Podcast: Play in new window

Once again silver was the star of the show this week, posting a 7% gain and closed in on the $80 mark. Gold climbed an admirable 1.7% while white metals also saw some modest gains. With the broad strength across the metals market, copper was not to be left out as it pushed toward all-time highs and showcased the rising inflationary pressures along with rising manufacturing costs.

Let’s take a look at where prices stand as of Wednesday, April 15:

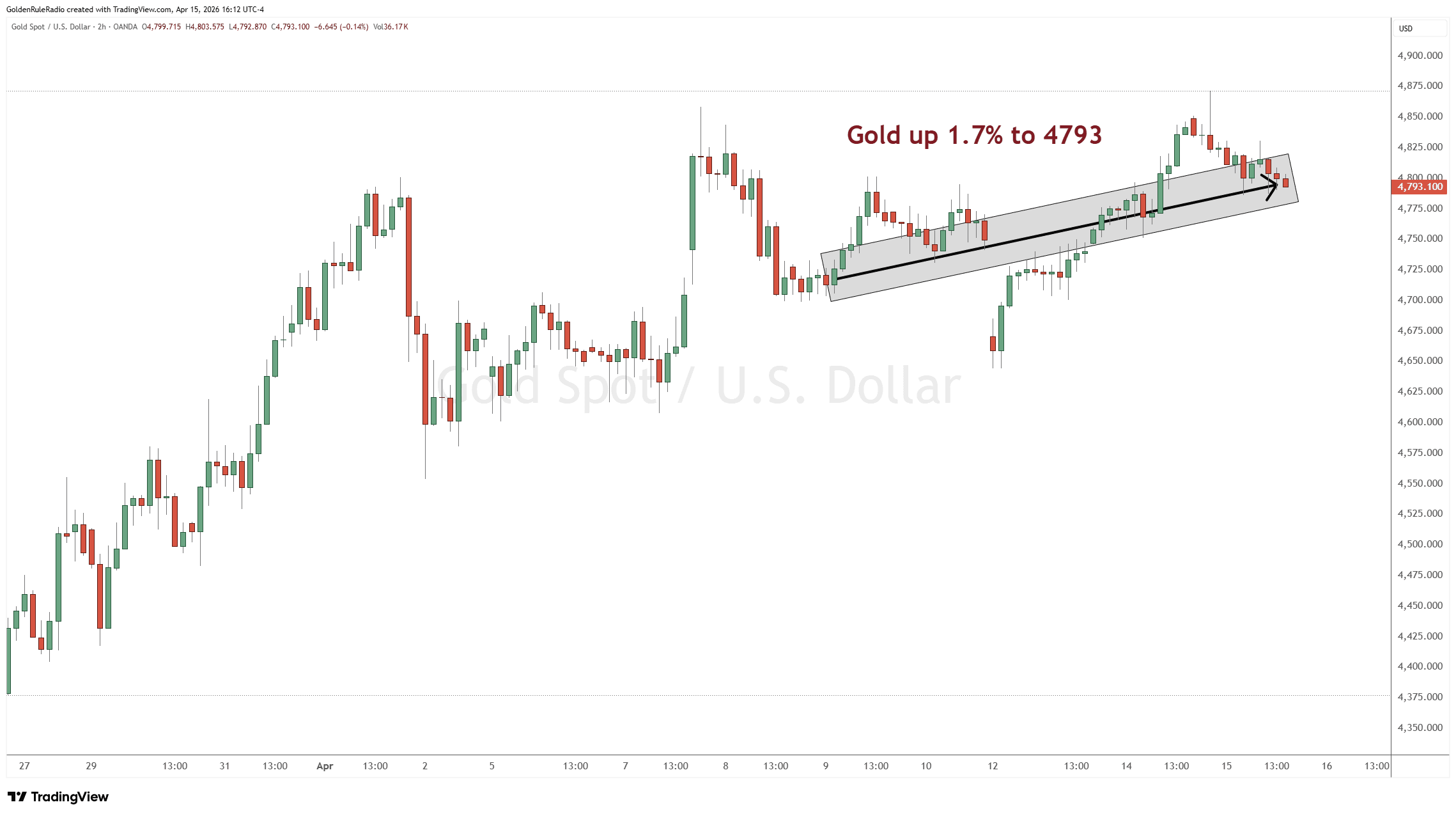

Gold is up about 1.7% sitting at at $4,793 an ounce and still holding in pretty strong.

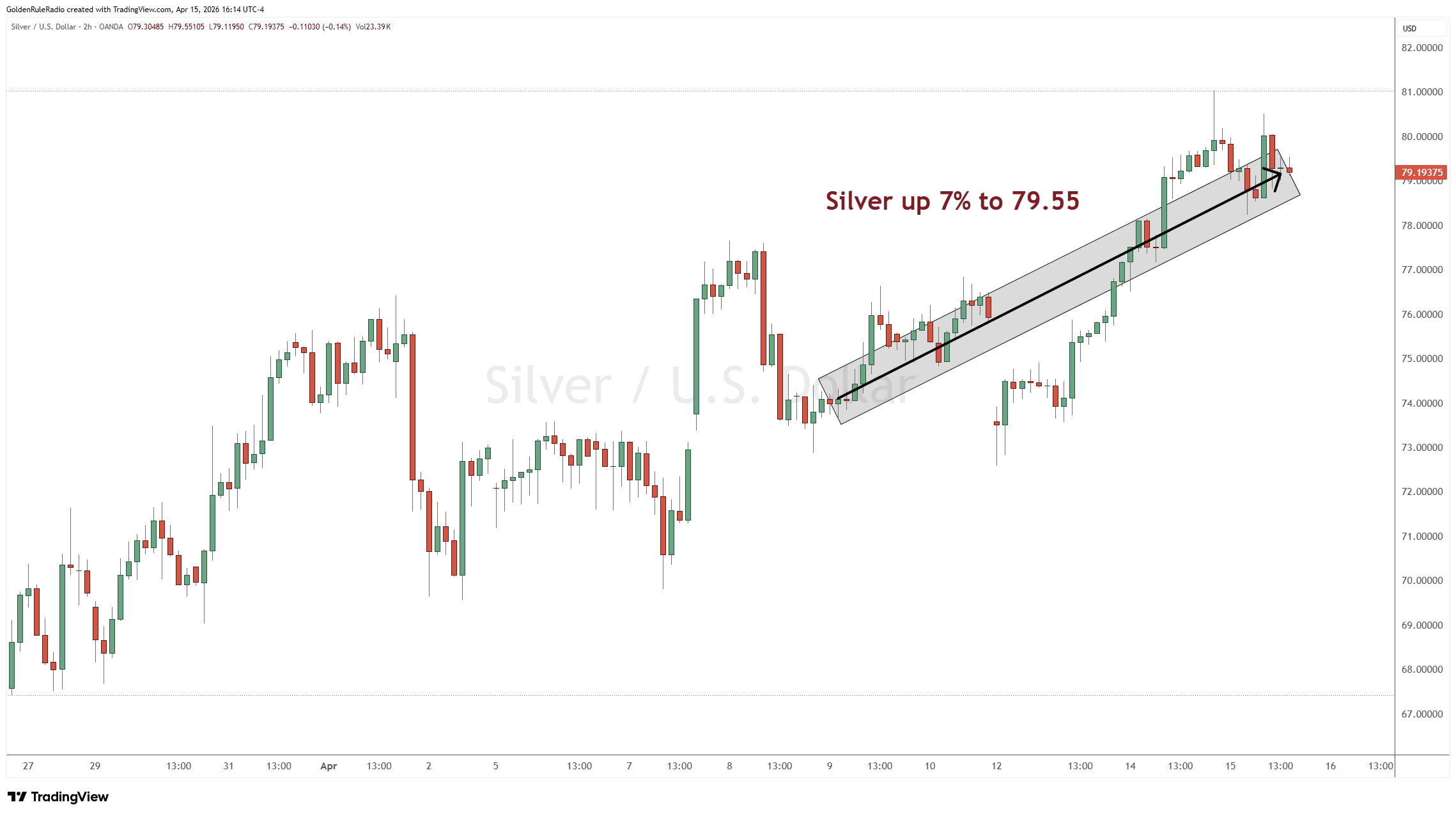

Silver is up 7% this week, sitting at $79.55 as of this week’s recording.

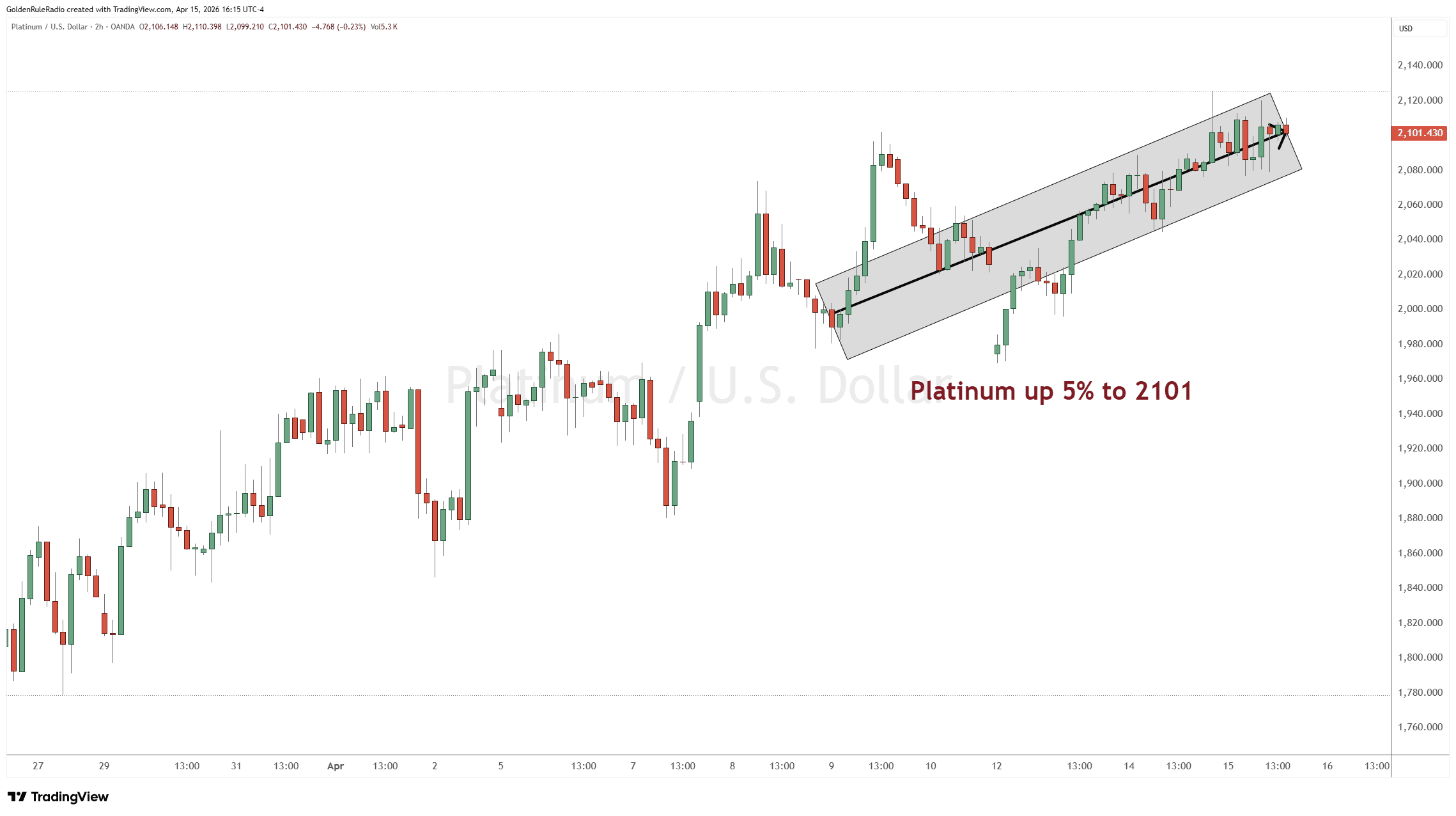

Platinum is up 5% at $2,101 from a week earlier.

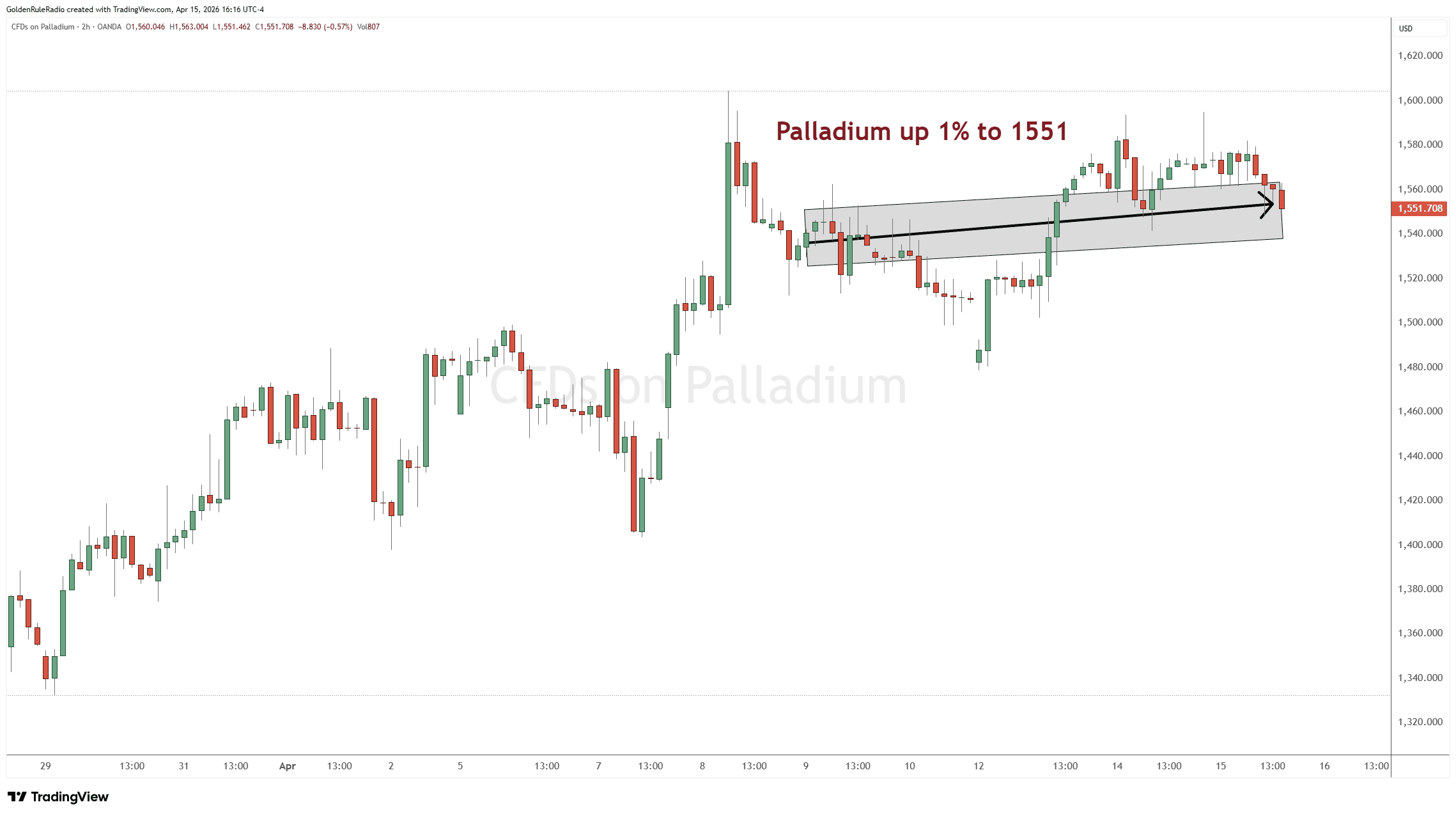

Palladium is up about 1% at $1,550. So all four metals are having a solid week since our recording last week.

Taking a look over at the paper markets…

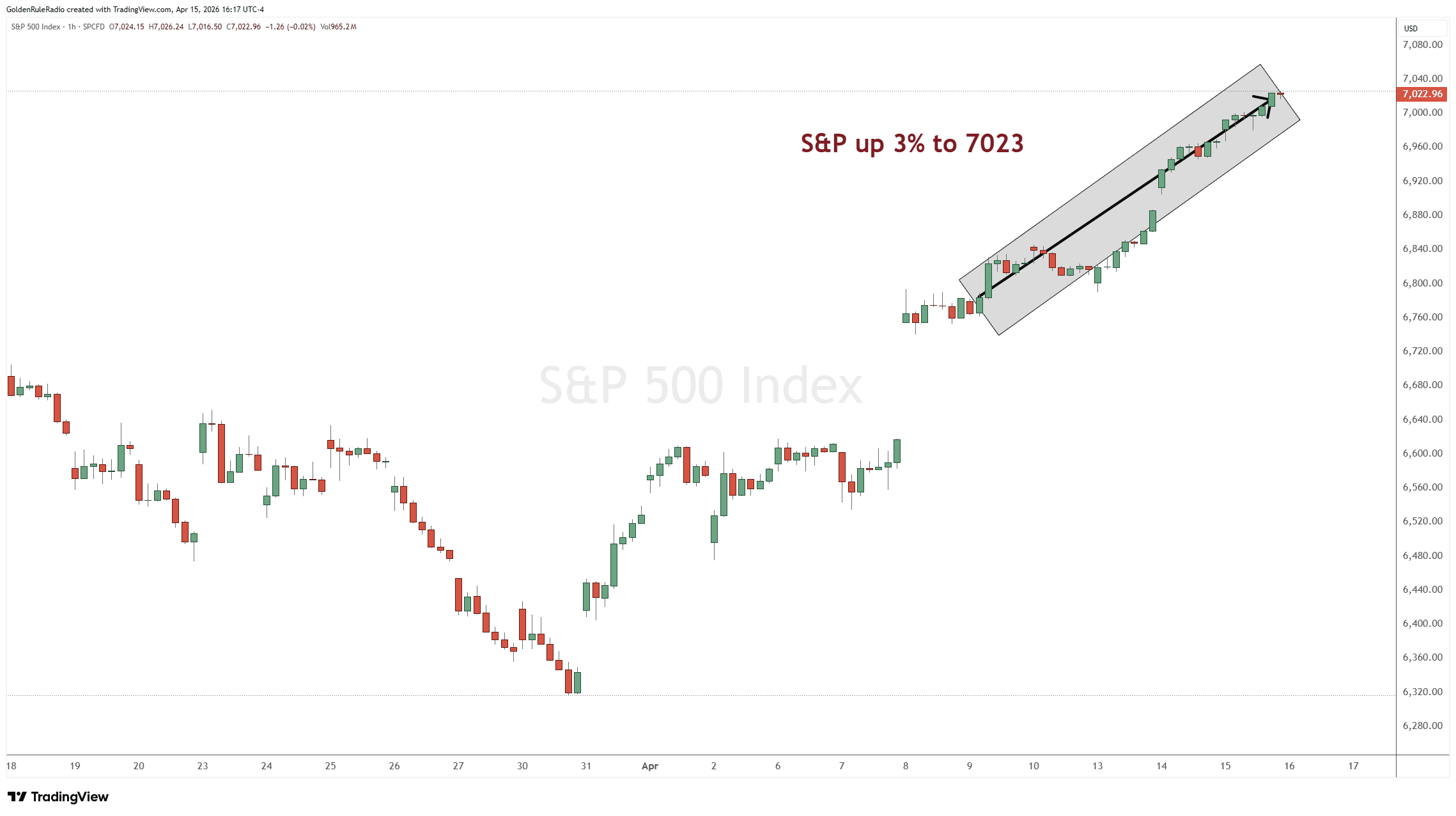

The S&P 500 is up 3% to 7,023 — hitting an all-time high this week. It is up 11% as of as of recording, and it has been on a bit of a tear the last couple of weeks.

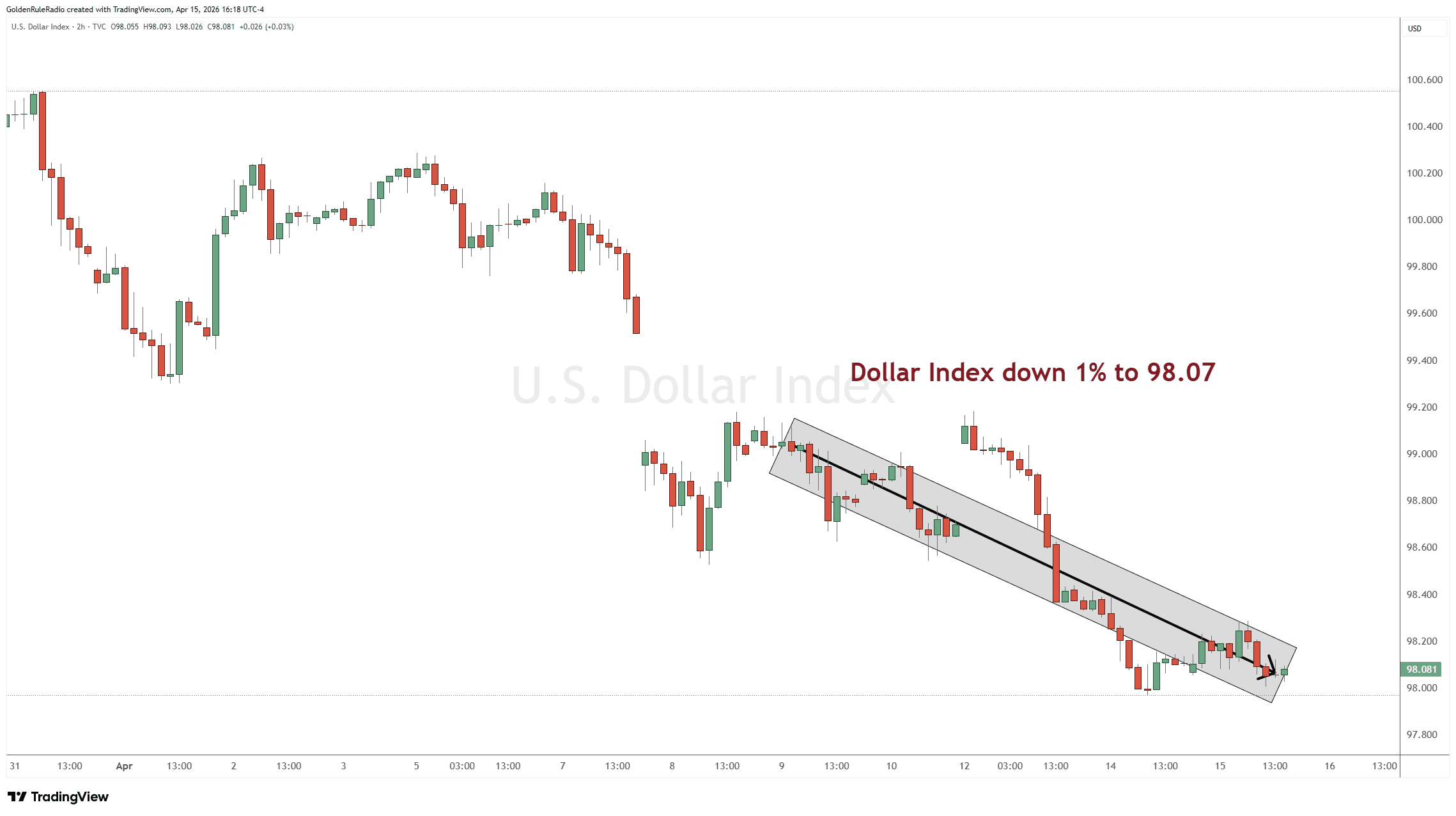

The US Dollar Index is down 1%, sitting at 98.07.

White Metals Dominate

After weeks of gold holding the headlines, silver jumped 7% this week while platinum added 5% — both outpacing gold’s solid 1.7% gain. More telling than any single week’s numbers: silver has now posted four consecutive up weeks. That kind of sustained momentum, building quietly rather than spiking all at once, is exactly what constructive trend behavior looks like.

Intraday ranges remain wide — silver touched $81.14 overnight before settling just under $80 in U.S. trading — which reflects the continued tug-of-war between leveraged paper positions and physical demand. But as we’ve noted for months, attempts to knock silver lower keep meeting buyers. The physical market is increasingly setting the terms, not the futures pits.

Dr. Copper Reaches For All-Time High

Copper nearly touched $6.50 this week, sitting within a nickel of its all-time high. “Dr. Copper” historically signals expanding economic activity and manufacturing demand — and right now, it’s telling you two things at once.

First, copper has simply lagged. With the cost of living roughly doubling in the last decade, copper’s percentage gains haven’t matched what silver, platinum, or even oil have done. Some of what you’re seeing now is catch-up to embedded inflation.

Second, the AI sector’s electricity appetite is enormous — and every one of those server farms runs on copper. The demand picture is unlike anything the market has previously modeled. A logarithmic move higher in copper prices, rather than the steady stair-step of the last two decades, is a real possibility.

For precious metals investors, elevated copper reinforces the case that we’re in a broad commodity repricing cycle — one that has years left to run.

Ratio Trades Favor Swaps Into Gold

The gold-silver ratio this week sits around 60:1, down from over 100:1 just a year ago. That’s a dramatic move — and it’s already generated extraordinary gains for investors who swapped silver for gold at extreme ratios. But the trade isn’t over.

At 60:1, the ratio continues to indicate swapping silver gains into gold — particularly inside IRAs, where no capital gains tax applies to the trade. The math is straightforward: silver has dramatically outperformed gold over the past year, and the ratio trade lets you lock in that outperformance as additional gold ounces.

You don’t need the ratio to hit 40:1 to benefit. Disciplined, incremental moves at current levels still grow your total holdings meaningfully.

Central Banks Continue De-Dollarization

Central bank gold holdings have now surpassed the U.S. Treasury holdings in value. That’s not a marginal shift — it represents a generational realignment in how sovereign wealth managers think about reserve assets.

For decades, Treasuries were the default. Gold was an old-world relic. That mental model is now officially outdated. And it’s not just central banks. Wall Street firms are now publicly recommending 20–25% physical gold allocations for their top clients. That recommendation, coming from people with every financial incentive to push paper assets, is something none of us have seen in four decades in this market.

The underlying driver is straightforward: in a world where trust is fracturing between major economic blocs, gold is the only asset that carries no counterparty risk, can’t be printed, and can’t be frozen by sanctions.

Stagflation Backdrop Is Good for Gold

CPI came in at 3.3% year-over-year last week — up sharply from 2.4% the prior month. PPI is running at 4% year-over-year. The Fed’s stated target is 2%, and they’re nowhere near it. Meanwhile, oil’s surge tied to the Iranian conflict is a classic stagflationary input: rising costs into a slowing, over-leveraged consumer economy.

Rate cuts are effectively off the table as long as inflation is re-accelerating. That removes one of the typical pro-gold catalysts — but gold is rising anyway, because the real driver isn’t rate expectations. It’s the structural deterioration of confidence in fiat money itself.

Every dollar of deficit spending, every trillion added to the national debt, every new money-creation cycle is a slow leak in the purchasing power of cash. Gold doesn’t need a crisis to perform. It just needs the status quo to continue.