More

Presented by Doug Noland since 2012

* * *

Kevin: Welcome to the McAlvany Weekly Commentary. I'm Kevin Orrick along with David McAlvany.I have gone back multiple times, Dave, to the webinar that you and Morgan and the other guys gave. And there are some key questions that we continue to receive, like, can gold have a meaningful rise if the consumer doesn't actually enter the market? And, how high do we think gold might go when it does go? Those are questions that you all went into detail on. I'd like to go back and look, during this particular Weekly Commentary, at some of those key moments.David: Kevin, with the Commentary, we're always looking for the appropriate framing and wanting to establish a healthy context so that investors can have a different appreciation for the dynamics that are in the marketplace, and make wise decisions. It would be easy to get lost in one month, two months, three months of market volatility and forget the bigger picture. And so, just as a review, to look at regime shift, some of the most significant regime shifts in our lifetime that are happening now, that will have defined and will continue to define the direction of the gold market in the months and years ahead, I think that review is helpful, and the Q&A will be helpful as well.Kevin: Yes, Dave. And this is actually from our McAlvany Wealth Management webinar from a few weeks ago. And for the listener who wants to see more than what we're about to show today, we will put a link to the entire webinar in the comments below.David: The rage today amongst investors, both professional and non, are data centers, are large language models, AI, semiconductors. And as we witnessed with the launch of SpaceX in recent days, the rage is companies that are likely to transform how we vacation on the moon and visit our intergalactic in-laws. These abstractions, enabled by ones and zeros and truly spectacular engineering feats, do have value, but not without reliance on practical physical realities—practical realities like energy, industrial commodities, construction materials, agricultural commodities, precious metals.Today, faith in the abstract may prove to be perfectly legitimate, may even extend to cryptocurrencies and quantum computation. But never forget, never forget that price is what you pay, value is what you get. If you overpay, you are likely to have performance problems with your portfolio. Prices paid for today's most popular investments are a performance problem in the making. Kevin Warsh, the newly elected Fed chair, recently shared that AI, in his opinion, will be the source of the next economic miracle, a miracle of productivity. Maybe he's right. Time will tell. What we are interested in, and we'll spend some time just discussing today, are the perceived fallen angels within the markets, and a particular kind of halo that only those hard asset companies can wear. So, let's dive in.* * *

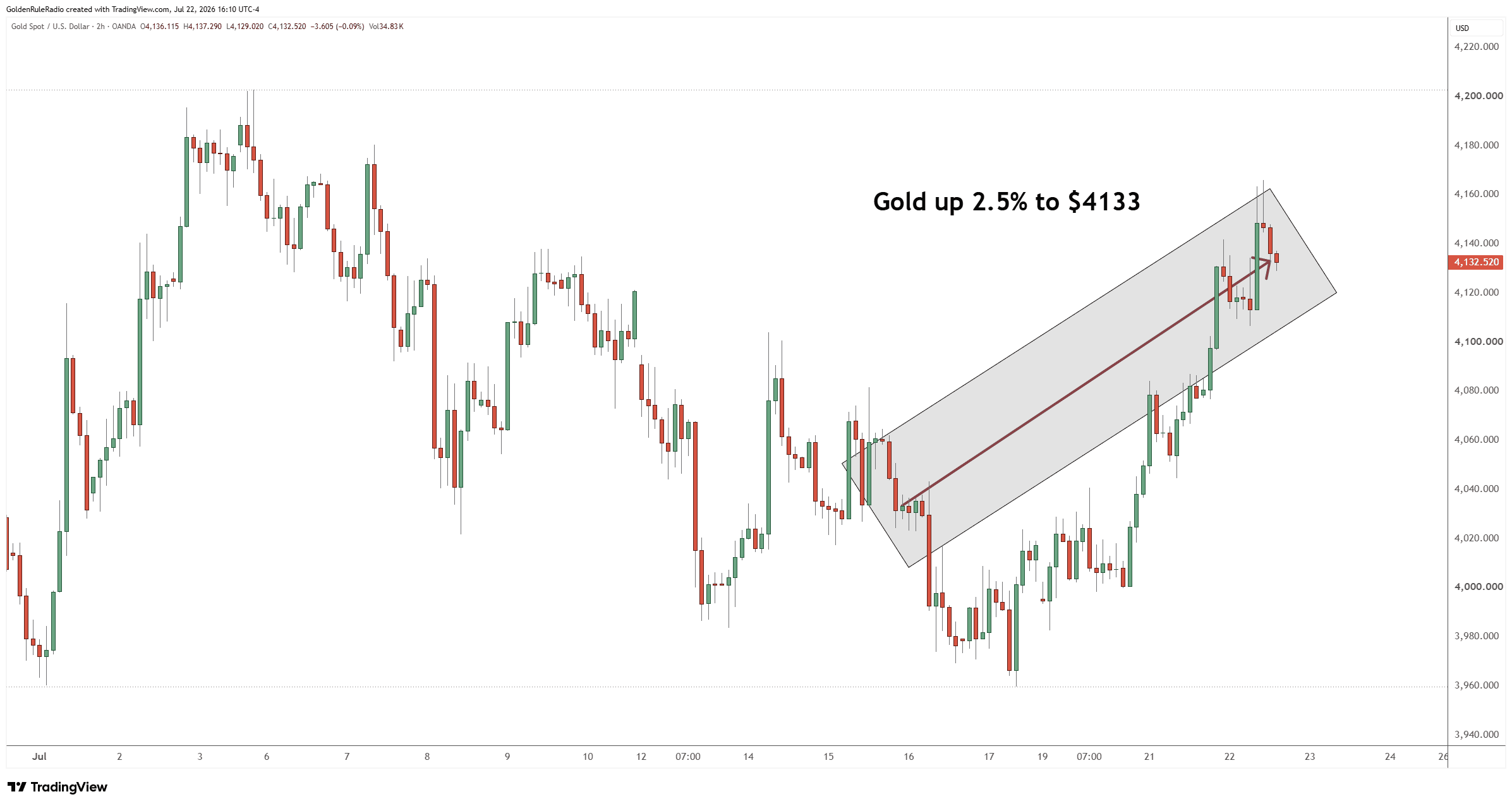

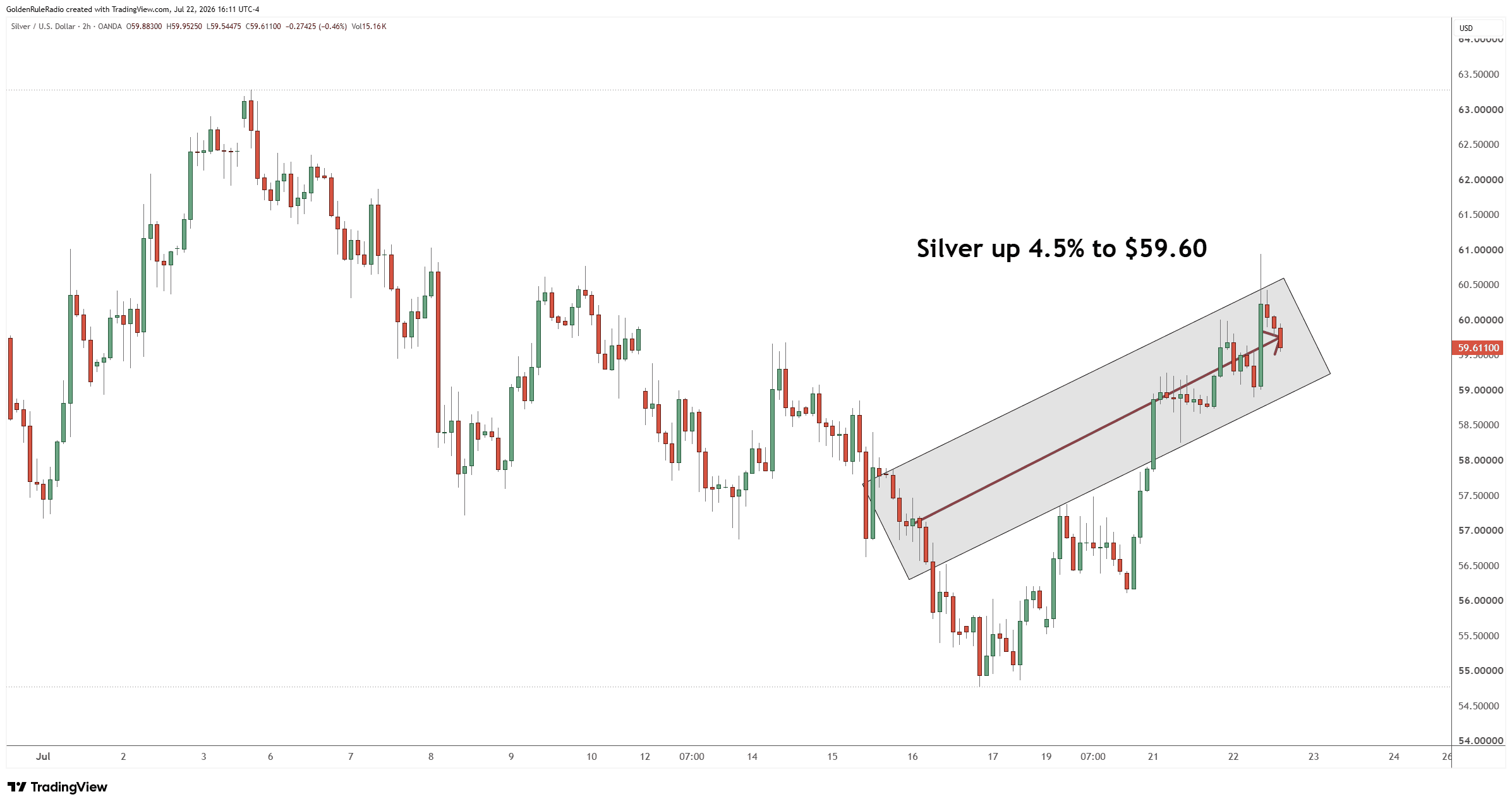

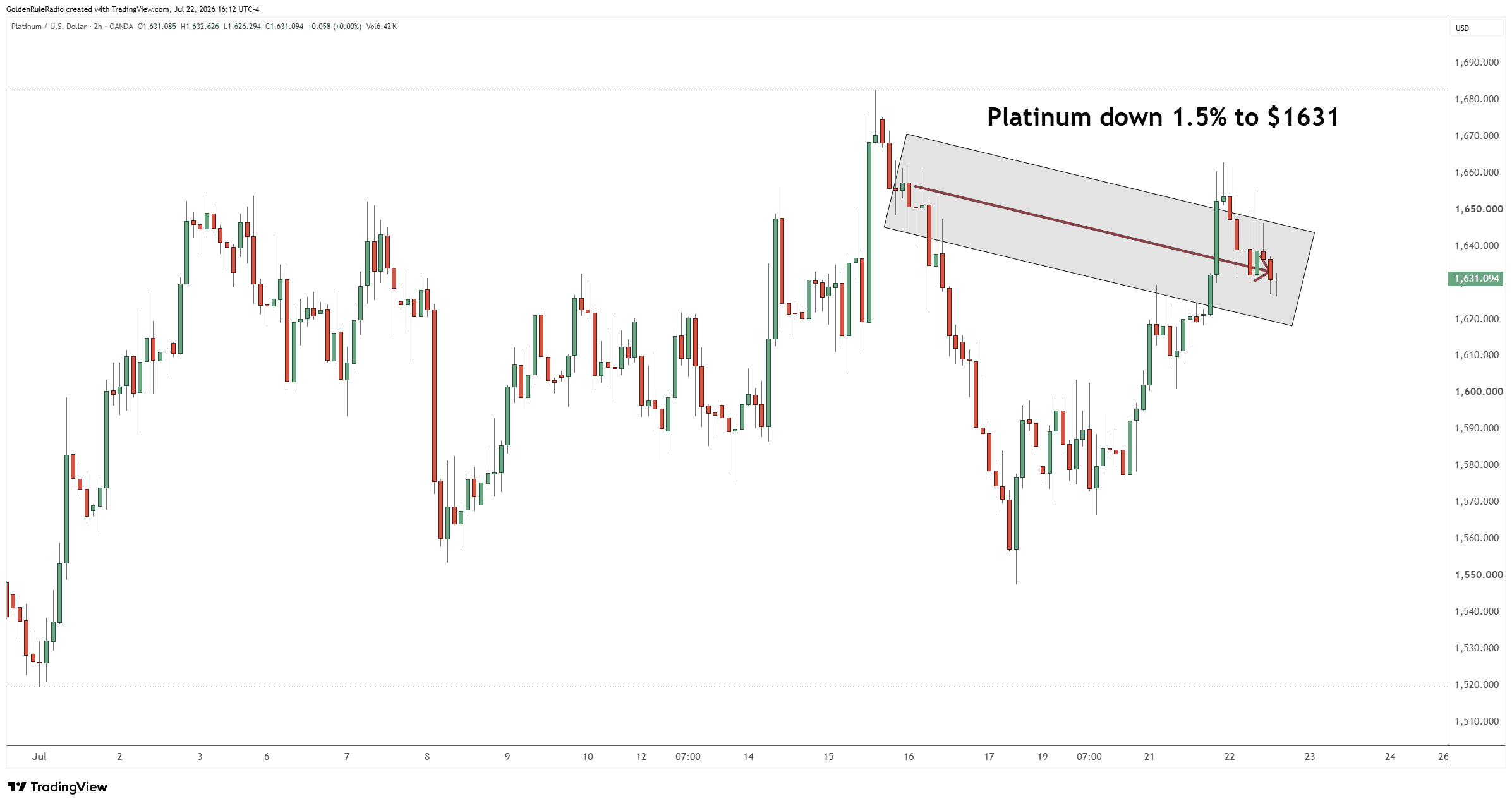

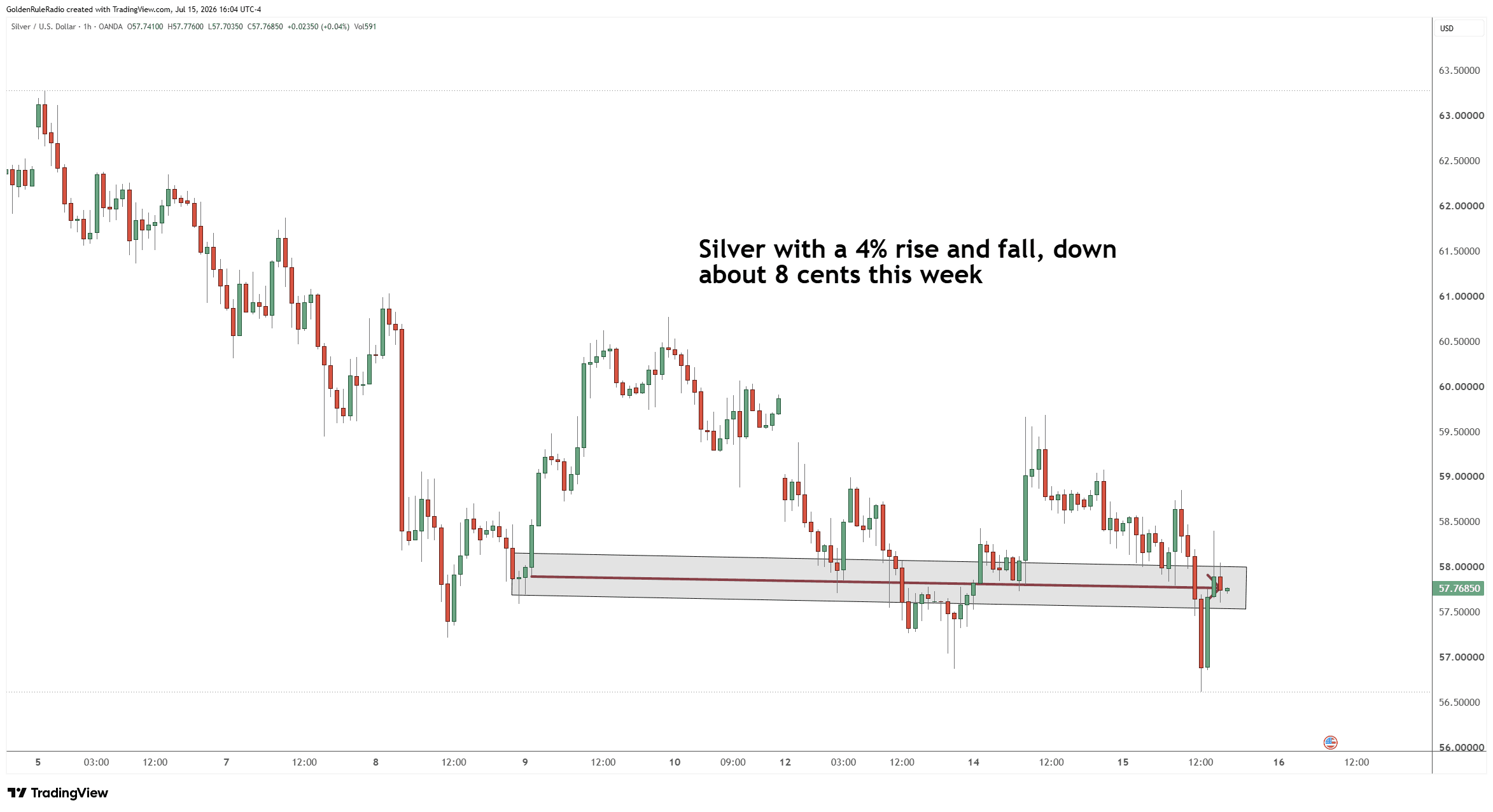

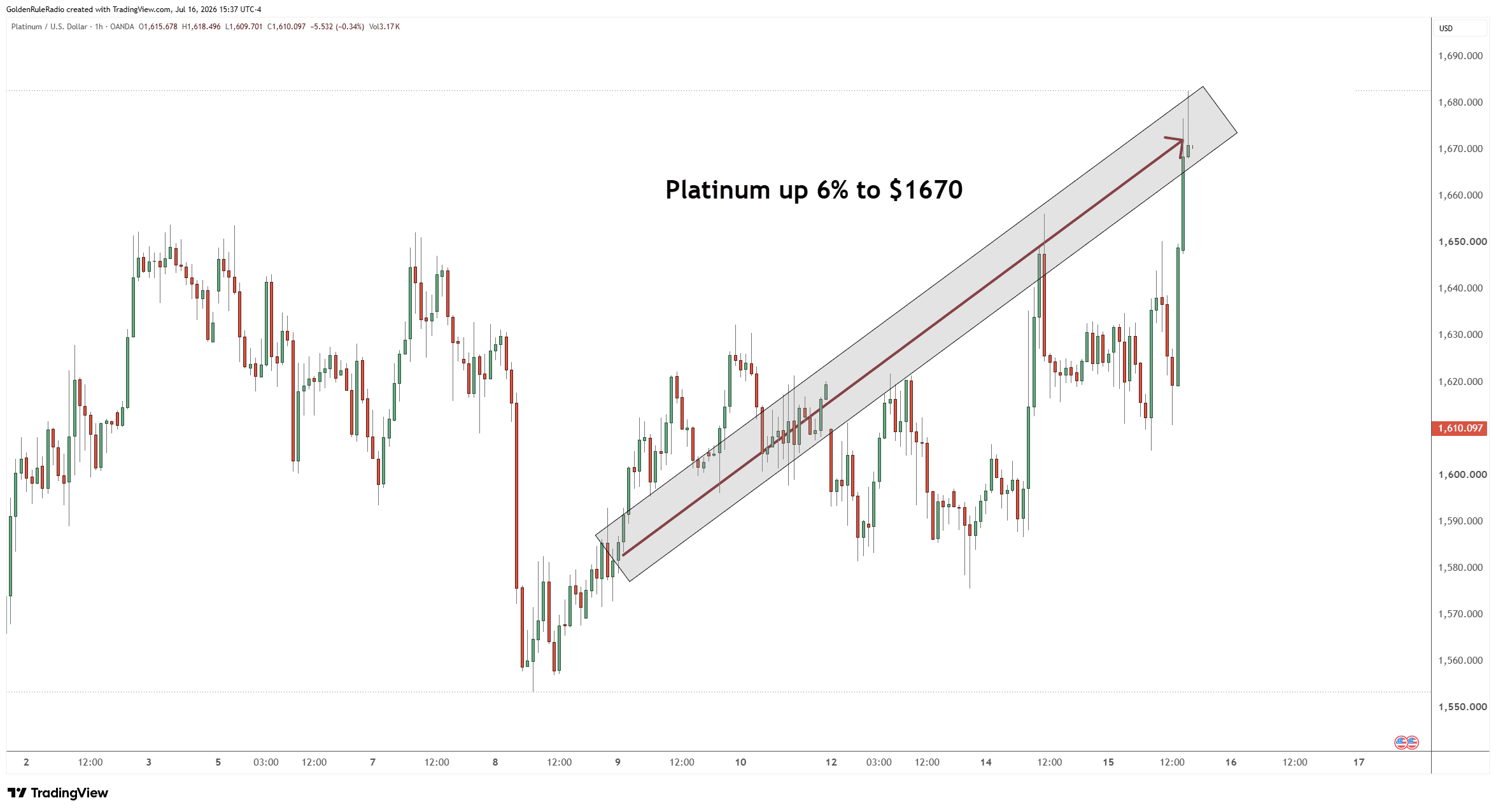

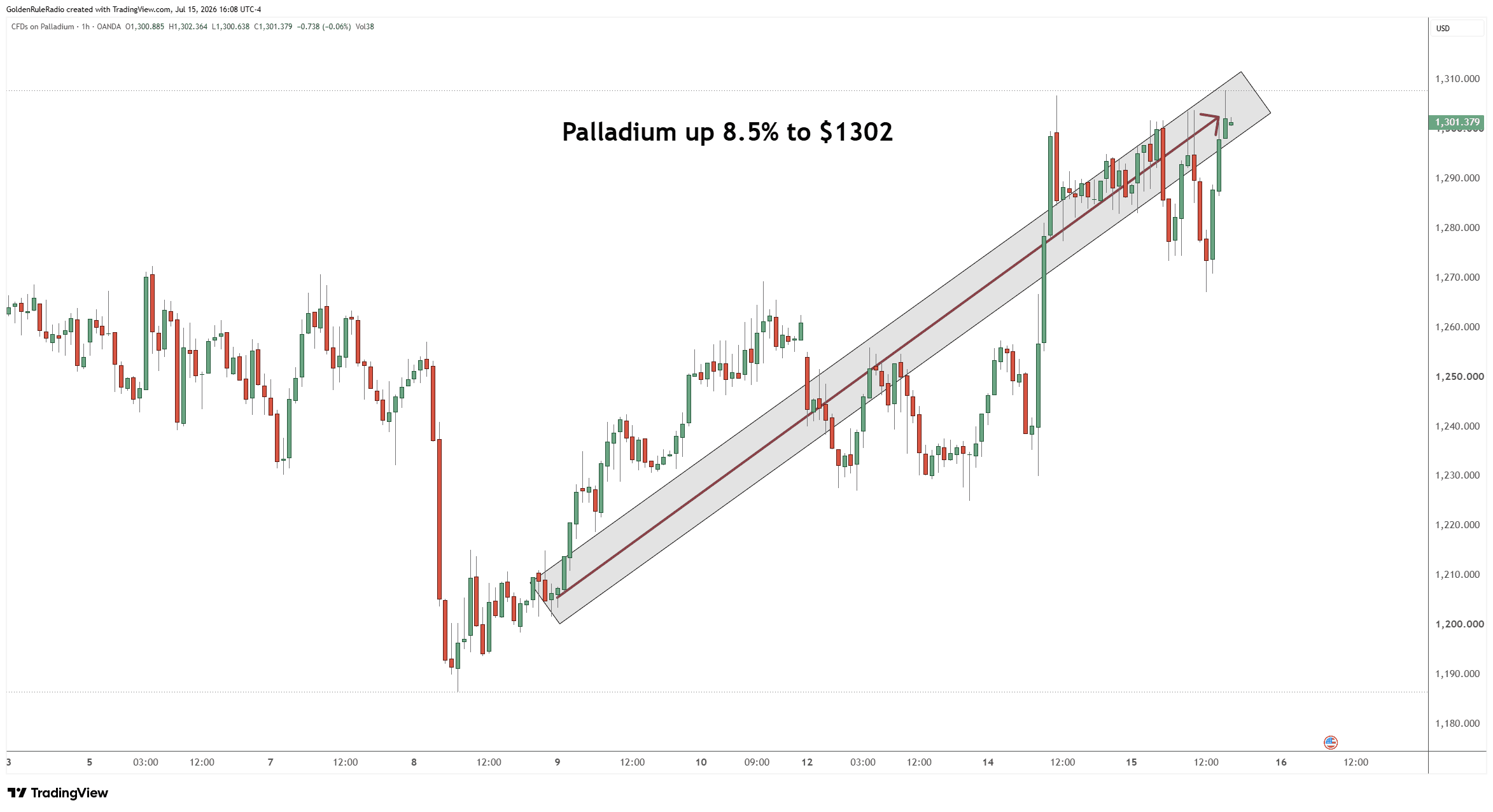

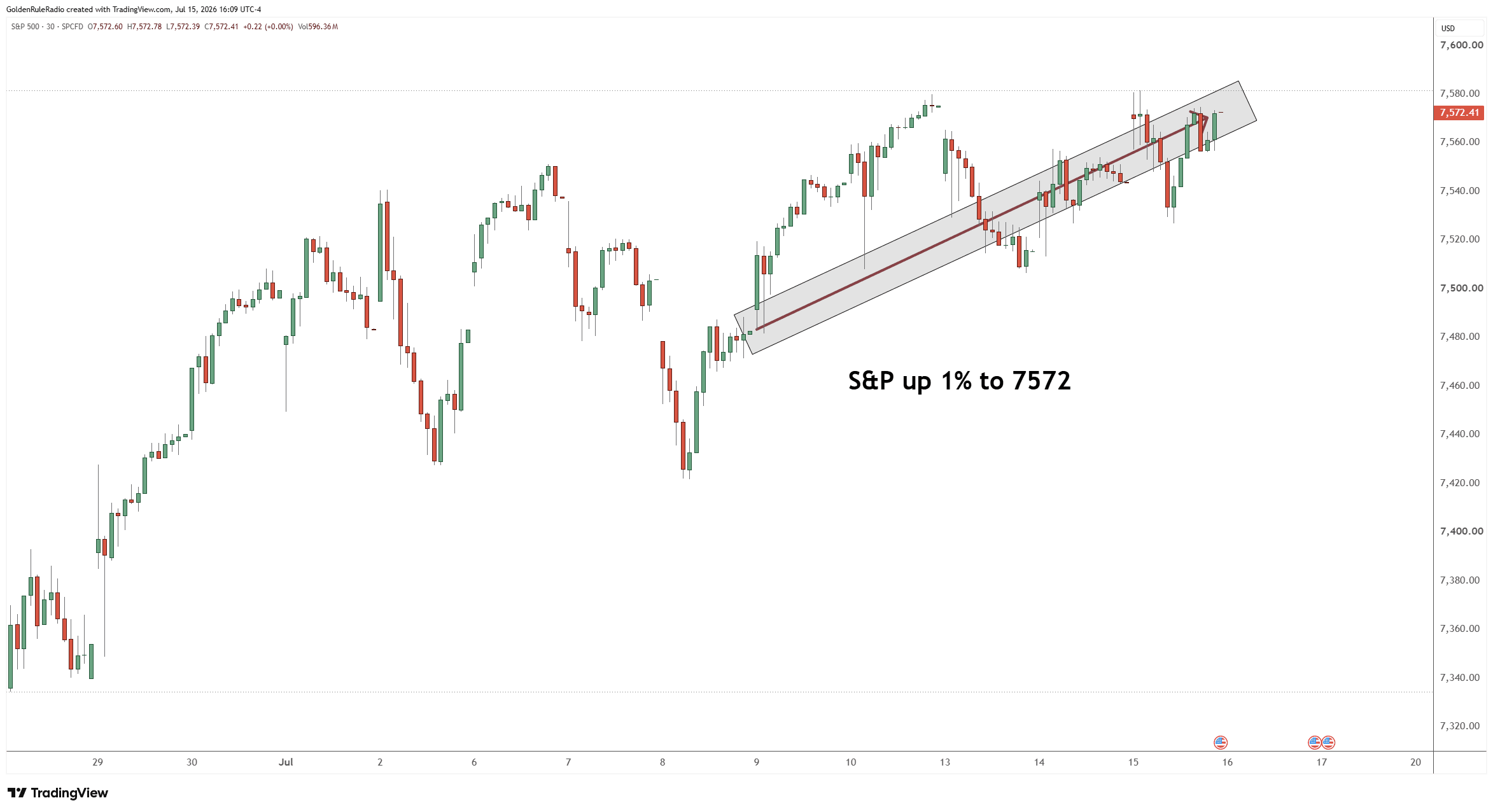

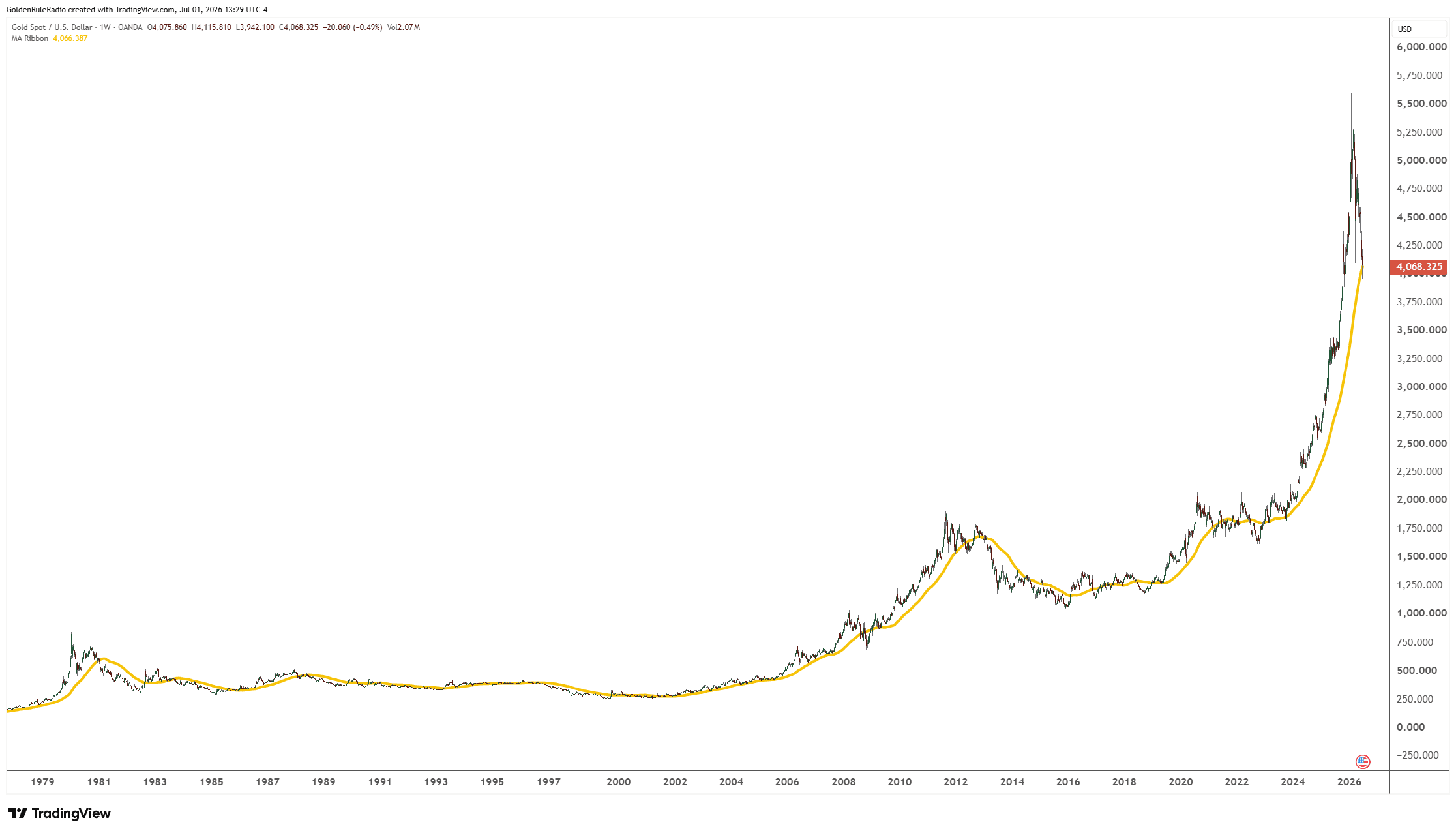

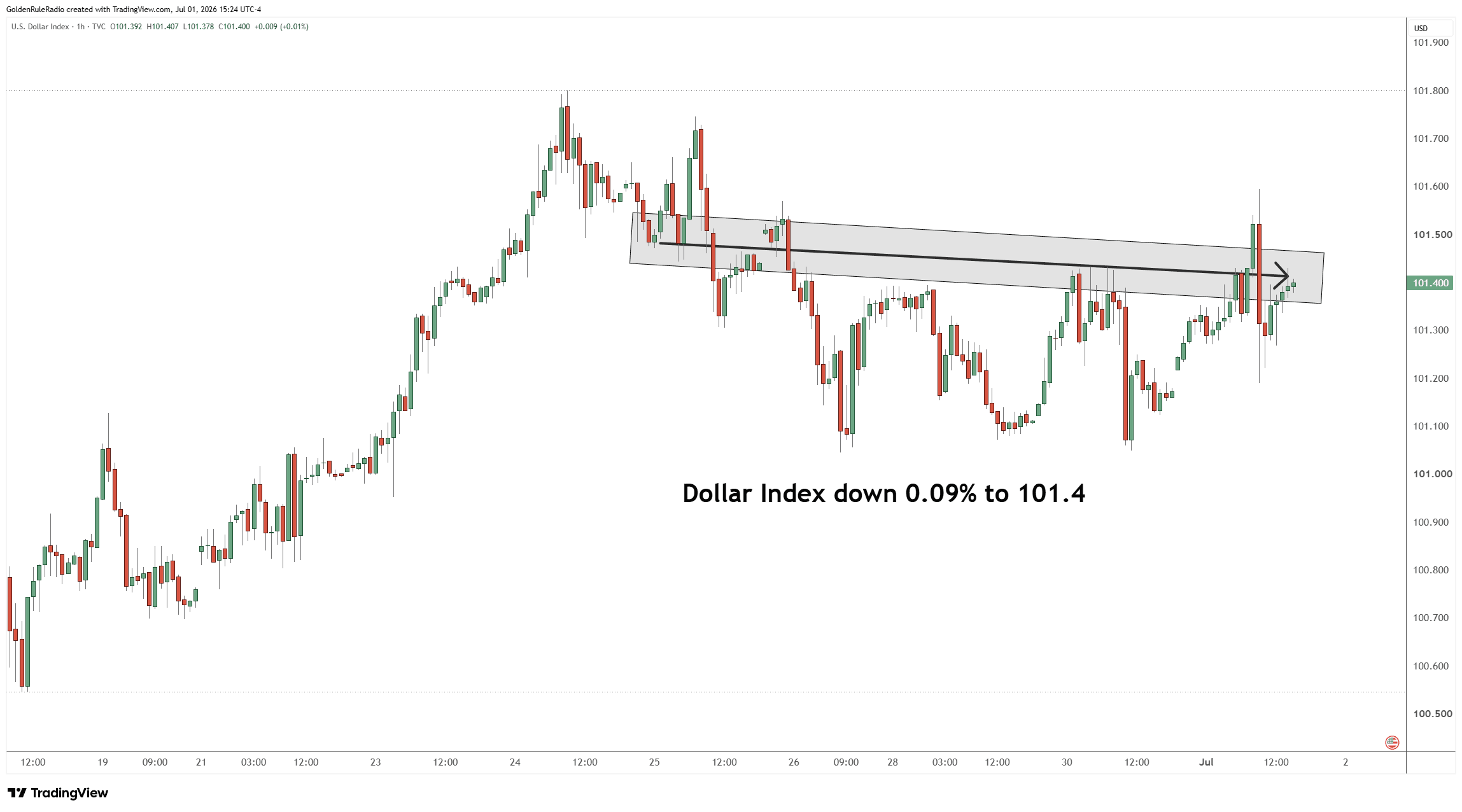

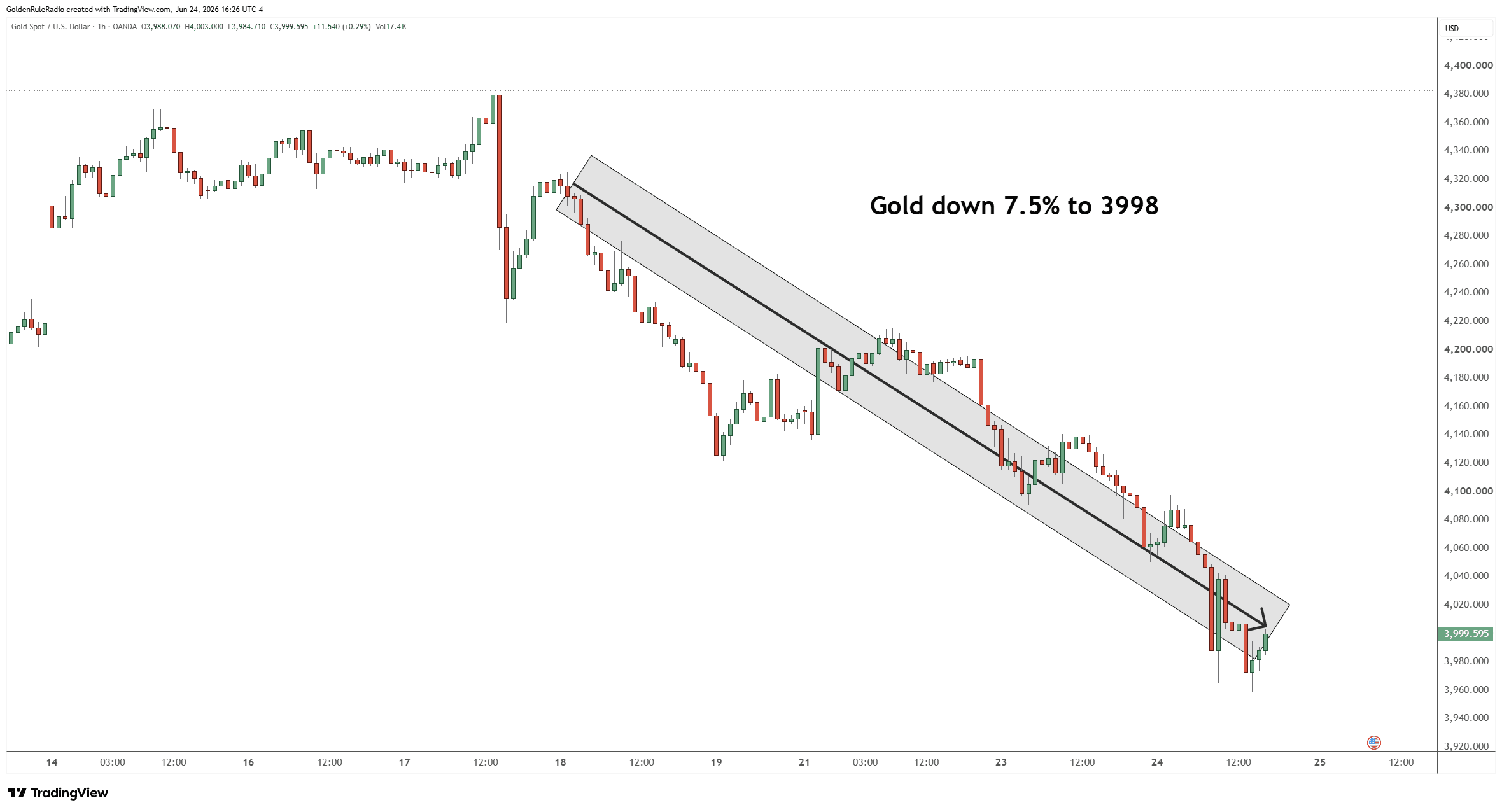

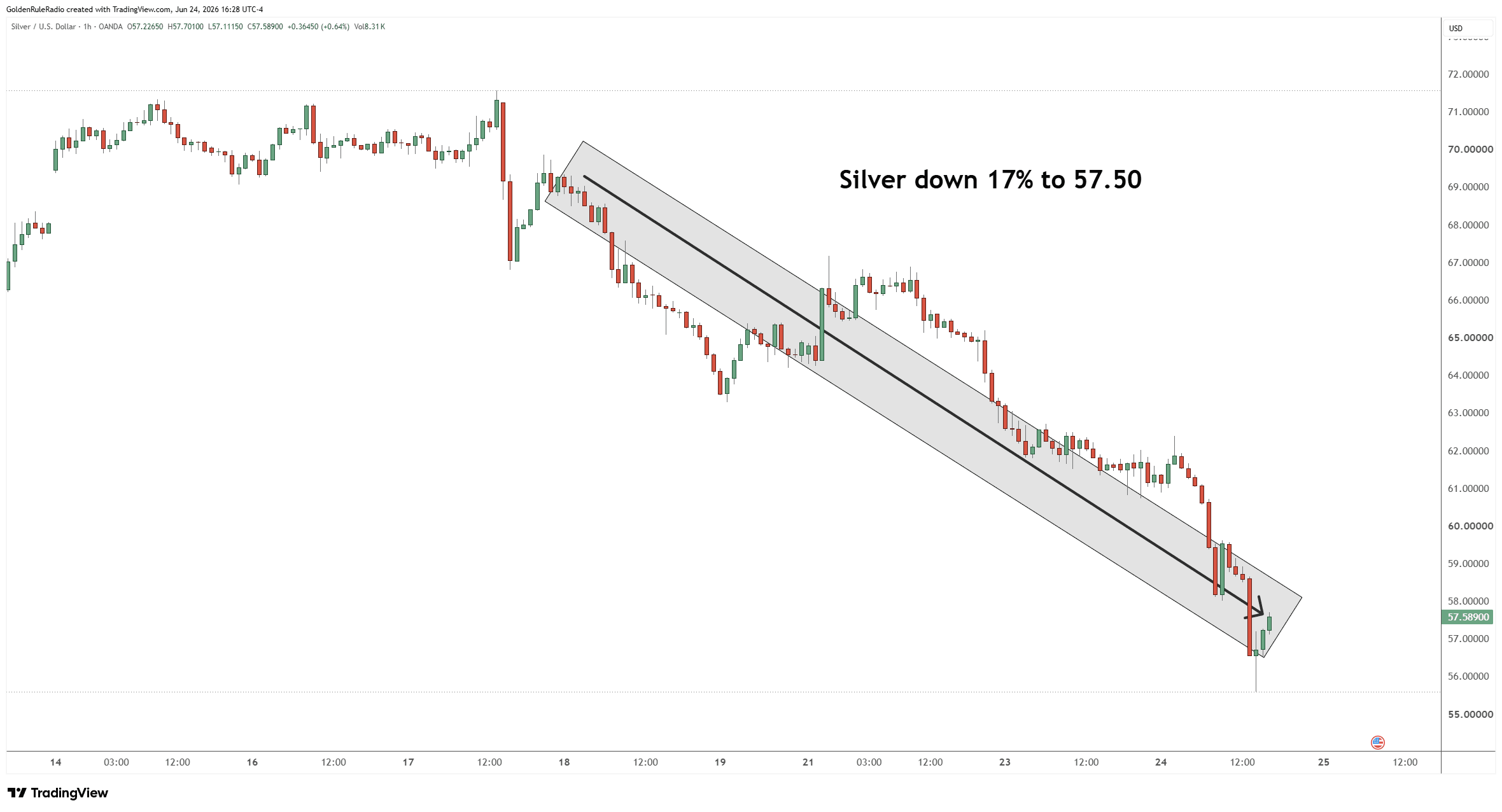

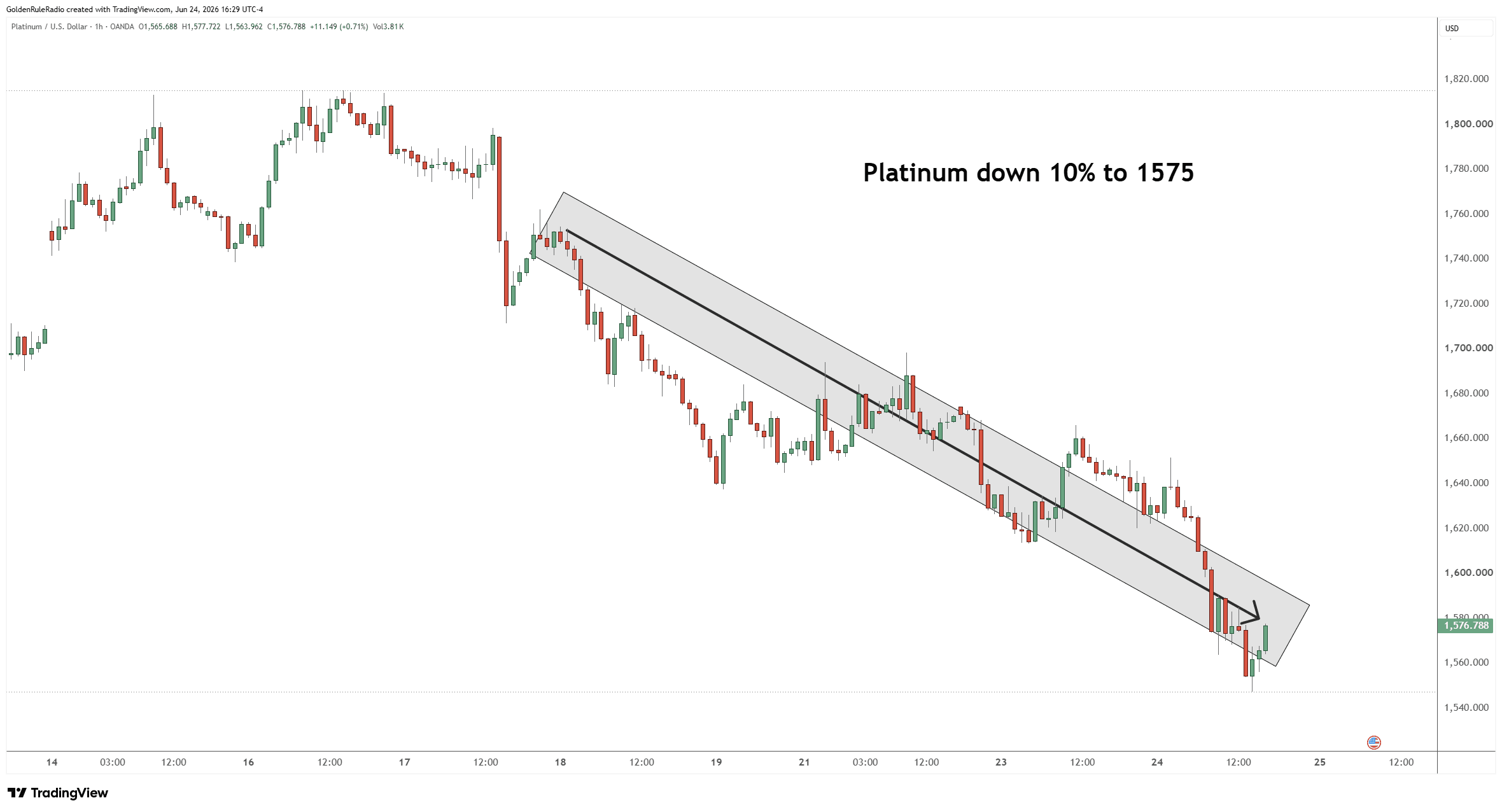

David: March 29th marked the lows in the equity market. Massive rally at month end and quarter end was spurred by headlines and announcements of the war ending soon, along with massive derivative short covering. US GDP was recovered, has recovered from the fourth quarter slump. We had the government shut down, which left its mark in the fourth quarter, about a half a percent growth, shrinking the full year number to 2.1%. Real Q1 growth has been revised lower to 1.6% with the Atlanta GDP marking the last several months closer to 4%. And last week's GDPNow figure from the Atlanta Fed has shrunk yet again to 2.8%.The White House very enthusiastically points to 5 to 6% GDP growth by year-end. Probably aggressive, in our mind. Bear in mind that the White House uses nominal GDP, which ignores inflation. Thus, the difference between what is reported and projected, they're like nominal versus real.Business investment was massive, has been this year, was setting a record pace last year and we're blowing out those numbers so far this year. So, business investment in Q1 surged to an annualized 8.6%, largely attributable to the AI CapEx arms race. Government spending also very significant, increased by 4.4%. Consumer spending remained anemic at 1.6% growth.The big theme, AI, CapEx spending. No limits budgeting for competitive AI edge, regardless of near-term returns on investment. Near term in that space is years, even 10 to 15 years out. When you combine government spending with business CapEx investment, it's no surprise that GDP as a measure of economic health is as strong as it is. Throw in the wealth effect for good measure as liquidity gets recycled through the economy, through the financial markets and into the economy over and over again, and GDP growth remains positive.The GDP deflater, which is the inflation assumption used in GDP, is not the same as CPI, not the same as PPI or PCE. And in fact lowballs the inflation issue, marking inflation at less than 3%. So frankly, if a more realistic inflation number were used, GDP growth would be closer to zero. Another bump in inflation, and I think we have real GDP in the negative territory. In that context, you're talking about stagflation. What GDP does not reflect is the bifurcation of experiences within the economy. Economists refer to the K-shaped economy, which captures this bifurcation along socioeconomic lines.The upper end of the K is your upper middle and upper classes. They're asset rich, they have buoyant balance sheets, which are enhanced by asset inflation, driven by ample liquidity in the financial markets. And of course this translates into spending numbers. The top 10% of wage earners account for 50% of all consumption—consumption making up nearly 70% of GDP. If you contrast the upper part of the K with the paycheck-to-paycheck crowd, the lower extended leg of the K is feeling the pinch from consumer price inflation without the offsetting increase from stocks and other investments. So, there's no wealth effect for most Americans.For middle America it already feels like recession, and sentiment indicators reflect that very strongly. Again, using a more realistic inflation number reveals that the average American is feeling the pinch. And it explains the University of Michigan sentiment numbers, which are at record lows, below the levels we reached during COVID if you can believe that.Enter the energy shock, and just remember that official inflation statistics were in fact creeping higher prior to the Mideast conflict. But with a reduction of 15 to 20% of global oil supplies, you now have inflation saturating the economy. CPI, PCE, and PPI, the wholesale price inflation index, all reflect higher levels of inflation. And over the last 90 days, the expectation of rate cuts have flipped to rate hikes. 100% probability of a hike by year-end, 67% probability of two hikes by this time next year. If you're watching the rate markets after the Warsh commentary today, the rates markets are expecting higher rates. Inflation brings a host of economic impacts and financial market complications, which will become obvious as the year proceeds. Morgan will discuss Fed monetary policy and bond market implications a little bit later.Not to get off track, inflation is not the only problem the bond market is dealing with. Yes, a 4.2% CPI print, 6.5% PPI print, they're meaningful, particularly for the bottom of the K-shaped economy, but too much supply—this is the big issue—too much supply and waning demand is also pressuring interest rates higher regardless of Fed monetary policy. Bonds face bear market dynamics, which many investors will in fact be surprised by.As for equities, I'll provide a few highlights. In summary, we are negative on the big indices like the S&P, the Dow, and the NASDAQ. This is in stark contrast with hard asset-related equities where we remain very bullish.Breadth in the main indices has narrowed. Only a few names are carrying the indices to new highs, which is never a healthy dynamic. Again, breadth is this [indicator of] how many companies are on the move to the upside. When there's only a few, that's an unhealthy dynamic. 50% of the year-to-date gains in the S&P 500 are from five companies.Valuations are between two and a half to three standard deviations from the mean. And on that basis, expected returns will hug the low single digits going out a decade. We look at the Shiller PE, we look at price to sales, we look at market cap to GDP for those valuation metrics.Examples might be helpful here. The median price to sales for the S&P 500 is 1.6. It currently trades at a very rich three and a half times. Compare that to Nvidia at 20 times; at Palantir, 63 times; or SpaceX at today's pricing of over 110 times price to sales. This is why I suggest that expected future returns based on those valuation metrics will hug the low single digits going out a decade. You are overpaying for those kinds of hype narratives.So what do we like? Hard assets continue to make sense today. We have built that case over recent years. We have built a diversified portfolio of companies that fall into four categories, all a unique expression of the hard asset theme. Global natural resources, infrastructure, precious metals mining companies, and real estate exposures in the form of publicly traded REITs.Each of these categories is like its own portfolio within the total framework—four portfolios in one. In this new cycle, we are witnessing gold as the tip of the spear, leading to further sequential opportunities in hard assets as the markets adjust to regime change.The studies we've undertaken and the portfolio allocations we're pursuing are gaining traction. As they gain traction, they also gain an audience. As the audience grows and capital begins to flow, positions that we are squarely in are positioned for growth. From a Goldman Sachs report released March 24th of this year titled "The HALO Effect: Heavy Assets, Low Obsolescence in the AI Era," I quote, "After more than a decade of under‑investment, Goldman Sachs Research analysts believe that higher real yields, geopolitical fragmentation, and supply chain rewiring have shifted equity leadership back toward tangible productive assets. They introduce the HALO framework—Heavy Assets, Low Obsolescence—to identify companies that are less exposed to technological obsolescence."So, now we have an acronym: HALO. Goldman and others are concluding in 2026 what has been in our minds for some time. While hard assets, or heavy assets, as Goldman likes to call them, are fresh on the minds of investors concerned about the implications of AI, we arrived at the same conclusion for a different set of reasons.AI is one more buttress for our argument. Hard assets are capital-intensive. Hard assets have low obsolescence. Hard assets rest in the middle of a scarcity bullseye. Hard assets provide resilience and are of great strategic value. Hard assets are on the diversification path for investors wanting to move from crowded tech, called capital-light trades, to a capital-heavy undercrowded domain.Commodities are breaking away from a floor-pinned position and rising in relative value to the popular abstractions of our day. Capital-intensive businesses have been on the move for several years, but their performance has been largely obscured from view by the capital-light companies outperforming them with their value tied to abstractions like intellectual property and brands. Examples of Nike and Coca-Cola come to mind, or companies that are selling software as a service and data flow, Microsoft, Adobe, Salesforce, or your leveraged networks and platforms, Airbnb, Uber, and things like that.Our perceived fallen angels have some advantages, which, to many investors, look like disadvantages. Operational complexity, resource scarcity, high sustaining capital requirements, energy and labor intensity, regulatory constraints, massive permitting requirements, long project timelines, all of which, again, most people would see as negatives, but these qualities provide the moats and cyclical advantages we're looking for in a period of rising inflation and rising interest rates.As an example, picture the copper mine built 30 years ago for 1.5 to $2 billion. To replicate that copper mine today might cost 15 to $20 billion, not the domain of a startup company, unless you're SpaceX, of course. This is not new-world stuff. In fact, it's old-world stuff. But guess what the irony is? The new-world stuff still depends on the old world, and that is a sweet revenge. Over time, a replacement is prohibitively expensive, permitting becomes harder, environmental limitations increase, skilled labor, which is very, very blue collar stuff, it's harder to find. And the asset-heavy nature of the companies reprices upward during inflationary regimes.Morgan: Former Treasury Secretary under Presidents Nixon and Ford William E. Simon famously said, "I continue to believe that the American people have a love-hate relationship with inflation. They hate inflation, but love everything that causes it." Now, for the last 50 years, it is the structure of the post-1971 dollar-based global system, or petrodollar system, that's allowed US policymakers to do everything that causes inflation without reaping the full massive inflationary brunt of their policy consequences. But now that post-'71 monetary system is beginning to break down and we believe the Iran war is the latest significant accelerant of that monetary regime change trend. We expect the current conflict with Iran will have deep and long-lasting implications for the post-1971 US dollar-centric global system. And since the war started, we are not alone in that view. The Iran war seems to have been a catalyst for Western media to begin to awaken to the reality of global monetary regime change, and to China's central role in facilitating it.In late March, there was a Bloomberg article titled "Iran War Could Be Making of the Petroyuan, Deutsche Bank Says." Then in early April, Bloomberg Macro Strategist Simon White penned an article titled "Iran War Has Caused Lasting Damage to the US Dollar System." Both articles pointed to very real and growing strains in the post-1971 global US dollar system.Both articles focused on how the Iran conflict could be the catalyst for both erosion in petrodollar dominance and the emergence of a competitive petroyuan, citing media reports that Iran was allowing the passage of ships through the Strait of Hormuz only if oil payments were made in yuan. Furthermore, both articles warned that the erosion in the petrodollar regime could have "significant downstream effects" to the dollar's use in global trade and savings, as well as to the dollar's role as a reserve currency.Also in April, Peter Alexander, CEO of Z-Ben Advisors, a Shanghai-based consulting firm essentially aiming to bridge the information gap between West and East, penned a very important article on Substack titled "China's Killer (Geopolitical) App." In the article, Alexander adds great detail to both the threat of damage to the US dollar system and to the golden origins of the petroyuan.As Alexander put it, "For more than a decade now, the Beltway consensus held that the US dollar system operates as a geostrategic choke point that can be deployed to alter the behavior of other state actors. Books have literally been written on this very topic, and it may have been true for a moment in time.What has yet to be recognized is that, in present day, a US dollar choke point has, in fact, run up against hard limitations on its efficacy. The American move to nakedly weaponize the US dollar system was a message received by Beijing with immediate effect. The risk, no matter how remote, of China being blocked access to SWIFT was existential. A solution was required and the People's Bank of China was tasked with finding a workable alternative.In 2015, that task was completed and the cross-border interbank payment system SIPS officially went live. SIPS conducts all functions—again, via RMB—from messaging to clearing to initial fiat settlement. It also became the first system to seamlessly integrate payment and settlement of the onshore and offshore RMB, CNH and CNY.Perhaps more consequential when it comes to the great power competition, SIPS resides fully outside the New York correspondent banking network. The very parties that sought to apply economic coercion for the purposes of altering unwanted behaviors are now blind.Obviously the introduction of SIPS was meant to directly benefit China. It is now also the case that the network is providing an attractive solution to a host of global south countries in an era where the Trump administration has ratcheted up the deployment of coercive economic and financial tactics as points of leverage.Now, Western critics of the viability of a petroyuan argue that in a global US dollar-dominated system, participants in the SIPS network would be stuck with too much unwanted excess yuan. But there are two important rebuttals to that argument. First, over the last decade plus, China has undeniably become the factory of the world, meaning there is no limit to the menu of offerings foreign nations can purchase from China with yuan. Second, the SIPS network utilizes a gold-based or gold-linked yuan for neutral net settlement in an emerging network often referred to as the Golden Road.As Alexander explains, SIPS is just the payment network. With China's capital account opened via the gold window, any trading partner holding RMB surpluses can directly convert all fiat balances into physical gold. That gold can be held in a Shanghai vault well beyond the reach of America's foreign policy of sanctions and tariffs, as well as the newly opened Hong Kong vault and vaults soon to be expanded into Saudi Arabia, Singapore, Malaysia, and eventually additional hubs plan for Dubai and Russia.And in addition to acting as a neutral reserve asset and facilitating non-dollar trade settlement, the entire China gold complex is also being positioned to act as a substitute for another critical component of the US dollar system. In this new system, gold can replace, at least at the margins, the role of US Treasuries in acting as global collateral. While not as liquid as US Treasuries, the usage of gold as collateral is meant to be levered as a mechanism to support a host of cross-border trade activities, including usage as a financial tool for invoicing of any return trade of physical goods. Beijing has been executing plans for this entire gold settlement solution for the better part of a decade. Its overt objective is mitigating the inherent risk of America's leverage over the US dollar system. The system is functional. It's now operational. And it's now expanding rapidly. More recently, in late May the Financial Times also picked up on the emerging petroyuan story and elaborated on it.In a May 21st article titled "Iran War Open's Golden Window with China's Renminbi," the FT, like Alexander, explicitly tied the rise of the petroyuan to China's SIPS international payment system and its gold link. Furthermore, the FT referred to the Iran war as "proof of concept". According to the FT, "Gold could serve as a neutral asset for countries to recycle excess renminbi into allowing China to maintain capital controls while competing more with the dollar in global trade. China has regulated the Shanghai Gold Exchange with a strict settlement system. Exporters to China can receive payment in yuan and immediately convert excess yuan into gold bars on the Shanghai Gold Exchange International Board without using dollars, but with the security of a neutral asset." Importantly, the FT noted that, since the Iran War, adoption of Beijing's SIPS cross-border payment system is surging to record highs.And as I said before, that the Iran war has provided "proof of concept" for the SIPS system. According to the FT, the average daily value of transactions settled through SIPS hit a record of $135.7 billion equivalent per day in March, as well as a new daily record in April of $150 billion equivalent per day.For perspective, that April daily record would translate to roughly a massive $50 trillion equivalent annual run rate. In short, SIPs adoption is now booming. Now, over the past two months, a popular narrative to explain gold's recent sell-off has emerged. It suggests the war with Iran is fundamentally bearish for gold and that, as a result, the war has catalyzed official sector gold sales. Now it is true that some nations did pare gold holdings in the first quarter. A number of central banks and sovereign wealth funds shed an estimated 115 tons in the first quarter of 2026, but the vast majority of those sales were one-time events mostly attributed to liquidity effects stemming from the closure of the Strait of Hormuz.Those sales, combined with the negative price action, raised concerns about institutions' appetite for gold and their interest in continuing the dedollarization trend. But a Bloomberg report may fully dismantle that gold-negative narrative, as in reality, even net of previously mentioned gold sales, Q1 net central bank purchases totaled 244 tons, up from 208 tons in the previous quarter, marking the fastest pace of central bank gold buying in almost two years.Again, the 244 tons was a net purchase number. It includes the 115 tons of one-time Hormuz-related gold sales. The red extension line on this slide displays the actual 359 tons of Q1 central bank gold buying if you adjust out one-time Hormuz-related sales. And after adjustment, Q1 was essentially tied for the third-largest quarter of central bank gold purchases on record. And in MWM's view, it's no mistake that such a strong quarter of central bank gold purchases occurred alongside record-breaking levels of average daily values of SIPS network transactions.In short, the Iran war didn't launch the SIPS gold-based petroyuan, but is proving what the FT called a proof of concept. And it is proving to be the catalyst for a dramatic acceleration of the global recognition and adoption of the SIPS gold-based petroyuan. In sum, the non-dollar energy and commodity trading system that net settles surpluses into gold that former Goldman Sachs Head of Commodity Research Jeff Currie first described as gold recycling replacing dollar recycling two years ago continues to gain notable traction in the East and growing awareness in Western financial and media circles.In MWM's view, when gold's technical correction ends, the next leg of the gold bull market is likely to be greatly enhanced by the growing recognition among Western investors of global monetary regime change dynamics.With Kevin Warsh and the Fed facing a bond market crisis while their policy hands are tied, and the gold-based rails of an alternative non-dollar global system beginning to hit its stride, MWM is confident that we don't have to wait long for the gold bull market to shake off the ongoing technical correction and resume trend to new all time highs and beyond.David: I'll start with, "If the Fed increases rates and takes a more responsible fiscal policy, what does that mean for the gold price?" Morgan, you hit that squarely in your comments, but perhaps you could reiterate the standard assumption and what we've discussed in-house in terms of the Summers-Barsky thesis, how it would behave under one set of circumstances and why this time is different.Morgan: So basically Summers-Barsky is talking about gold basically moves inversely to real rates. So higher real rates makes gold less attractive and negative real rates makes gold attractive. But in our view, that dynamic is only fit for a healthy system. And I think we're far from a healthy system. So as I said in my presentation, I'm definitely of the mind that they may be able to hike interest rates 25 basis points, maybe 50 basis points, and maybe for a period of time. But we're at that point where the negative impact to the deficit via interest expense adding into government expenses and growing as fast as it is and ballooning as much as it has, you're talking about putting a debt spiral into motion if you allow real rates to go higher for longer.So I think those days are done, and I don't think they can— Part of the question was, I believe, is if they get more austerity in their fiscal policy. And that's also problematic for them because for one thing we're increasing defense spending, not cutting it—dramatically in fact, the plan is.And then we're not going to cut entitlements for political reasons. And also we aren't going to cut spending really because if we did at this point, government spending is such a large part of GDP that you would very likely trigger a recession. A recession means lower tax receipts. The stock market falling means the capital gains taxes drop. And again, that just feeds into the circular nature of the debt spiral dynamic. So I don't think there's really— I mean, I think practically speaking there is the cap yields and inflate your way out of this, is practically speaking what we're ultimately dealing with.David: The next question I'll take. "What does the price of gold look like in the future if retail investors do not participate in gold in a meaningful way even as government debt levels increase, the economy suffers, inflation interest rates remain at current levels or even increase?"I think the best analog for that is what we've witnessed from 2022 through 2025, where we basically had a $2,000 increase in the price of gold with virtually no participation from the general public. You could argue, and if you look at ETF statistics, there was a significant uptick in retail demand from the middle part of 2025 through the end of last year and into the beginning of this year. So retail did show up. But if you wanted to know what the price of gold looked like without the retail investor, central bank demand has been absolutely critical to driving the price. That 2,000 point move higher from 1,650, 1,800 to over 4,000 an ounce, largely attributable to central banks doubling their purchases from a run rate which was 500 tons per year and has been averaging at or above 1,000 tons a year since 2022.Central bank demand is not a forever thing, but we do see that continuing over the next several years. Morgan illustrated what the motivation would be from the standpoint of—well, I just mentioned from the standpoint of reserve management and what central banks want as a denomination for their reserves. And Morgan hit on how gold demand would be very central to a system of trade which does not settle in dollars and does not promote recycling of trade dollars or petrodollars into the US Treasury market. So that alternative system is yet another source, which is trade related, not retail or investor related.I do think that retail comes into the gold market at some point. And what we have witnessed in past bull markets in metals—we've been in the metal space for 54 years—and what we've witnessed there and even prior to that, if you wanted to stretch back 50 to 100 years or more, is that retail chases gold when it's afraid of something else. And so if that's volatility in the equity market, if that's volatility in the bond market, safe haven dynamics ultimately kick in. And today you don't see the need for it as people clamor for the newest, shiniest gizmos, gadgets, and solutions via AI.So when those markets turn, if those markets turn, I think retail has a motivation to diversify their own reserves, so to say, and look at it as a safe haven. But the moves in metals are not dependent on retail. I think central banks have defined the floor in gold. Retail will ultimately blow out the ceiling, which is a chapter yet to be written.The next question, "Have you seen the price estimates for gold in July of $20,000 an ounce or $1,500 an ounce for silver?" I have seen those. Of course, being in the metals business for 54 years, we've seen all kinds of projections over time. And what we would suggest is that a Dow/gold ratio of two to one or three to one is very reasonable. And so if you assume the movement of numerator and denominator, both of those things moving toward each other, you could see gold in the range of 15,000 an ounce. 12,000 I think is not unrealistic. 15,000 becomes a high watermark.Perhaps we could see 20, but I think you're beginning to really wonder at that point—at any point higher than that—if the true commentary is not supply and demand, but just reflecting a broken currency like we've seen with the yen. One ounce of gold trades for 750,000 yen. Is that particularly meaningful? Well, it is if your savings are based in yen because you've preserved your purchasing power as the currency has gone through a veritable meat grinder.So at some point prices become irrelevant. It's one of the reasons why I think looking at the Dow/gold ratio and looking at relative values is super important because we may be looking at the Dow at 150,000 and gold at, again, a three to one ratio, 50,000. You know the high price based on relative value, not nominal pricing in the context of competitive currency devaluation.* * *

Well, you've been listening to the McAlvany Weekly Commentary. I'm Kevin Orrick, along with David McAlvany. You can find us at mcalvany.com and you can call us at 800-525-9556.* * *

This has been the McAlvany Weekly Commentary. The views expressed should not be considered to be a solicitation or a recommendation for your investment portfolio. You should consult a professional financial advisor to assess your suitability for risk and investment. Join us again next week for a new edition of the McAlvany Weekly Commentary.* * *

Kevin: Welcome to the McAlvany Weekly Commentary. I'm Kevin Orrick along with David McAlvany.I have gone back multiple times, Dave, to the webinar that you and Morgan and the other guys gave. And there are some key questions that we continue to receive, like, can gold have a meaningful rise if the consumer doesn't actually enter the market? And, how high do we think gold might go when it does go? Those are questions that you all went into detail on. I'd like to go back and look, during this particular Weekly Commentary, at some of those key moments.David: Kevin, with the Commentary, we're always looking for the appropriate framing and wanting to establish a healthy context so that investors can have a different appreciation for the dynamics that are in the marketplace, and make wise decisions. It would be easy to get lost in one month, two months, three months of market volatility and forget the bigger picture. And so, just as a review, to look at regime shift, some of the most significant regime shifts in our lifetime that are happening now, that will have defined and will continue to define the direction of the gold market in the months and years ahead, I think that review is helpful, and the Q&A will be helpful as well.Kevin: Yes, Dave. And this is actually from our McAlvany Wealth Management webinar from a few weeks ago. And for the listener who wants to see more than what we're about to show today, we will put a link to the entire webinar in the comments below.David: The rage today amongst investors, both professional and non, are data centers, are large language models, AI, semiconductors. And as we witnessed with the launch of SpaceX in recent days, the rage is companies that are likely to transform how we vacation on the moon and visit our intergalactic in-laws. These abstractions, enabled by ones and zeros and truly spectacular engineering feats, do have value, but not without reliance on practical physical realities—practical realities like energy, industrial commodities, construction materials, agricultural commodities, precious metals.Today, faith in the abstract may prove to be perfectly legitimate, may even extend to cryptocurrencies and quantum computation. But never forget, never forget that price is what you pay, value is what you get. If you overpay, you are likely to have performance problems with your portfolio. Prices paid for today's most popular investments are a performance problem in the making. Kevin Warsh, the newly elected Fed chair, recently shared that AI, in his opinion, will be the source of the next economic miracle, a miracle of productivity. Maybe he's right. Time will tell. What we are interested in, and we'll spend some time just discussing today, are the perceived fallen angels within the markets, and a particular kind of halo that only those hard asset companies can wear. So, let's dive in.* * *

David: March 29th marked the lows in the equity market. Massive rally at month end and quarter end was spurred by headlines and announcements of the war ending soon, along with massive derivative short covering. US GDP was recovered, has recovered from the fourth quarter slump. We had the government shut down, which left its mark in the fourth quarter, about a half a percent growth, shrinking the full year number to 2.1%. Real Q1 growth has been revised lower to 1.6% with the Atlanta GDP marking the last several months closer to 4%. And last week's GDPNow figure from the Atlanta Fed has shrunk yet again to 2.8%.The White House very enthusiastically points to 5 to 6% GDP growth by year-end. Probably aggressive, in our mind. Bear in mind that the White House uses nominal GDP, which ignores inflation. Thus, the difference between what is reported and projected, they're like nominal versus real.Business investment was massive, has been this year, was setting a record pace last year and we're blowing out those numbers so far this year. So, business investment in Q1 surged to an annualized 8.6%, largely attributable to the AI CapEx arms race. Government spending also very significant, increased by 4.4%. Consumer spending remained anemic at 1.6% growth.The big theme, AI, CapEx spending. No limits budgeting for competitive AI edge, regardless of near-term returns on investment. Near term in that space is years, even 10 to 15 years out. When you combine government spending with business CapEx investment, it's no surprise that GDP as a measure of economic health is as strong as it is. Throw in the wealth effect for good measure as liquidity gets recycled through the economy, through the financial markets and into the economy over and over again, and GDP growth remains positive.The GDP deflater, which is the inflation assumption used in GDP, is not the same as CPI, not the same as PPI or PCE. And in fact lowballs the inflation issue, marking inflation at less than 3%. So frankly, if a more realistic inflation number were used, GDP growth would be closer to zero. Another bump in inflation, and I think we have real GDP in the negative territory. In that context, you're talking about stagflation. What GDP does not reflect is the bifurcation of experiences within the economy. Economists refer to the K-shaped economy, which captures this bifurcation along socioeconomic lines.The upper end of the K is your upper middle and upper classes. They're asset rich, they have buoyant balance sheets, which are enhanced by asset inflation, driven by ample liquidity in the financial markets. And of course this translates into spending numbers. The top 10% of wage earners account for 50% of all consumption—consumption making up nearly 70% of GDP. If you contrast the upper part of the K with the paycheck-to-paycheck crowd, the lower extended leg of the K is feeling the pinch from consumer price inflation without the offsetting increase from stocks and other investments. So, there's no wealth effect for most Americans.For middle America it already feels like recession, and sentiment indicators reflect that very strongly. Again, using a more realistic inflation number reveals that the average American is feeling the pinch. And it explains the University of Michigan sentiment numbers, which are at record lows, below the levels we reached during COVID if you can believe that.Enter the energy shock, and just remember that official inflation statistics were in fact creeping higher prior to the Mideast conflict. But with a reduction of 15 to 20% of global oil supplies, you now have inflation saturating the economy. CPI, PCE, and PPI, the wholesale price inflation index, all reflect higher levels of inflation. And over the last 90 days, the expectation of rate cuts have flipped to rate hikes. 100% probability of a hike by year-end, 67% probability of two hikes by this time next year. If you're watching the rate markets after the Warsh commentary today, the rates markets are expecting higher rates. Inflation brings a host of economic impacts and financial market complications, which will become obvious as the year proceeds. Morgan will discuss Fed monetary policy and bond market implications a little bit later.Not to get off track, inflation is not the only problem the bond market is dealing with. Yes, a 4.2% CPI print, 6.5% PPI print, they're meaningful, particularly for the bottom of the K-shaped economy, but too much supply—this is the big issue—too much supply and waning demand is also pressuring interest rates higher regardless of Fed monetary policy. Bonds face bear market dynamics, which many investors will in fact be surprised by.As for equities, I'll provide a few highlights. In summary, we are negative on the big indices like the S&P, the Dow, and the NASDAQ. This is in stark contrast with hard asset-related equities where we remain very bullish.Breadth in the main indices has narrowed. Only a few names are carrying the indices to new highs, which is never a healthy dynamic. Again, breadth is this [indicator of] how many companies are on the move to the upside. When there's only a few, that's an unhealthy dynamic. 50% of the year-to-date gains in the S&P 500 are from five companies.Valuations are between two and a half to three standard deviations from the mean. And on that basis, expected returns will hug the low single digits going out a decade. We look at the Shiller PE, we look at price to sales, we look at market cap to GDP for those valuation metrics.Examples might be helpful here. The median price to sales for the S&P 500 is 1.6. It currently trades at a very rich three and a half times. Compare that to Nvidia at 20 times; at Palantir, 63 times; or SpaceX at today's pricing of over 110 times price to sales. This is why I suggest that expected future returns based on those valuation metrics will hug the low single digits going out a decade. You are overpaying for those kinds of hype narratives.So what do we like? Hard assets continue to make sense today. We have built that case over recent years. We have built a diversified portfolio of companies that fall into four categories, all a unique expression of the hard asset theme. Global natural resources, infrastructure, precious metals mining companies, and real estate exposures in the form of publicly traded REITs.Each of these categories is like its own portfolio within the total framework—four portfolios in one. In this new cycle, we are witnessing gold as the tip of the spear, leading to further sequential opportunities in hard assets as the markets adjust to regime change.The studies we've undertaken and the portfolio allocations we're pursuing are gaining traction. As they gain traction, they also gain an audience. As the audience grows and capital begins to flow, positions that we are squarely in are positioned for growth. From a Goldman Sachs report released March 24th of this year titled "The HALO Effect: Heavy Assets, Low Obsolescence in the AI Era," I quote, "After more than a decade of under‑investment, Goldman Sachs Research analysts believe that higher real yields, geopolitical fragmentation, and supply chain rewiring have shifted equity leadership back toward tangible productive assets. They introduce the HALO framework—Heavy Assets, Low Obsolescence—to identify companies that are less exposed to technological obsolescence."So, now we have an acronym: HALO. Goldman and others are concluding in 2026 what has been in our minds for some time. While hard assets, or heavy assets, as Goldman likes to call them, are fresh on the minds of investors concerned about the implications of AI, we arrived at the same conclusion for a different set of reasons.AI is one more buttress for our argument. Hard assets are capital-intensive. Hard assets have low obsolescence. Hard assets rest in the middle of a scarcity bullseye. Hard assets provide resilience and are of great strategic value. Hard assets are on the diversification path for investors wanting to move from crowded tech, called capital-light trades, to a capital-heavy undercrowded domain.Commodities are breaking away from a floor-pinned position and rising in relative value to the popular abstractions of our day. Capital-intensive businesses have been on the move for several years, but their performance has been largely obscured from view by the capital-light companies outperforming them with their value tied to abstractions like intellectual property and brands. Examples of Nike and Coca-Cola come to mind, or companies that are selling software as a service and data flow, Microsoft, Adobe, Salesforce, or your leveraged networks and platforms, Airbnb, Uber, and things like that.Our perceived fallen angels have some advantages, which, to many investors, look like disadvantages. Operational complexity, resource scarcity, high sustaining capital requirements, energy and labor intensity, regulatory constraints, massive permitting requirements, long project timelines, all of which, again, most people would see as negatives, but these qualities provide the moats and cyclical advantages we're looking for in a period of rising inflation and rising interest rates.As an example, picture the copper mine built 30 years ago for 1.5 to $2 billion. To replicate that copper mine today might cost 15 to $20 billion, not the domain of a startup company, unless you're SpaceX, of course. This is not new-world stuff. In fact, it's old-world stuff. But guess what the irony is? The new-world stuff still depends on the old world, and that is a sweet revenge. Over time, a replacement is prohibitively expensive, permitting becomes harder, environmental limitations increase, skilled labor, which is very, very blue collar stuff, it's harder to find. And the asset-heavy nature of the companies reprices upward during inflationary regimes.Morgan: Former Treasury Secretary under Presidents Nixon and Ford William E. Simon famously said, "I continue to believe that the American people have a love-hate relationship with inflation. They hate inflation, but love everything that causes it." Now, for the last 50 years, it is the structure of the post-1971 dollar-based global system, or petrodollar system, that's allowed US policymakers to do everything that causes inflation without reaping the full massive inflationary brunt of their policy consequences. But now that post-'71 monetary system is beginning to break down and we believe the Iran war is the latest significant accelerant of that monetary regime change trend. We expect the current conflict with Iran will have deep and long-lasting implications for the post-1971 US dollar-centric global system. And since the war started, we are not alone in that view. The Iran war seems to have been a catalyst for Western media to begin to awaken to the reality of global monetary regime change, and to China's central role in facilitating it.In late March, there was a Bloomberg article titled "Iran War Could Be Making of the Petroyuan, Deutsche Bank Says." Then in early April, Bloomberg Macro Strategist Simon White penned an article titled "Iran War Has Caused Lasting Damage to the US Dollar System." Both articles pointed to very real and growing strains in the post-1971 global US dollar system.Both articles focused on how the Iran conflict could be the catalyst for both erosion in petrodollar dominance and the emergence of a competitive petroyuan, citing media reports that Iran was allowing the passage of ships through the Strait of Hormuz only if oil payments were made in yuan. Furthermore, both articles warned that the erosion in the petrodollar regime could have "significant downstream effects" to the dollar's use in global trade and savings, as well as to the dollar's role as a reserve currency.Also in April, Peter Alexander, CEO of Z-Ben Advisors, a Shanghai-based consulting firm essentially aiming to bridge the information gap between West and East, penned a very important article on Substack titled "China's Killer (Geopolitical) App." In the article, Alexander adds great detail to both the threat of damage to the US dollar system and to the golden origins of the petroyuan.As Alexander put it, "For more than a decade now, the Beltway consensus held that the US dollar system operates as a geostrategic choke point that can be deployed to alter the behavior of other state actors. Books have literally been written on this very topic, and it may have been true for a moment in time.What has yet to be recognized is that, in present day, a US dollar choke point has, in fact, run up against hard limitations on its efficacy. The American move to nakedly weaponize the US dollar system was a message received by Beijing with immediate effect. The risk, no matter how remote, of China being blocked access to SWIFT was existential. A solution was required and the People's Bank of China was tasked with finding a workable alternative.In 2015, that task was completed and the cross-border interbank payment system SIPS officially went live. SIPS conducts all functions—again, via RMB—from messaging to clearing to initial fiat settlement. It also became the first system to seamlessly integrate payment and settlement of the onshore and offshore RMB, CNH and CNY.Perhaps more consequential when it comes to the great power competition, SIPS resides fully outside the New York correspondent banking network. The very parties that sought to apply economic coercion for the purposes of altering unwanted behaviors are now blind.Obviously the introduction of SIPS was meant to directly benefit China. It is now also the case that the network is providing an attractive solution to a host of global south countries in an era where the Trump administration has ratcheted up the deployment of coercive economic and financial tactics as points of leverage.Now, Western critics of the viability of a petroyuan argue that in a global US dollar-dominated system, participants in the SIPS network would be stuck with too much unwanted excess yuan. But there are two important rebuttals to that argument. First, over the last decade plus, China has undeniably become the factory of the world, meaning there is no limit to the menu of offerings foreign nations can purchase from China with yuan. Second, the SIPS network utilizes a gold-based or gold-linked yuan for neutral net settlement in an emerging network often referred to as the Golden Road.As Alexander explains, SIPS is just the payment network. With China's capital account opened via the gold window, any trading partner holding RMB surpluses can directly convert all fiat balances into physical gold. That gold can be held in a Shanghai vault well beyond the reach of America's foreign policy of sanctions and tariffs, as well as the newly opened Hong Kong vault and vaults soon to be expanded into Saudi Arabia, Singapore, Malaysia, and eventually additional hubs plan for Dubai and Russia.And in addition to acting as a neutral reserve asset and facilitating non-dollar trade settlement, the entire China gold complex is also being positioned to act as a substitute for another critical component of the US dollar system. In this new system, gold can replace, at least at the margins, the role of US Treasuries in acting as global collateral. While not as liquid as US Treasuries, the usage of gold as collateral is meant to be levered as a mechanism to support a host of cross-border trade activities, including usage as a financial tool for invoicing of any return trade of physical goods. Beijing has been executing plans for this entire gold settlement solution for the better part of a decade. Its overt objective is mitigating the inherent risk of America's leverage over the US dollar system. The system is functional. It's now operational. And it's now expanding rapidly. More recently, in late May the Financial Times also picked up on the emerging petroyuan story and elaborated on it.In a May 21st article titled "Iran War Open's Golden Window with China's Renminbi," the FT, like Alexander, explicitly tied the rise of the petroyuan to China's SIPS international payment system and its gold link. Furthermore, the FT referred to the Iran war as "proof of concept". According to the FT, "Gold could serve as a neutral asset for countries to recycle excess renminbi into allowing China to maintain capital controls while competing more with the dollar in global trade. China has regulated the Shanghai Gold Exchange with a strict settlement system. Exporters to China can receive payment in yuan and immediately convert excess yuan into gold bars on the Shanghai Gold Exchange International Board without using dollars, but with the security of a neutral asset." Importantly, the FT noted that, since the Iran War, adoption of Beijing's SIPS cross-border payment system is surging to record highs.And as I said before, that the Iran war has provided "proof of concept" for the SIPS system. According to the FT, the average daily value of transactions settled through SIPS hit a record of $135.7 billion equivalent per day in March, as well as a new daily record in April of $150 billion equivalent per day.For perspective, that April daily record would translate to roughly a massive $50 trillion equivalent annual run rate. In short, SIPs adoption is now booming. Now, over the past two months, a popular narrative to explain gold's recent sell-off has emerged. It suggests the war with Iran is fundamentally bearish for gold and that, as a result, the war has catalyzed official sector gold sales. Now it is true that some nations did pare gold holdings in the first quarter. A number of central banks and sovereign wealth funds shed an estimated 115 tons in the first quarter of 2026, but the vast majority of those sales were one-time events mostly attributed to liquidity effects stemming from the closure of the Strait of Hormuz.Those sales, combined with the negative price action, raised concerns about institutions' appetite for gold and their interest in continuing the dedollarization trend. But a Bloomberg report may fully dismantle that gold-negative narrative, as in reality, even net of previously mentioned gold sales, Q1 net central bank purchases totaled 244 tons, up from 208 tons in the previous quarter, marking the fastest pace of central bank gold buying in almost two years.Again, the 244 tons was a net purchase number. It includes the 115 tons of one-time Hormuz-related gold sales. The red extension line on this slide displays the actual 359 tons of Q1 central bank gold buying if you adjust out one-time Hormuz-related sales. And after adjustment, Q1 was essentially tied for the third-largest quarter of central bank gold purchases on record. And in MWM's view, it's no mistake that such a strong quarter of central bank gold purchases occurred alongside record-breaking levels of average daily values of SIPS network transactions.In short, the Iran war didn't launch the SIPS gold-based petroyuan, but is proving what the FT called a proof of concept. And it is proving to be the catalyst for a dramatic acceleration of the global recognition and adoption of the SIPS gold-based petroyuan. In sum, the non-dollar energy and commodity trading system that net settles surpluses into gold that former Goldman Sachs Head of Commodity Research Jeff Currie first described as gold recycling replacing dollar recycling two years ago continues to gain notable traction in the East and growing awareness in Western financial and media circles.In MWM's view, when gold's technical correction ends, the next leg of the gold bull market is likely to be greatly enhanced by the growing recognition among Western investors of global monetary regime change dynamics.With Kevin Warsh and the Fed facing a bond market crisis while their policy hands are tied, and the gold-based rails of an alternative non-dollar global system beginning to hit its stride, MWM is confident that we don't have to wait long for the gold bull market to shake off the ongoing technical correction and resume trend to new all time highs and beyond.David: I'll start with, "If the Fed increases rates and takes a more responsible fiscal policy, what does that mean for the gold price?" Morgan, you hit that squarely in your comments, but perhaps you could reiterate the standard assumption and what we've discussed in-house in terms of the Summers-Barsky thesis, how it would behave under one set of circumstances and why this time is different.Morgan: So basically Summers-Barsky is talking about gold basically moves inversely to real rates. So higher real rates makes gold less attractive and negative real rates makes gold attractive. But in our view, that dynamic is only fit for a healthy system. And I think we're far from a healthy system. So as I said in my presentation, I'm definitely of the mind that they may be able to hike interest rates 25 basis points, maybe 50 basis points, and maybe for a period of time. But we're at that point where the negative impact to the deficit via interest expense adding into government expenses and growing as fast as it is and ballooning as much as it has, you're talking about putting a debt spiral into motion if you allow real rates to go higher for longer.So I think those days are done, and I don't think they can— Part of the question was, I believe, is if they get more austerity in their fiscal policy. And that's also problematic for them because for one thing we're increasing defense spending, not cutting it—dramatically in fact, the plan is.And then we're not going to cut entitlements for political reasons. And also we aren't going to cut spending really because if we did at this point, government spending is such a large part of GDP that you would very likely trigger a recession. A recession means lower tax receipts. The stock market falling means the capital gains taxes drop. And again, that just feeds into the circular nature of the debt spiral dynamic. So I don't think there's really— I mean, I think practically speaking there is the cap yields and inflate your way out of this, is practically speaking what we're ultimately dealing with.David: The next question I'll take. "What does the price of gold look like in the future if retail investors do not participate in gold in a meaningful way even as government debt levels increase, the economy suffers, inflation interest rates remain at current levels or even increase?"I think the best analog for that is what we've witnessed from 2022 through 2025, where we basically had a $2,000 increase in the price of gold with virtually no participation from the general public. You could argue, and if you look at ETF statistics, there was a significant uptick in retail demand from the middle part of 2025 through the end of last year and into the beginning of this year. So retail did show up. But if you wanted to know what the price of gold looked like without the retail investor, central bank demand has been absolutely critical to driving the price. That 2,000 point move higher from 1,650, 1,800 to over 4,000 an ounce, largely attributable to central banks doubling their purchases from a run rate which was 500 tons per year and has been averaging at or above 1,000 tons a year since 2022.Central bank demand is not a forever thing, but we do see that continuing over the next several years. Morgan illustrated what the motivation would be from the standpoint of—well, I just mentioned from the standpoint of reserve management and what central banks want as a denomination for their reserves. And Morgan hit on how gold demand would be very central to a system of trade which does not settle in dollars and does not promote recycling of trade dollars or petrodollars into the US Treasury market. So that alternative system is yet another source, which is trade related, not retail or investor related.I do think that retail comes into the gold market at some point. And what we have witnessed in past bull markets in metals—we've been in the metal space for 54 years—and what we've witnessed there and even prior to that, if you wanted to stretch back 50 to 100 years or more, is that retail chases gold when it's afraid of something else. And so if that's volatility in the equity market, if that's volatility in the bond market, safe haven dynamics ultimately kick in. And today you don't see the need for it as people clamor for the newest, shiniest gizmos, gadgets, and solutions via AI.So when those markets turn, if those markets turn, I think retail has a motivation to diversify their own reserves, so to say, and look at it as a safe haven. But the moves in metals are not dependent on retail. I think central banks have defined the floor in gold. Retail will ultimately blow out the ceiling, which is a chapter yet to be written.The next question, "Have you seen the price estimates for gold in July of $20,000 an ounce or $1,500 an ounce for silver?" I have seen those. Of course, being in the metals business for 54 years, we've seen all kinds of projections over time. And what we would suggest is that a Dow/gold ratio of two to one or three to one is very reasonable. And so if you assume the movement of numerator and denominator, both of those things moving toward each other, you could see gold in the range of 15,000 an ounce. 12,000 I think is not unrealistic. 15,000 becomes a high watermark.Perhaps we could see 20, but I think you're beginning to really wonder at that point—at any point higher than that—if the true commentary is not supply and demand, but just reflecting a broken currency like we've seen with the yen. One ounce of gold trades for 750,000 yen. Is that particularly meaningful? Well, it is if your savings are based in yen because you've preserved your purchasing power as the currency has gone through a veritable meat grinder.So at some point prices become irrelevant. It's one of the reasons why I think looking at the Dow/gold ratio and looking at relative values is super important because we may be looking at the Dow at 150,000 and gold at, again, a three to one ratio, 50,000. You know the high price based on relative value, not nominal pricing in the context of competitive currency devaluation.* * *

Well, you've been listening to the McAlvany Weekly Commentary. I'm Kevin Orrick, along with David McAlvany. You can find us at mcalvany.com and you can call us at 800-525-9556.* * *

This has been the McAlvany Weekly Commentary. The views expressed should not be considered to be a solicitation or a recommendation for your investment portfolio. You should consult a professional financial advisor to assess your suitability for risk and investment. Join us again next week for a new edition of the McAlvany Weekly Commentary.

* * *