Kevin: Right, right. You don't want to play precious metals necessarily for the gain, even though it brings the gain. But with what you're talking about in the credit markets right now, there is an increased need for liquidity. And so the pressure, why don't we talk about pressure on what everyone has, which is a mortgage. And we're not seeing the lower rates that we were hoping for.David: Well, and when we begin to see liquidity drained from the system, it is first at the periphery. So we mentioned leveraged loans and collateralized loan obligations, private credit being under acute pressure last week, but you also saw increased pressure last week in the mortgage market, mortgage backed securities, the prices went higher, agency paper, the cost went higher. And we also saw acute pressure in corporate credit as well, both investment grade and high yield paper. You're beginning to see some real attention paid to credit quality and of course the spreads begin to rise above the Treasury rate.Kevin: Well, and Morgan said what we're seeing are classic signs of a liquidity squeeze right now, and corporate credit, that's going to fall into that as well. Companies are going to be affected.David: And as corporate credit shows stress, as we've long argued, corporate credit pressure increases pressure on the equity markets. So first in most— If you want to see where a real nasty decline in equities comes from, it's when the cost of capital is on the increase for your corporate borrower and that—Kevin: So that's affecting the equities price right now as well.David: Yeah, I think that's probably on a lag. So yes, we saw some volatility last week, but I think what happens in credit ultimately plays out in equity, and we are seeing some shifts in the credit market. So whatever we saw last week in the equity market pales in comparison with what we're likely to see going forward should that pressure in credit remain.Kevin: Well, and that's leveraged as well. I mean, equities are leveraged just like the credit has been.David: Yeah. And so to the degree that interest rates migrate higher, your leveraged traders will be forced into a very awkward position. And again, the biggest leverage out there is in the hedge fund community, whether it's risk parity or basis trades or carry trades, they were getting stomped on last week. And so, again, these are certainly, they play both equity and debt, but they were catching it on both sides last week, risk parity in particular. So, interesting, we see credit default swaps moving up meaningfully on investor concerns of solvency. That was a shift last week, and also, particularly in the emerging markets, you saw credit default swaps on the increase.Kevin: Which is basically insurance on volatility, right?David: It's insurance on default. And so as the cost of insurance goes up, you've got more people clamoring for coverage. It'd be like, you've got a minimal policy, fire policy on your house, but then all of a sudden you've got a forest fire and it's raging and you're thinking to yourself, maybe I should top that off. Well, try to get it.Kevin: To do that. while it's going. Yeah.David: And it may be on offer, but it's going to be at a much higher price.Kevin: That's a good analogy.David: Yeah. It's also in the emerging markets that you see evidence of an unwind in carry trade speculation. So when CDS rates are going higher in the emerging markets, it's a pretty good indication that the carry trade, very leveraged speculation, is coming unwound. So Friday, credit default swap pricing was higher by 52 basis points in the emerging markets, a major move, and it went to the highest set in April of last year amid the tariff turmoil.Kevin: Well, I'm wondering, too, with the emerging markets, the emerging markets might— Do you think there's an effect of the higher energy prices because we're not as affected as, say, Asia would be, right?David: Yeah. And I think that's an important point, is much higher vulnerability to a rise in energy costs in Asia and in Europe. I mean, there's a number of popular emerging market investor destinations where carry trades have attracted a lot of capital, but if you just focus on Europe and Asia, if we're paying $3 per million British thermal units.Kevin: BTUs.David: BTUs.Kevin: Okay.David: It's about a 7% higher cost than before the conflict started.Kevin: So that's not that noticeable here.David: No, but Europe is higher by 140%.Kevin: Oh my.David: So from 11 to now $27 per million BTUs. And in Asia, the JKM market has moved from 14 to— I mean, it's quite volatile, but a range of 19 to 24. So it's up anywhere from 35 to 70%.Kevin: So is there a recession in the wind with the countries that are paying so much more right now?David: Yeah. I mean, think about your manufacturing base in Europe and in Asia. Energy costs are a significant input, and it stands to reason that a 35 to 70% increase is going to impact your profitability. A 140% increase in Europe is definitely going to impact your profitability.Kevin: And the price, and the price you pay for those goods.David: Yeah. So recession risk is much higher in Asia and in Europe. And these are places that are far more dependent on energy imports. So continuation of the conflict in Iran will see much more dramatic impact there. And if global recession dynamics set in, you'll see an impact first in Europe and then, on a lag, I think into US equities.Although we don't face the same risks in terms of import vulnerability, there still is an impact if you're thinking about US equities. The S&P 500, that comes to mind, two fifths of profits come from overseas. So if demand is squeezed overseas because of recessionary tendencies or trends overseas, then it will show up. Won't show up in something like the Russell 2000, small caps, which are really focused on a domestic market. But if you've got multinationals in the mix, that's where your two fifths of profits are coming from overseas and you've got to be much more mindful of recessionary trends outside the United States.Kevin: Well, and you had brought up, we don't really have to worry about a supply problem. That's very different than the 1970s, when we had the oil crisis in the 1970s. At this point, we export oil, right? We're not importing oil nearly as much as exporting.David: Yeah. And last year, we benefited from that to the tune of, I think, 64, $65 billion, if you're looking at sort of our energy trade balance. We're a net energy exporter. We don't have supply problems. We may end up with a consumer price problem. Swallowing higher prices at the pump is economically challenging for a lot of households, and it's very politically consequential.And so keeping in mind the midterms, this is something that could be a defining factor for the midterms. But in this respect, things could not be more different than the 1970s. We had total dependency on Mideast oil. It's a non-issue in the US today. It's very much an issue in Taiwan, very much an issue in Japan, very much an issue in South Korea.Kevin: When we're talking about Asia and Europe right now, I mean, this is probably an area that we haven't really paid enough attention to.David: Conflict in the Middle East tightens global energy supplies. It pushes oil and gas prices higher. Increases inflation as a net effect. I'll repeat, it's Asia and it's Europe that are the most vulnerable to recession. And frankly, from a strategic standpoint, there's glaring vulnerabilities in places like Taiwan, down to 11 days of oil reserves.Kevin: Wow.David: That is very interesting because you recall that what we've done, what the US has done, the Trump administration has done to blockade Cuba from fuel supplies. We had a complete power outage just a few days ago in Cuba, with no fuel available, zero. China can easily do the same to Taiwan, an energy blockade. And you're talking about such low reserves at this point, what happens to the global economy if Taiwan comes to a halt? I think it was McKinsey a year ago suggested that you're talking about a trillion-dollar hit to global GDP if you take Taiwan offline.Kevin: And you said they have 11 days, right now, of reserves.David: Correct. Correct. So in this regard, I think Trump has set an unhealthy precedent in terms of a blockade and sort of an energy— I mean, at this point, if the Chinese wanted to do the same, they basically say, same playbook, "You did it, what's wrong with us doing it?"Kevin: Right, right. Well, it sounds like it's coming to a head at this point. I mean, because we also have the midterm elections, and inflation is still on the minds of the people.David: Yeah. I think Friday of last week was sufficiently terrifying in the global financial markets for Trump to suggest an end to the Iranian engagement.Kevin: So you think it was just the turmoil that we had with a split force that-David: Oh, yeah. He pays attention— Just like he's claimed 50,000 on the Dow, look at our great success. To the degree that you see slippage in the financial markets or chaos in the financial markets, he's hypersensitive, hypersensitive to it. So I don't know what very soon means. I don't know what mission accomplished means. I don't know what he means by our objectives have been met.Kevin: They're still shooting missiles and drones.David: Yeah, and I'm shocked and amazed that after, I don't know how many hundreds of sorties and thousands of targets hit, seven to ten thousand targets hit. I don't know how there's anything left.Kevin: Where are they coming from?David: But they are.Kevin: Right.David: And the Strait of Hormuz is still under threat, and there's still the capability of launching hypersonic missiles and throwing into the air any number of drones.So we also had last week, we had PPI, Producer Price Index, it could have also been a strong warning to the Administration leading into the midterms. What was expected was a three-tenths percent increase. Instead, we got a 0.5 and that was on core. So if you're taking out food and fuel, there's your half percent increase, and factor in food and fuel, factor in fuel to the PPI, and it's 0.7% increase as opposed to the 0.3 expected.Kevin: And people really watch the gas price. I mean, they may not watch inflation, but they see what they're paying at the pump.David: Which suggests that with PPI surprising to the upside, CPI will probably, Consumer Price Index will probably surprise to the upside as well. And if we get past that $4.11 threshold—Kevin: What is that? Why 4.11?David: It's the point that we hit back in 2008 with the last run in oil to 150. And it was the point at which the consumers were coming unglued. You could have put anything in front of them and it was pitchforks and people ready to tar and feather anybody in the oil business because it seemed like this was being done to us. Again, it's politically consequential, and $4.11, if you breach that national average on gasoline prices, I think consumers will revolt in the midterms.Kevin: Well, and the Trump administration has to know that midterms typically go to the other party. And so they're already, they're vying for good perceptions. But when we were talking at the meeting today, three scenarios were put forward. One scenario was a quick, decisive, complete victory for the United States. The second one would be a longer prolonged issue, and that could actually lead to many long-term problems. That's the duration problem. And then the third would be some sort of negotiated settlement, which would probably have to include Russia and China because they're so closely tied. And so the three scenarios, the middle one, the duration one you talked about, you said duration is probably going to be key as to the aspects of the effect of this war.David: Weeks ago, that duration issue, that was the critical variable for us thinking about the Iran conflict. It remains the case. If you look at energy shocks and extended war, these are factors that increase the odds of recession dramatically. You could see consumer behavior become self-reinforcing here as well. Even if you've got a recessionary impact overseas and not in the United States, if prices at the pumps stay high enough long enough, back to the duration issue, you begin to see a shift in consumer dynamics and what are they spending on.Kevin: Slowing the GDP.David: Yeah. Correct. Correct. So you've got consumer expectations, which feed into inflation. You also have on the horizon expectations already shifting in terms of the duration of the conflict. The oil curve is shifting along with the yield curve, both higher levels and longer time frames being reflected on those curves.Kevin: That's interesting that you can look at that, but that's true. When you look at the future's markets, you can see what expectations are. And at this point, longer term oil. And that's a reversal from when the war first started, if I remember right.David: Well, so far the curve hasn't gone the other direction. It still falls off pretty dramatically, but the whole curve has shifted higher, and as it shifted higher, it's also extended further out. So the expectation is growing that it's going to be here longer than we originally thought. I mean, again, two weeks ago you could have looked at the curve— The difference between two weeks ago and today, the curve is bumped and extended further at a higher level. So again, when you start thinking about the long-term inflationary consequences of this engagement, will it be here long enough to change consumer behavior in the US? It's already at a level which is beyond critical in Asia and Europe.Kevin: So if consumption does slow down, okay, we are in a midterm election year, if consumption slows down, a classic Keynesian would say, "Well, the government just needs to print some money and spend it." Do you think that might be the response if that happens?David: Yeah, it's a fancy economic term, aggregate demand. To prop up aggregate demand—which is the sum total of demand within the economy, consumption in the economy—if that begins to fade, the consumer tightens his belt, classic Keynesian demand management kicks in, and government spending is supposed to fill the consumer gap so GDP contraction stays at a minimum—except that in this environment you've got deficit spending pre-conflict already on track, according to the Congressional Budget Office, to be $1.9 trillion. That's the projected deficit for 2026.Kevin: And we're not including war spending right now either, are we?David: Not included, not included. So how large a consumer gap would Donald Trump and Scott Bessent be willing to fill? If equities soften over the next six to nine months, you've got not only a diminishment in capital gains tax revenue, you've got that reverse wealth effect which would hit consumption pretty dramatically. Again, it's just a question of, let's say we spend an extra two, three hundred billion dollars in war spending, so 1.9, you're already at 2.2.Kevin: 2.1 or 2.David: And then again, if the consumer's retrenching, the government typically steps in. How much more are they willing to add, and what's the threshold level at which the bond market begins to reappraise the stability of US fiscal position? And I don't know what that threshold is, but that's where I think you begin to see significant issues within the fixed income markets.And it really is— We're in this phase where people are focused on, investors are focused on, liquidity, and there is a preference for dollars. It doesn't take much of a shift to start reconsidering solvency. That can be credit quality. It can also be duration risk. It can also be just sort of fiscal viability, which pressures rates higher. And these are all game changing elements.Kevin: So a stronger dollar today could mean a much weaker dollar tomorrow. I mean, there's no telling what could happen if that scenario plays out.David: Yeah. I mean, when I recall, when I bring to mind these backdrop issues, you could reverse the first quarter dollar rally with a swift decline by year end. I mean, not a gradual decline, but—Kevin: But a reversal.David: A reversal. A sharp reversal. And at the same time witness a ratcheting higher in rates reflective of Treasury oversupply. And we already talked about, a few weeks ago, the trillions of dollars that have to be refinanced this year, existing debt which is coming due. You've got to satisfy investors with an adequate compensation. Interest rates have to reflect their demands for compensation for risk. And you start adding, is it 1.9? Is it 2.2? Is it 2.5? What's the final tally for deficit spending in 2026?The war hangs a question mark over that, which is very material for the fixed income markets. And I think you have the Fed and the Treasury put in a very awkward position. They can either watch the financial markets circle the drain or they can instead intervene. And how they intervene, to what degree they intervene, when they intervene, these are all relevant factors in order to keep the Trump Dow 50,000 narrative alive through the midterms.Kevin: That costs some money. That costs some money.Well, okay, so let's talk about liquidity because that really is what's affecting things right now. I mean, even I had to sell some gold and silver, we're putting windows in on the house. And I mean, that's what it was for. So I needed to raise liquidity, but I didn't tap into the portion that I'm using for preservation. In other words, the difference between raising money for liquidity temporarily or holding long-term for preservation, you're still encouraging that you add to that position.David: Yeah. I mean, I think, again, looking at the macro backdrop, this is one of the best setups that gold has ever had, ever had, in US financial market history.There is a place for liquidity, and certainly we keep adequate liquidity in the asset management side of our business. We're close to 40% liquidity today. I mean, it's not like we don't prize short-term Treasuries or a cash equivalent position, but there's also a place for conviction on the gold trade. And while I can't argue with price action—I mean, the last week was ugly—I can see beyond the temporary price pressure to the enduring issues of our overindebtedness and of a significant monetary regime change. The Mideast conflict is in many respects helping to facilitate and codify a shift away from dollars.Kevin: Yeah. So the dollar recycling is still being replaced by gold recycling through other currencies.David: And I'm not talking about the immediate-tense investor liquidity preference, which boosts demand for dollars. I'm talking about global trade, and this is where global trade settlement is a far bigger issue. You're changing the international financial plumbing as opposed to watching today's preference for US dollars.Kevin: Well, and even Iran is saying that they'll only let ships through that are trading oil in other currencies, like Chinese yuan.David: Yeah. I mean, the Chinese are settling oil in yuan, and the very large crude carriers getting through the Strait of Hormuz are either connected directly to Iran—China, India's had a number of ships that have gone through—Kevin: But these are all BRIC type of countries that are moving away from the dollar already.David: Yeah. Largely anti-dollar-block countries that are seeing their VLCCs [very large crude carriers] get through the trade of Hormuz untouched, unscathed. Normal traffic's 138 vessels per day. That's what it was pre-conflict. Now it's down to five to six per day. And again, those with safe passage are tied to that largely anti-dollar block.So it is interesting that we see this codification away from dollars. I don't have evidence that every one of those barrels that's making it through Hormuz is being settled in yuan. I just can't imagine that China would be interested in doing so, or that Iran would be interested in trading their oil in US dollars.Kevin: Well, and it may not be yuan. It might be rubles. It might be rupee. I mean, these are countries that will trade their currencies for oil and then those oil countries will trade for gold.David: Yeah. I think post-conflict we are not going back to the old petrodollar recycling. And at the margins, you see the changes. Russian barrels will trade more and more in rubles. Payments from China for the purchase of whether it's Iranian oil or Russian oil will be in yuan or RMB. Indian purchases will be going forward in rupees. And so, at the margins we are codifying this demise of dollar hegemony.Kevin: Well, and Morgan has brought this up, too. You guys actually brought this up at the last McAlvany Wealth meeting that we had in October, that possibly Scott Bessent and the Trump administration need to see the dollar lose that hegemony to some degree because of the burden of being a reserve currency at this point.David: And the priority of reshoring jobs and building out our manufacturing base, it does imply a degraded dollar. I don't think they want an uncontrolled decline, but if they saw a gradual decline, that would certainly be compatible with their larger policy objectives.Kevin: So they might not be opposed to this disconnect that's going on, fully.David: Yeah. The question is how big of a decline it is, and that's the difference between the dollar being on— At the end of this conflict in the Middle East, are we on the injury list or are we sort of in the casualty catalog?Kevin: Right.David: So I could imagine the current liquidity preference for US dollars getting purged as the annual deficit comes in north of 2025. So again, currently we have dollar strength. That can flip pretty fast with a reappraisal of US Treasuries and the value of the US dollar. At what price stability?, is the question. What are the trade-offs that the current administration, between Bessent and Trump, is willing to accept in order to maintain financial market stability into the midterms, to keep a lid on rates and to prevent interest costs from skinning the Treasury alive? Is yield curve control something that we can assume is slotted for the back half of 2026? Is it out of the question? I think it's becoming more and more probable by the day. And where do you think gold goes in the context of desperate debt monetization?Kevin: Sure.David: This is again where I say my bullishness on gold is not biased or based on owning it and wanting to see it higher. I simply can't imagine a world where policymakers navigate these challenges without significant reputational costs. And it's loss of confidence tied to that reputational cost— It's loss of confidence that I see reflected in the gold bull market. Price appreciation is proportional and directionally opposite to confidence. So, declining confidence, and that's where gold begins to step up the pace.Kevin: Right.David: So the world is—at least from the perch that I sit in—the world is looking far less stable today than it was six weeks ago or six months ago or six years ago. And in the final analysis, gold is the preferred safe haven when solvency is on the line.* * *

You've been listening to the McAlvany Weekly Commentary. I'm Kevin Orrick along with David McAlvany. You can find us at mcalvany.com and you can call us at 800-525-9556.This has been the McAlvany Weekly Commentary. The views expressed should not be considered to be a solicitation or a recommendation for your investment portfolio. You should consult a professional financial advisor to assess your suitability for risk and investment. Join us again next week for a new edition of the McAlvany Weekly Commentary.* * *

Kevin: Welcome to the McAlvany Weekly Commentary. I'm Kevin Orrick along with David McAlvany.Dave, you had an unusual conversation with Lauryn Williams, an athlete who has won medals both in the Winter and the Summer Olympics.David: Yeah. Amazing to see someone who's competed four different places around the world, Sochi, Athens, London, and in China as well. A 100-meter racer is someone who's got some real talent. I mean, it's down to fractions of fractions of seconds to be the fastest person in the world. And so to medal and to be in the top two, three in the world in that event is meaningful. Then to translate all that power into what she can do in a bobsled is great.As we talked to Lauryn Williams, a four-time Olympian and first women, as you mentioned, to win both the Summer and Winter games, that is certainly a part of her legacy. I was fascinated as we got to the end of the conversation that for her, her greatest accomplishment was nothing to do in the world of sports, but was something that she had just recently discovered. The beauty of motherhood and what it means to lead in a different way, to inspire in a different way.And she's been both an inspiration and a leader on the Olympic team. And she competed not only individually but also in teams, in various relay events, and of course, the bobsled is a two person team as well.And so, I was left with the impression that here's a woman who is a reader, here is a woman who is legacy-minded, both from the standpoint of high levels of competition and wants to win—is there to do one thing: win.So many people in the world of business can win, and it's at the expense of other people. That sometimes is the unfortunate case of zero-sum game. I think, for her, being legacy minded, being a lifetime learner, these are things that were very impressive to me.* * *

Lauryn Williams, great to have you join us today. I don't know that I've had the privilege of speaking with someone who's won as many medals as you have at a level of competition that is second to none. There's athletes all over the world who aspire to someday be in the Olympics. And you've been there not once, not twice—Athens, London, Sochi. The accolades for you as a sports professional just go on and on. Tell us a little bit about yourself, just kind of background for our listeners.Lauryn: So a little bit about me, I'm born in Pennsylvania, raised in Michigan. Split time between both because my parents split up. Then I went on to the University of Miami, and then I moved to Texas for a little bit. When I say a little bit, about 10 years, and now I live in Medellin, Columbia.The things that I think my mom would say are important if she was saying, "This is my daughter, let me tell you about her," is that at age nine-ish, I got home faster than the family German Shepherd. And she was like, "I got to get my daughter into a track and field program."My dad's story, on the other hand, is a little bit different. He says we were at the Carnegie Science Center, and there was a Flo-Jo hologram, and I didn't see anything else at the Science Center that day, I only raced the hologram until I beat it. I don't think it was set at World Record pace back then, but that's when he knew I had some promise for track and field.And I was really fortunate that my parents instilled in me the importance of education. And so I wasn't really thinking about track as a thing that I was going to do long-term, or the Olympics. I didn't really understand what it meant to be in the Olympics. I just liked running faster than the boys in my neighborhood. I was like, "Okay, I can beat the girls. Now I can beat the boys." Then I started to beat boys older than me, and I just thought it was a really cool thing to be able to brag about.I wanted to be able to use my education in order to be able to help people, because my godmother and my godfather were a neonatologist and an anesthesiologist, and I saw their big house. I saw the fun parties that they had. And I just thought, "Education is the key to get me the money so I can do whatever I want." And at a young age, that was the extent of my thought process.David: Well, would love to hear about your journey to becoming first American woman to medal in both the Summer and Winter Games.Lauryn: Yeah, I think that the journey was just kind of mapped out for me. So in 2004, I was a junior in college. I was just focusing on winning the NCA championships, and I was so excited for that opportunity. I had gone my freshman and sophomore year to the national championships, but I had not won, and my sole focus that year was winning the NCAA championships. No thought of the Olympics had crossed my mind.I get to the NCAA championships, I run the second-fastest time in the world. I do win. And now I'm the fastest American heading into the Olympic Trials. And I was just like, "Oh my goodness, what do I do?" Luckily, I had a coach that helped me just kind of navigate the world of becoming a professional athlete. I made it to my first Olympic Games in 2004 at 20 years old, and then on went the journey. 2008 in China, 2012 in London.And the cool part, I think, of the story is, everybody says like, "How did you become a bobsledder? What was that path like?"I met a girl in the airport. Reading is fundamental. I love to read. I read an article about a fellow Olympian who had tried bobsled and enjoyed it, and she and I were in the airport headed to a race. So she came back to track and field. We were both just randomly heading over to Rome and met in the same airport, and I asked her about it. "How was it? What was your experience like? How did you find bobsled?"And she's like, "Lauryn, you got to try it." And it's the Olympic year. And I was like, "The Olympic year? How do you become Olympian in bobsled?" That was not a thought process of mine at all. But I did go ahead and give it a try because I knew I was getting ready to retire from track and field. And so, little did I know, six months later I would be at the Olympic Games.David: It combines both team dynamics because you've done track and field relay, as well as competing on your own, and bobsled, again, it's a team dynamic. How would you compare, how would you contrast the difference between being an individual competitor, this is your event, it's all on you, versus the working collaboratively with someone else or with a team.Lauryn: Yeah, I think my path was divinely made for me to be prepared to win that medal in bobsled. And I mean that in a way that in 2004, 2008, I was a part of the four-by-one Olympic relay team, and we didn't have any success.And a lot of things happened behind the scenes, but what I realized is what we need to be able to do to work together, especially when you have different chemistries. We're taught to compete against each other all year long, so these are the same girls that you are racing to beat, racing for a spot on the Olympic team. And then they throw you all together and say, "Go win Olympic gold medal for Team USA." And we botched it, like I said, not just once but twice.What I realized is what was going wrong in those two Olympic Games, so that when I was brought to the third Olympic Games, I said, "Hey guys, I know how to make this work. The one thing I can bring is my experience," because a lot of the other members were new members of the Olympic team for the first time.And so I said, "We got to cut the fighting out. We've got to be able to get on the same page. We've got to have chemistry." And I think that was also the catalyst for me having what I needed to be able to switch over into bobsled, which is much more of a team sport, much more cohesive. But learning how to unify people was a skillset I had to learn from the trials and tribulations we had in 2004, 2008.David: Yeah, that's amazing. I'm curious about the psychology of competitive athletes and what you look back on in the various competitions you've had all over the world, what's the most valuable advice you've been given to manage your own psychology? Some days you show up and it's a great day, some days you don't. And to be able to manage the ups and downs of a highly competitive environment, do you feel like you got what you needed in terms of psychological coaching? And what would be something that you would add to the mix?Lauryn: I feel like the thing that I got or that I learned from the situation was: control what you can control. There are so many things outside of your control, and we've got to pivot in those moments and make the most of them, but the main focus should be on what you can control. And I remember very clearly in the 2004 Olympic Games, one of my competitors making just like these crazy grunting noises and screaming and yelling. It was meant to be a distractor to us. And it was very distracting because it was just like, "What is she doing? Is she having a seizure? Does she have a medical issue?" It was just not normal sounds that would come up. And I had to say, "Hold on a second, Lauryn. Why are you here?" I am here to get to the finish line first. That is the sole purpose that I have for being here right now in this moment. Does not matter what noise, what is happening around me.And in the same way that you can drown out the crowd and drown out the things around you, I needed to control what I can control. Her noise-making I could not. But getting to that finish line, hearing the gun and zoning in on the starter was something that was within my control. And when I started to think of things about, what can I control versus obsessing about the things that I couldn't control that maybe were bothering me, I started to have a lot more success.David: Great point. Can you tell us about your mission to help elite athletes have a better handle on their finances?Lauryn: Yeah. I started in track and field, like I said, at age 20 as a professional, and I didn't know that that was going to be my future or my fate, if you will. I had very little financial literacy at that point. I was a junior in college. I was a finance major. And now looking back, I think so many of us look at what we learned in college and the information you could throw out the window versus information that is absolutely necessary. And personal finance is different from the broad major of finance. And then I just didn't have a lot of life experience.So I ended up in the hands of a family friend as a financial advisor. And I didn't know that there were different types of advisors. I didn't know what kind of questions to ask a financial advisor, but I did know that I had an opportunity to make more than anybody in my immediate family had made, and I didn't want to waste it.And so I was like, "Hey, what do I need to do?" And I didn't get good answers from that advisor. So I fired him, hired another guy, thought that was going to go better. It didn't. And then I got frustrated. I said, "What does somebody do when they're willing to pay for help to organize their finances, but they can't find someone?"And so I went online and I found the certified financial planning coursework, and honestly, I rolled in it just trying to teach myself stuff about money because I didn't understand the basics of creating a financial plan for myself or the basics of personal finance.The coursework itself put a light bulb on, if you will. And as I learned these things, I was asking my friends, "Well, do you have a SEP IRA? Are you using a solo 401(k)?" And they're like, "What are you talking about, Lauryn?"And that's when I realized it wasn't just me that had this gap as a professional athlete who was earning well. It was a bunch of us that were being neglected, and had a good earning potential and a good opportunity to make the most of a very short window of earning well, but we weren't doing it. And so I wanted to be the change I wanted to see in that regard.David: At Vaulted, we share your mission to support America's top athletes. So as you know, we've started this initiative giving $30,000 of real gold for each first place finish, and we're very excited about that. I think, in part we see that there's a challenge for many professional athletes. I'd love for you to share with us what the biggest misconception the public has about an elite athlete's financial reality.Lauryn: I think the biggest misconception is that when you win, you're set for life. In the United States, you are not set for life by simply winning an Olympic gold medal. In the same way that we have 1% of America that is the affluent, we have 1% of those that are making the Olympic team that are earning in a situation where they could be set for life based on the earnings and the endorsements and things that come in.There are a lot of athletes that do not earn anything the following year after competing in sport, or earn very little, or they only earn what is given by Team USA for the Olympic medal. There is a program, Operation Gold, now where there is some money given to you, some cash given to you for your competition and your role. But after you spent years of training, even if you just go with the year before the Olympic Games—the amount that you invest into having coaching and housing and proper food, physiotherapy, nutrition—the $30,000 that they give you is pretty much used up.To compete on a world stage level, that's not millions and trillions of dollars. It's not something that's going to make a long-term impact on your life. It's going to probably clear the debt or replenish whatever you saved in order for you to be able to move on. And like I said, the hundreds of thousands or millions that a lot of people think that we make is few and far between.David: Yeah. So if there's a small percentage of people who can monetize their professional sporting abilities, we see endorsements as a potential way for— But what percentage of professional athletes actually get those endorsements, what would your guess be?Lauryn: Oh, I would say it's a very small percent. Like I said, I made the team in 2004 and there were no outside endorsements. My only sponsor was Nike, which was the shoe company, and which in track and field specifically, that's the main way you're considered a pro athlete is that a shoe company gives you some sort of contract. So there's not like the NFL or NBA where you're like a W-2 employee of a team of some sort. You're not a W-2 employee of the United States Olympic Committee either. And so, yeah, 2004, there weren't very many endorsements at all. A few things came afterward, but they're usually like one-year contracts or they'll do six- or eight-month contracts that say, "We want to use your name during this Olympic timeframe. We want to use your name for the next year." It's not a long-term, four-year or 10- or 12-year thing. It's just like, "Here's an influx of money so that we can work off of you and work off the hype that is happening around you."But a very small percentage of athletes get those opportunities. I think now the branding opportunity that athletes have that I didn't have necessarily when I was competing, was being able to use social media as a platform to talk to other sponsors and be an ambassador of different sports.David: So if income after the professional event, after the winning of a medal, is something that is less predictable, what's a story that you've heard from an athlete that really illustrates the struggle of what's after standing on the stage and receiving those medals?Lauryn: Oh, there's so many, but one that stands out to me is my very first Olympic Games. In 2004, I was on my way home. We were in the airport. I was with a fellow athlete. We had the same agent, so we had the same flight booked. And he's like, "I'm so excited to only have to work 40 hours per week." He's like, "I'm going down to 40 hours." And I was completely confused because I was a junior in college. So I went from college to the Olympic Games and now I was going to be a full-time professional athlete. And the contract that I had, I did not have to work. And there's a big difference between, like I said, events as well.I was a 100-meter runner. That's kind of a premier event for the Olympic Games. Everybody's tuning in to see who's the fastest man and woman in the world. He was a high jumper, and he had just won the same silver medal that I had won in his event at the Olympic Games, the second-best high jumper in the world. And he was not planning on not working at all. He was planning on going down from an 80-hour work week to a 40-hour work week at that time. That was what the income that he was going to receive was going to help him do.David: Do you find professional athletes end up with debt? What does that look like?Lauryn: Yeah. Unfortunately, it is par for the course that a lot of athletes, like I said, at various events are ending up in debt. And the thing that I've been fortunate to be able to do, I think sometimes people think of what a financial planner does, and we think of wealth management and investing and those pieces of the puzzle, but the thing that was really important to me was being able to help people on a foundational, baseline-level basis.And I helped them figure out how to take out the best amount of debt. "Let's take it from here versus here because this will have a lower interest rate." Let's think about how long you're going to train for before we give it up because you're in too much debt to maybe recuperate if you take on a regular job. What are the cause and effects of you deciding this? How can we take on this debt responsibly, and how can we make a plan to be able to pay it off responsibly if you're going to take on debt?"And I think that's a reality that, like you said, not a lot of people are thinking of or not a lot of financial planners would be interested in. It was like, debt is bad and that's it. This is someone's dream. This is someone's goal that could be once in a lifetime, and if they achieve it, it's something that no one can take away from them. So why not let somebody make a calculated decision and an educated decision to be able to take on that debt, versus just kind of willy-nilly swiping a credit card and going about it and then having to pay the price later?David: It's such an interesting setup because you've got kids who go to college, and very often they'll graduate with $100,000 in debt, $150,000 in debt. If you go on to a master's program or law school or medical school, you could have a half million dollars in debt. What's the kind of range you're talking about? Is it tens of thousands of dollars, six figures, for a professional athlete who's pursued their dream? But very different than a doctor who you could say, "Well, hey, eventually you're going to be able to work this off," the pay scale is sufficient to ultimately pay back a half million dollar liability.Lauryn: Yeah, I would say it's probably around $30,000 on average. That was kind of the threshold for what I was seeing as a regular amount of debt that athletes were having to take on or a normal amount of expenses to be able to cover things, and where people start to just feel uncomfortable. $70,000 or $80,000 of debt, it's a harder hole to dig yourself out of.And like I said, one of the things I was fortunate to be able to do is kind of forecast that, because a lot of people don't think about what happens in the future. They're just thinking about what's happening in the moment. They're betting on themselves, hoping that it will all pay off, that they'll be able to write a check for it at the end of the day because performances have played out.But my job is to be able to say, "Okay, what if it doesn't? What kind of work can we get? What is your degree going to bring you? And how long is it going to take you to dig yourself out of that hole if everything goes wrong?" And so yeah, $10,000 to $30,000 was the average of what I was seeing. The most that I saw was, I think she had $96,000 of debt. And she had come to me with that debt.David: Well, let's talk a little bit about athlete chatter. If you're coming home from the Games, is there ever any conversation among the athletes about top honors not being real gold?Lauryn: Always.David: I mean, are competitors even aware of that?Lauryn: Yes. I remember learning, and I said, "Wait, what? It's only gold plated? Wait, what does that mean? You mean the rest of it has something else inside of it? Well, what does it have in it?" And then I got home and I was like, "It's not even real gold." I was definitely let down when I learned that it wasn't an actual gold medal, especially because I had seen on television people biting the medal and I thought that that was like, "Wow, what a cool thing. You have this big bar." And like I said, I was raised in a time where gold was talked about a little bit more. I think it's talked about a little bit less now as an asset or just like, "Wow, I'm going to get this thing that's really valuable. I'm going to have my own gold bar in the shape of an Olympic medal." That is really what I thought it was. And then I learned, they were like, "The silver medal is actually worth more because—David: Amazing.Lauryn: —it has more silver in it than the gold medal has [gold]." So I was like, "Oh, okay."David: That's one of the reasons why we wanted to start this initiative with Vaulted, because we see the amount of work that goes into being one of the world's greatest athletes. And we just want to honor that, want to recognize the time and talent and all that each individual athlete brings in terms of the honor and prestige to our country. And it seems a little cheap, frankly. That's the way I feel. But I'd be interested in how you feel about that discovery process and what most athletes are like, "Oh, well, it's not even real gold."Lauryn: Yeah. A little cheap is an understatement. There's so much money that goes into the Olympic Games, so much sponsorship, so many different pools of income that come around the Olympic Games. And athletes have long been frustrated for not being compensated for the work that they do, and having to figure out sponsorships.And like I said, even in America, we're not one of those countries where we set the athlete for life. A lot of places, you get land or you get lifetime membership into the military, etc. And so it's just frustrating in general that this is the world's biggest stage to compete on for your sport, and you said that the thank you is something that has very little value at the end of the day. And so yeah, I wouldn't even go so far as to say it's cheap, I think it's kind of disrespectful what they give us as the medal when it's all said and done, because we know how much money is floating around.Other people are being well compensated, executives and various sponsors and stuff are gaining from this. So if nothing else, if we will not be compensated, could you invest in giving us a medal that we could be proud of for a lifetime?David: All right, so as a certified financial planner, as someone who looks at every asset class and says, "Okay, this is how you create a mix," is physical gold something you'd actually advise athletes to hold?Lauryn: Yeah. I've evolved as a planner. I was definitely hard no on the front end. I've just come from a very conservative background. I mentioned a little bit of my story with the financial planner, ended up with two very hardcore commission-based guys that sold me a bunch of products that I didn't necessarily need. And so when I entered financial planning, I was pretty purist on low-cost investments and keeping things very simple, and knowing that investing was going to be a key piece of your puzzle to help your money grow, but not doing things that are super complicated. And so that evolution that has come around is thinking about what really diversity means, and understanding that in terms of what is going to be long-term. Cryptocurrency. I remember at the very beginning with bitcoin coming out, and I was just telling my clients, "No, absolutely not. No way, no how, stay away from it."And I know quite a few people that put everything they had into bitcoin. And while I'm still not a fan of that as a way to go about your investing strategy, if you got in on the very beginning of it in the same way that, like you said, we saw gold way back, once upon a time at a much lower rate than it is now, if you can hold your investments in general for a long term, you do generally get to see the benefit, reap the benefit of having patience and watching that investment grow over time.David: Yeah. In the time that you've been an Olympic competitor and took the podium for the first time, you're talking about a metal that was less than four digits, under $1,000. To now over $5,000. And the reality is it just keeps track with inflation, so it's getting repriced gradually to reflect the loss of our purchasing power. And as such, it's kind of a ballast asset within a portfolio.I'm curious if you think the athletes that accept the gold from our initiative will keep it invested, sell it? What would you advise them to do based on current market conditions, recent trends, things like that?Lauryn: I would definitely say keep. What a cool opportunity this is. What a great thing to be able to add to your portfolio, like you said, diversification happening without you having to be an investment guru. I think this is a really cool long-term opportunity that Vaulted is giving these athletes. But the reality is that, like I said, some will have to pay off their debt, and so turning it into cash and using it for purposes like that will happen.I'd love to hear that every athlete talks to a financial person if they don't have one before, and just say, "Hey, what's the best thing to do? Maybe I could take a third of this and pay off debt. I could take a third of it and put it in a traditional investment account because I've never opened one before, and keep a third of it in gold," or whatever is the best thing for that particular athlete.But I think, like I said, based on where athletes are currently, while the needle is moving in the right direction, it has not moved enough that athletes are not going to want to take their cash and run. But we've got to encourage them. We've got to educate them to understand what a cool opportunity this is to be able to have this gold and to be able to, like you said, maybe 20 more years from now, see what that investment has grown to.David: Well, I worked with gold my whole life, but my relationship with it is, I think, different than yours. When you think about the meaning of gold, both the symbol and as a financial asset, what does it represent to you personally? Do you see a difference between the symbol and the asset? What do you think would drive that?Lauryn: I think, for me, the two are still kind of one and the same. Like I said, with the Olympics being such a big part of my life and that gold medal being the thing that you're chasing, the actual asset—gold—represents achievement to me. It is a longstanding asset that has been around for pretty much forever. And once you've done something in the Olympic scape, there's something that can't be taken away from you. I will always be the first American woman to medal in the Summer and Winter Olympics. Whoever won the gold medal just recently in these games will always be the gold medalist for 2026. I had to think about what year we're in.And so the longevity of what it is that you have accomplished is kind of imprinted in whatever medal it is that you've earned. And like I said, in specifically the gold medal, in the same way that the longevity of gold and its value, like you said, it's undisputable what's happened over the course of time, and that it's been here. It's been a constant part of our lives and it's been a great way to be able to diversify our portfolio. So I feel like they run synonymous along the same lines as far as their meaning and their importance in my life.David: Yeah, I certainly see that with investors. It is a representation of real wealth, and it is a store of value through time. So in a different way, but a complementary way, it does mark their achievement, whether it's in business or in just being diligent in their savings through time. It's something that is a representation of the hard work and effort that they've put in. And that certainly is what that medal is supposed to be for you, a mark of achievement, an accolade, a mark of prestige in our country.And just, thank you for representing us so well. What you did certainly accrues to your own legacy, but it's one of those things that certainly is one of those things that as an American we're so proud of. And every time I watch the Games, it just gives me chills. Every time we see one of our athletes take the stage, it's something that's like, "Yes, I'm proud to be an American."And it's you that stirs those feelings of, "This is greatness and this is what we're capable of." Just the beginning. There's so many more people out in culture who have these abilities, small percent that can compete with you, very few that would be the fastest woman in the world, but still it's a representation of what can be done, what can be achieved. So I appreciate that.Lauryn: I feel like it's a representation of just, like you said, reaching your full potential. We get to take the main stage, but everybody can reach their full potential in whatever it is that they're doing. You can be the best heart surgeon, you can be the best janitor, you can be the best school teacher and change a third grader's life. And I think that's what the Olympics inspires, but I think that's what we all need to be striving for in life. What does it look like to be a gold medal person as far as reaching your full potential and contributing whatever you can to the world?David: As one of the greatest American athletes of all time and a certified financial planner, what's the one financial lesson you wish every athlete understood before stepping onto the world stage?Lauryn: I think the most important piece of the puzzle is that all aspects of your finances work together. There's no one piece that doesn't affect another piece, and so you need to be looking at yourself in a holistic way. And that's what I think more planners need to do. Like I said, we get so caught up in one piece of the puzzle, like, invest, invest, invest. But what about this debt we talked so much about today? What about those student loans? What about you want to buy a home? What about your kids' 529 plan? Every little piece of the puzzle matters in the same way that we create a championship plan for ourselves to be able to compete. And it's not just, "Run as fast as I can."I am a world-class sprinter, but I had to think about how I was eating. I had to think about how I was sleeping, when to travel, how many days to get there before, how much water to drink. Those things were all very, very important. When I was going to eat crazy amounts of dessert or things like that. Stress levels. How is your family treating you? All of it played a role in me being able to compete. In the same vein, all aspects of your finances are going to work together for you to be able to win at whatever your financial goals are.We usually talk about financial goals in the realm of retirement, but that's not the most important thing to a lot of athletes anymore, or not a lot of people. I say, "What does retirement mean?" and they're like, "I love my job. I'm never going to quit. I'm planning for when I can't work because you're telling me to, Lauryn, but I hope that I can do this till I'm 90. I really love my work in that way."Or they want to go to part-time. They've never seen their parents retire. These words don't mean the same thing as, like you said, traditionally they have been. And so creating a financial plan considering all the pieces of your puzzle is going to be the most important thing. And don't be afraid to talk to somebody about what's important to you because it is going to have some sort of financial implication, and you can build a plan that is customizable to whatever it is that you're trying to accomplish. And it doesn't have to fit inside the box of what, like you said, all these benchmarks that the world throws at us.David: I feel like I'd be remiss if I didn't ask you this question. How would you define success and how do you achieve it?Lauryn: This is a very good question. I would say, for me, success is defined by feeling happy about what I'm doing. And so you're doing things. Everybody has to do stuff on a day-to-day basis, but a lot of people describe it as like, "Can you sleep at night?" I want to go beyond just being able to sleep at night with the work that I'm doing. I want to feel excited about it. I want to feel invigorated by it. And getting up each and every day to be able to do something that I love and I'm able to pursue something that I love, to me is the success.It's not about being able to earn $1 billion, or $1 million even, for that matter. It's about being able to make a meaningful difference and feeling excited when I hang up the phone. "Hey, I just talked to David today and some athlete might hear this podcast and actually change the way they think about money because of it." I'm not saying yes to anything that's not making me feel invigorated, not making me feel like I can share in a way that's going to make an impact and ultimately make me feel happy. So to me, success equals happiness.David: Do you think you can achieve that success without a degree of discipline?Lauryn: Ooh. No. No, you cannot. No matter what it is, even if it's something more intangible in the way that I've described, you've got to work to be happy. And so if happy is what I'm describing as success, there are things that are going to come up against you each and every day that could make me unhappy or threaten that happiness. I mentioned student loans being, like I said, part of my expertise. I really love that work because I can change somebody's life in 60 minutes with what they did not understand about their student loan situation, and it makes me happy. But what happens if I'm not disciplined, I don't understand what's happening in student loans, I can make a mistake. I can cost people tens of thousands of dollars. And then the student loan system is changing on a regular basis. It's very political and real humans are being tied up in that, and that doesn't make me happy.But I have to be able to reframe, instead of being frustrated about what politicians are doing, into saying, "What can I do to continue to make people happy?" And like I said, the work that I'm doing to untangle what is a very messy situation is what takes the discipline, the discipline to get up each and every day when you're frustrated about a system that you can't fix, a system that— It's broken, to be quite frank. But I'm responsible for being disciplined if I want to be happy.David: You have achieved a lot. And I'm curious as we wrap up our conversation today, what is the achievement that you're most proud of?Lauryn: This changes on such a regular basis. I'm sure if you would have asked me 18 months ago I probably would have said something different. But I am a new mom and I did not know I would be a mom. I was kind of in the boat of like, "This timeframe is probably come and gone," and happy being the super aunt to my sister's two little ones. And now I am momming and it has changed the way that I think about everything. There is someone else that is counting on me to inspire her, to teach her, to protect her. And each and every day she's teaching me something. And I never would've thought that I would be in a position to just love this little thing so much. She's so happy, but also sassy already at nine months. And yeah, I am incredibly, incredibly proud to be her mom.David: Well, you've inspired us, and I don't think you'll have a hard time inspiring her. Thank you so much, Lauryn, for spending the time with us today and exploring your journey to becoming a world-class athlete. And we really appreciate your time.Lauryn: Thank you for having me on the show, David.* * *

You've been listening to the McAlvany Weekly Commentary. I'm Kevin Orrick, along with David McAlvany, and I hope you enjoyed the interview with Lauryn Williams. You can find us at mcalvany.com and you can call us at 800-525-9556.

* * *