Podcast: Play in new window

Silver surged upwards this week with a 13% rise and nearly reached $90. While gold remained relatively flat, platinum continued its breakout and pushed up to $2,150. As central banks continue to buy gold, its value as a reserve currency begins to outweigh its use as a traded commodity. Comparatively, silver’s volatility keeps opportunities open for strategic exchanges based upon the gold-to-silver ratio.

Let’s take a look at where prices stand as of Wednesday, May 13:

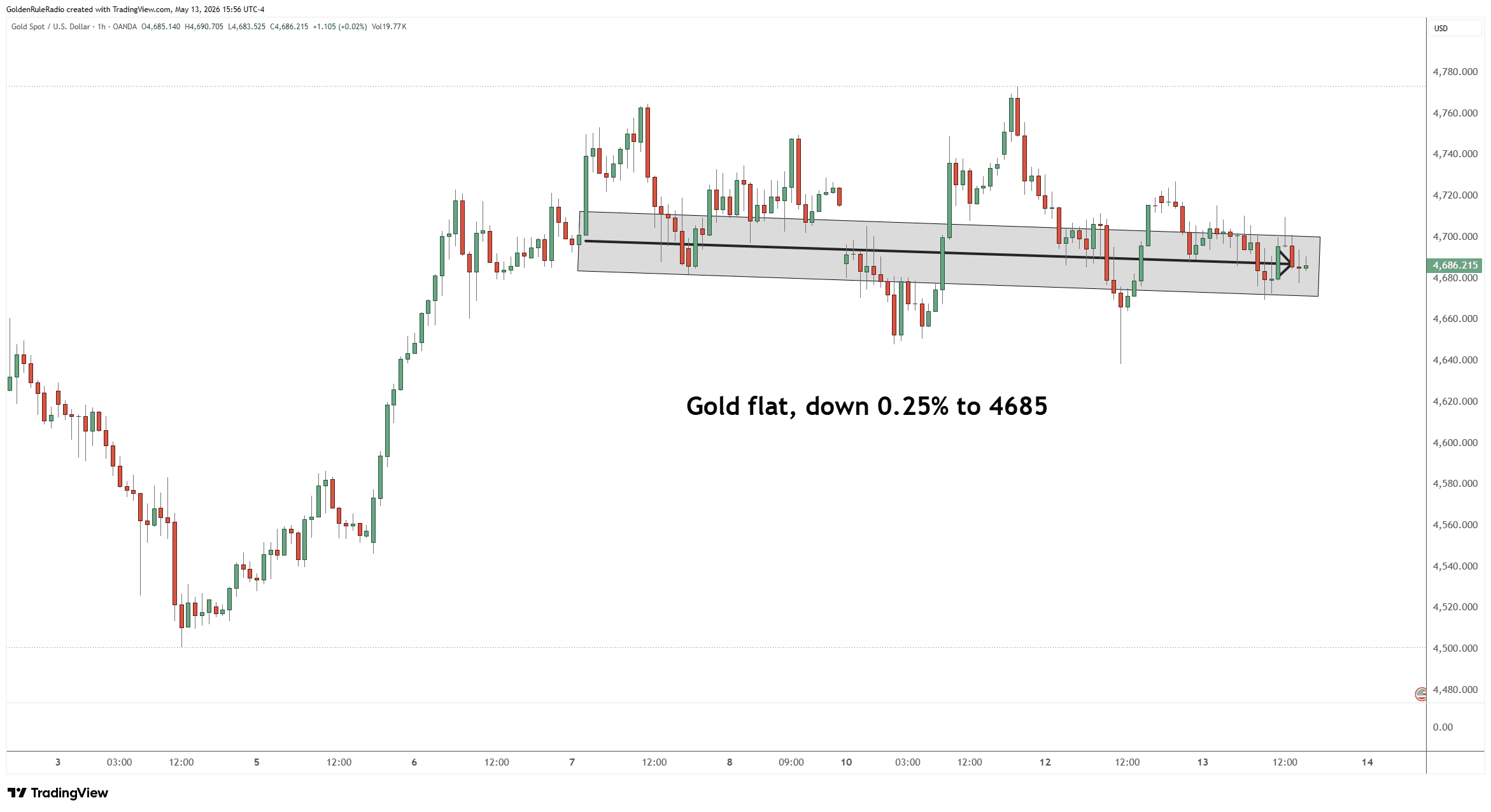

The price of gold is essentially flat on the week, down about 0.25%, sitting just under $4,700 at $4,685.

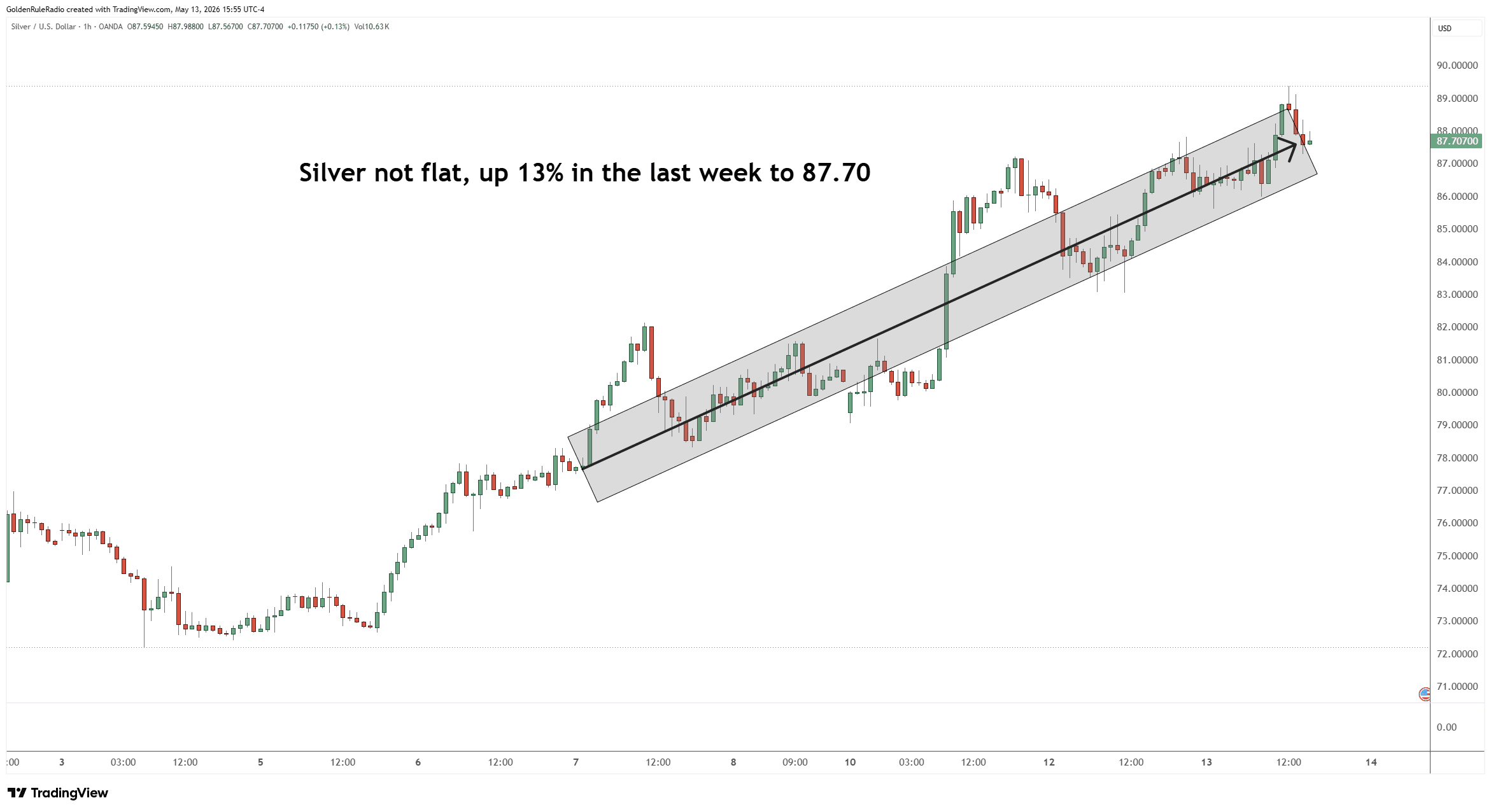

The price of silver is the standout — up a staggering 13% on the week, screaming back toward $90 an ounce and currently sitting at $87.70.

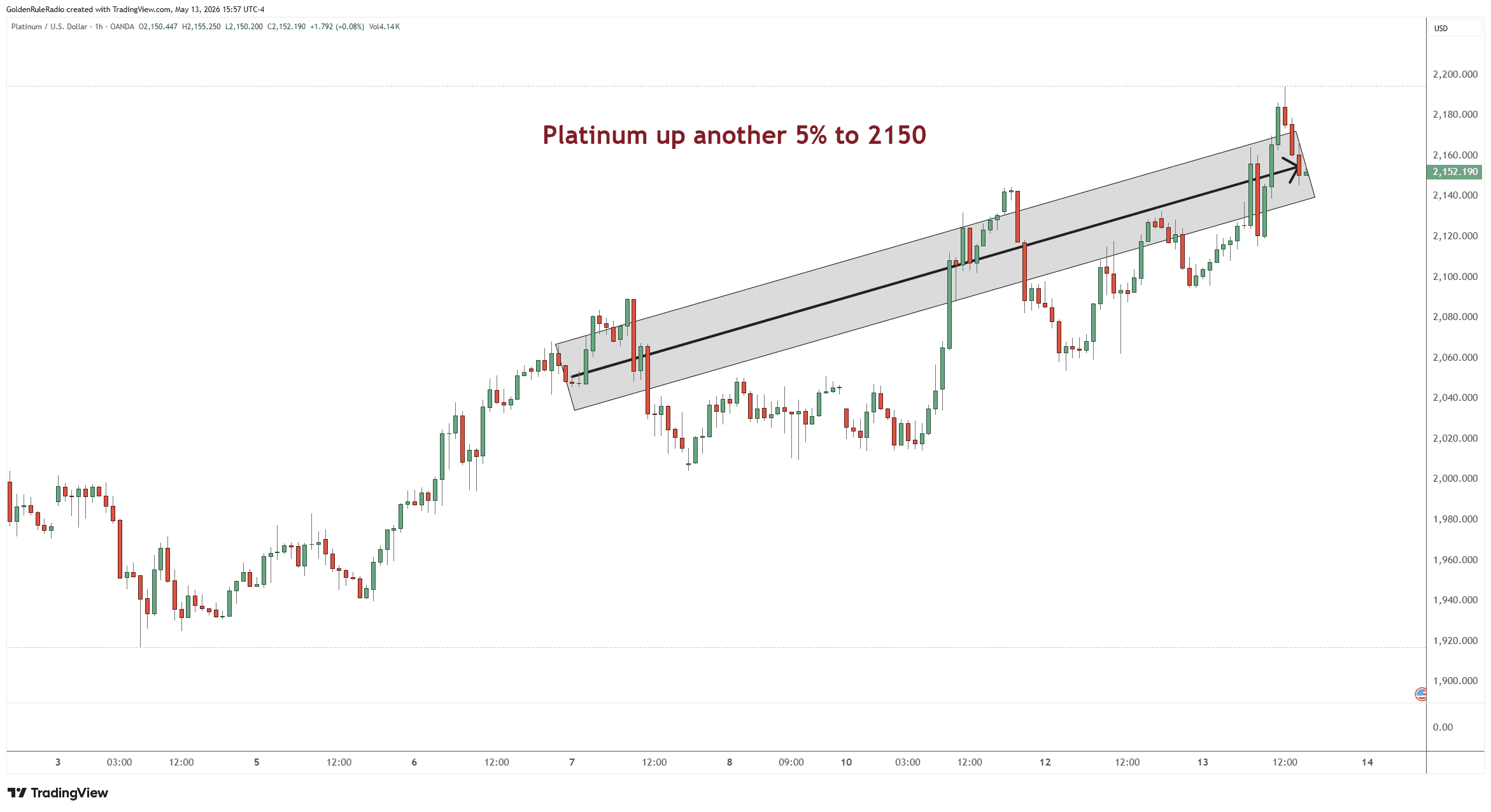

Platinum is up another 5% this week after gaining 9% last week — a two-week tear upward for a combined 14% move. It’s sitting firmly above $2,000 at $2,150.

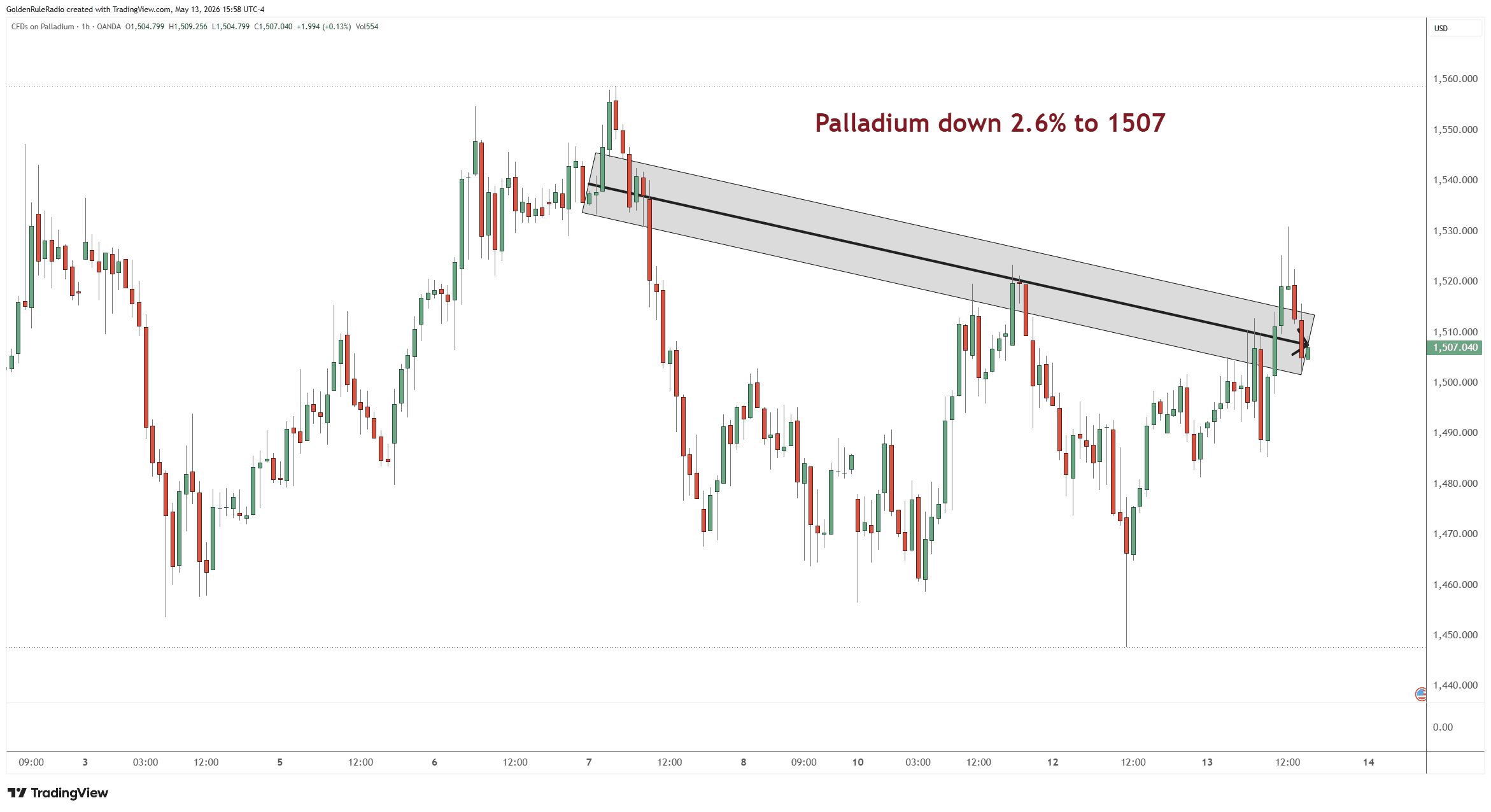

Palladium is the outlier, moving in the opposite direction — down 2.5% to $1,507. The gap between platinum and palladium continues to widen.

Taking a look over at the paper markets…

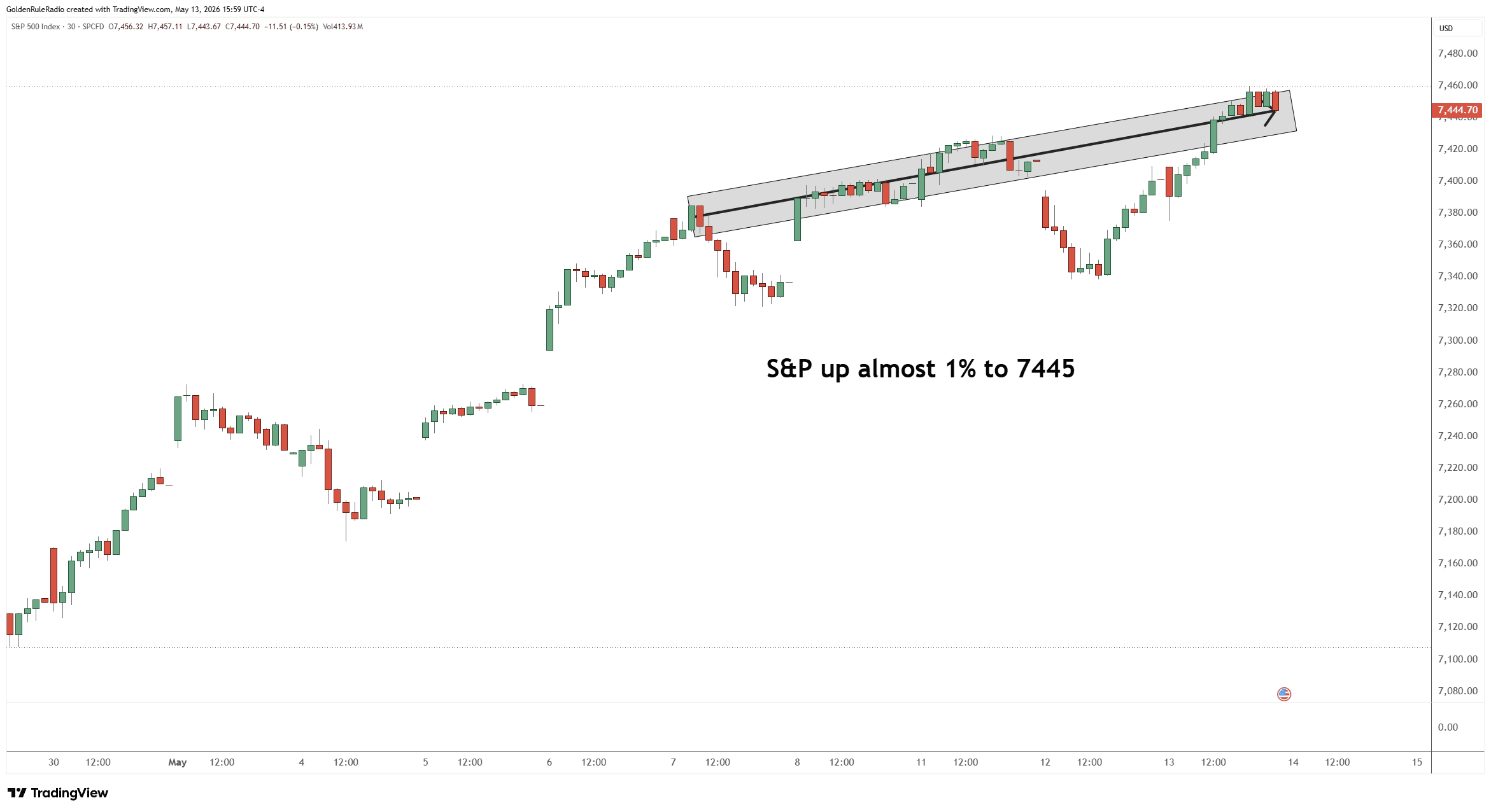

The S&P 500 is up almost 1% on the week at 7,445, continuing its recent run higher.

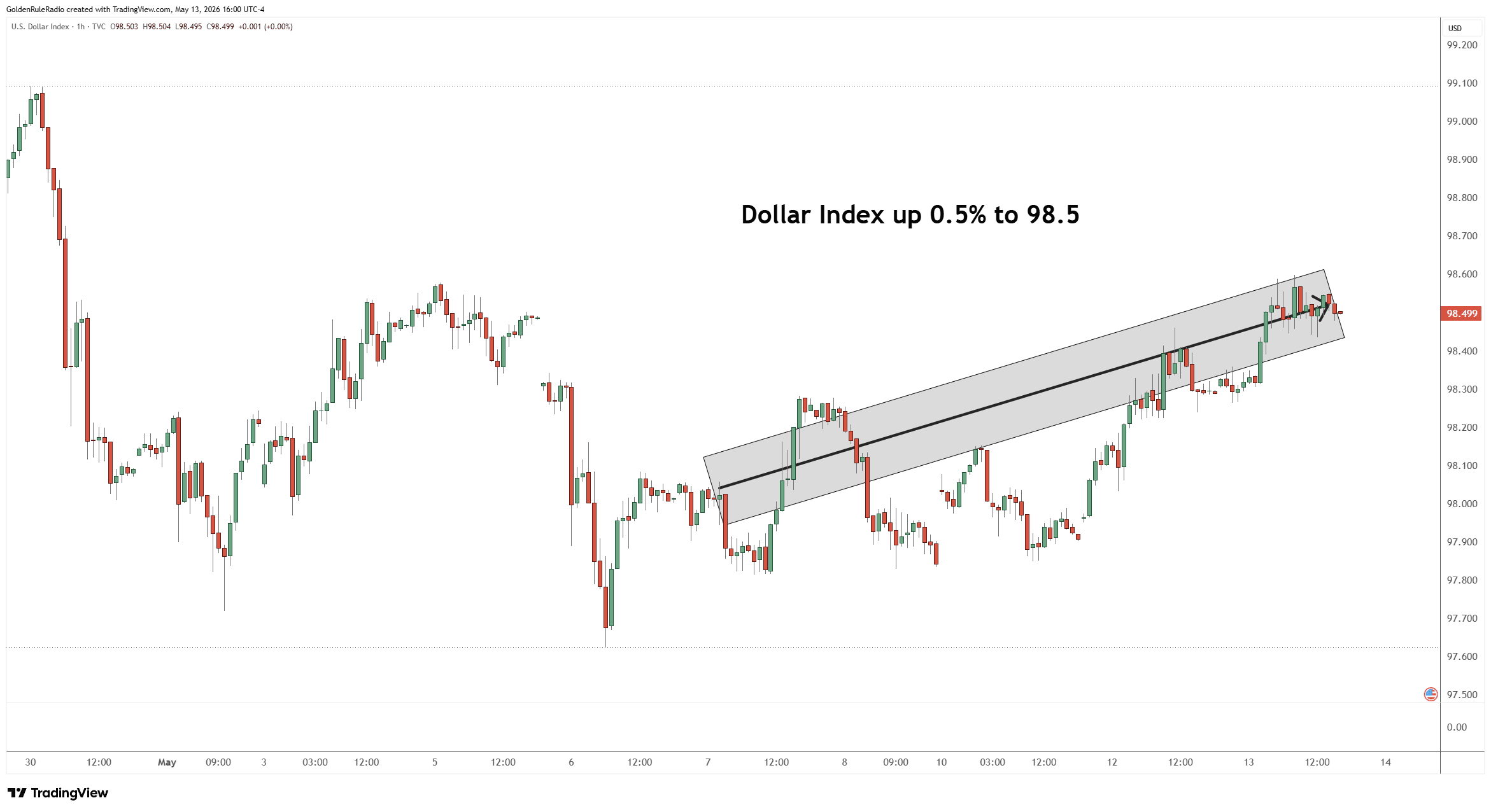

The US Dollar Index (DXY) is up about half a percent at 98.5.

The Dollar Story Is Bigger Than the DXY

One of the most important — and underappreciated — points is that the DXY index is an increasingly misleading way to measure the dollar’s health. Because it’s roughly 50% weighted against the Euro, it essentially reflects a US/European currency comparison and not much else.

When you overlay the DXY against the Fed’s broader trade-weighted dollar index, which brings in 25 to 30 additional countries including China, Asian trade partners, Latin America, and the Middle East, you start to see a different and more concerning picture. The dollar is weakening on a broader global basis, and so are European currencies alongside it.

This matters because the real geopolitical and monetary conversations happening right now aren’t US vs. Europe — they’re about China, the Asian trade bloc, the Middle East, and South America. As those relationships shift, measuring dollar strength only against the Euro misses most of the story. Domestically, the inflation pressures we’re feeling are showing up in those trade-weighted relationships as well. It’s a global problem, not just an American one.

Gold Transforms From Commodity to Currency

For the past 40 to 50 years, gold has been traded primarily like any other investable asset — analysts applied the same chart-reading frameworks to it that they would to equities or bonds, predicting price based on investor behavior and capital flows. That mental model is becoming obsolete.

What we’re now witnessing is a policy-level transition. Global central bank gold reserves, which had fallen to as low as 9–10% of total reserve assets, are climbing back — now at 20–25% and growing, and beginning to surpass the US dollar’s share in international reserve holdings. Nations that once dismissed gold are now actively rebuilding their reserves and using gold as collateral in cross-border trade.

Gold is no longer just a hedge against inflation. It is increasingly functioning as the replacement currency of choice when trust in the dollar system breaks down.

For decades, investors have asked: if the dollar fails, what replaces it? The Euro was supposed to be the answer 20 years ago. Then it was the Chinese yuan. But history keeps returning to the same answer — the asset that has served as money for 4,000 to 5,000 years.

That shift in how gold is being used at the sovereign level is what drove prices from around $1,600 in mid-2022 all the way to $5,600 earlier this year. The current consolidation near $4,685 is traders finding their footing after an extraordinary run — not a sign that the trend is broken.

Silver at $90: A Critical Technical Moment

Silver’s 13% surge this week brings it right to a key decision point. After topping out near $120, falling all the way back to around $60, and now rebounding to nearly $90, silver has recovered approximately 50% of its entire decline. That 50% retracement level — right around $90 — is where silver is likely to run into its first significant resistance.

If silver pushes through $90 and holds, there’s a path toward a retest of prior highs near $120, which would constitute a potential double top — a setup that bears watching closely. If it stalls here and rolls over, that’s equally meaningful for how you position.

The broader takeaway on silver: even at nearly $90 an ounce, it remains significantly undervalued relative to where it traded historically and relative to gold.

Silver is still very much an investable asset in the traditional sense — driven by both industrial demand and investor positioning. Gold is increasingly becoming a policy and currency conversation. That divergence is real and growing, and it’s showing up in the way the two metals are trading relative to each other right now.

Platinum deserves a mention here as well. At current pricing, it may represent the most compelling value in the precious metals complex.

Gold-Silver Ratio: Review Your Position

With silver dramatically outperforming gold over the past several months, the gold-to-silver ratio has declined sharply. That creates a window — one that may not stay open indefinitely — to convert silver gains into additional gold ounces.

If you entered silver at ratios of 70, 80, 90, or even 100-to-1 during the post-COVID years, you’ve captured an enormous move. The question to ask now is this: “How many more ounces of gold can my silver buy today compared to when I bought it?”

Turning 10 ounces into 15, 15 into 20 — that compounding effect over a decade matters far more than whatever the dollar price happens to be at any given moment. Ten years from now, whether silver is at $200 or $500, what will matter is how many ounces you hold.

If your portfolio is currently weighted 50%, 60%, or more toward silver, this is a good time to reach out to your advisor and review your entry points and the current ratio. Taking measured, gradual steps to rebalance into gold while silver is strong is exactly what this kind of market rewards.

The Equity Market Disconnect

A final note on stocks: the S&P is sitting at 7,445 and the headlines sound bullish, but a look under the hood tells a more complicated story. The gains are heavily concentrated — Nvidia alone is up over 3,000% over the past four to five years, while the majority of the other 29 S&P stocks have gained a comparatively modest 100–300%. The market’s strength is being carried by a very small number of companies.

At the same time, rising costs of living are hitting ordinary Americans harder than rising stock portfolios are helping them. There’s a growing divide between those whose net worth is tied up in equities and those simply trying to manage monthly expenses. A strong stock market doesn’t pay the grocery bill.

Call for a Complimentary Portfolio Review

Whether you’re adding to an existing position or just getting started, the team at McAlvany Precious Metals is here to help you build a plan that fits your goals. With a collective 75 years of experience in the precious metals market, we offer complimentary, no-obligation consultations. Give us a call at 800-525-9556.